Following the 2008 financial crisis, regulators across the globe have pondered how to ameliorate systemic risk in derivatives markets. At the 2009 G-20 summit, international regulators committed to address this risk through clearing and capital requirements for market participants. The implementation of a particular capital requirement known as the Basel III leverage ratio, however, may undermine derivatives clearing for clients of clearing firms that are banks subject to the leverage ratio (Clearing Firms). Coordinated regulatory intervention will be required to ensure the leverage ratio does not compromise derivatives clearing and the overarching objective of reducing systemic risk.

The Dodd-Frank Act implemented the G-20 commitment to clearing by requiring the clearing of certain standardized swaps through a regulated central counterparty or clearinghouse (CCP). The Commodity Futures Trading Commission (CFTC) has implemented the Dodd-Frank mandate by requiring most interest rate swaps and credit default index swaps to be cleared. In order to avoid counterparty credit risk, market participants also have elected increasingly to clear less-standardized swaps and other swaps that the CFTC has not required to be cleared. Today, about 75 percent of transactions in the markets that the CFTC oversees (which also include futures markets) are centrally cleared — an exponential increase from about 15 percent as of the end of 2007, according to testimony from CFTC Chairman Timothy G. Massad before a Senate committee in May 2015.

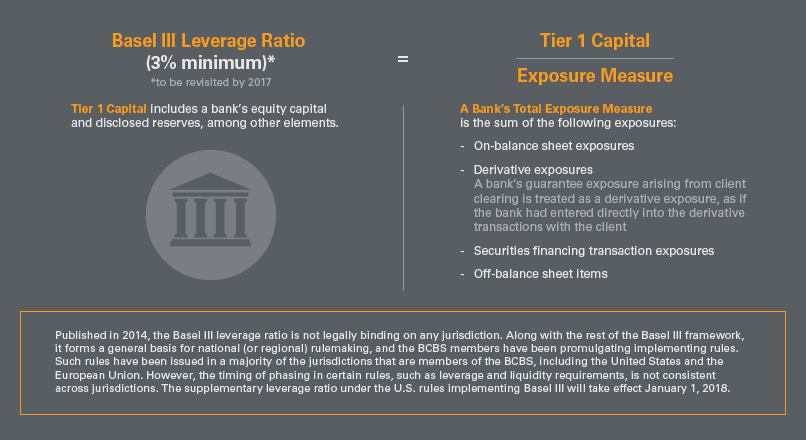

The Basel Committee on Banking Supervision (BCBS), an international regulatory body, addressed the G-20 commitment to strengthen bank capital requirements by promulgating a global framework that includes, among other initiatives, the Basel III leverage ratio. The ratio measures a bank's core capital (e.g., equity capital and disclosed reserves) against an exposure standard that includes the bank's on- and off-balance sheet sources of leverage and its derivatives exposure. Under the minimum leverage ratio requirement set forth by the BCBS, a bank's core capital should be at least 3 percent of its total exposure. (The BCBS will revisit this requirement in 2017 at the latest.) This is intended to constrain the buildup of leverage in the banking sector and improve banks’ ability to withstand stresses of the magnitude associated with the 2008 financial crisis.

Clearing Firms, their clients, CCPs and the CFTC have raised concerns regarding the manner in which the Basel III leverage ratio calculation takes into account a Clearing Firm's exposure from client clearing. In particular, the Basel III leverage ratio framework states that a Clearing Firm will "calculate its related leverage ratio exposure resulting from the guarantee [of its client's cleared derivative trade exposures to the CCP] as a derivative exposure … as if it had entered directly into the transactions with the client." If the leverage ratio framework treats a Clearing Firm as a direct party to the cleared derivative trade with its client, then the Clearing Firm's exposure would be greater than it would be as an intermediary and financial guarantor for that trade. For instance, by creating the legal fiction that the Clearing Firm is its client's counterparty, the leverage ratio framework would preclude the Clearing Firm from reducing its derivatives exposure by the collateral (or performance bond) posted by the client. This would be the case even though such collateral is held by the relevant CCP (which is effectively the client's true counterparty) and is legally and operationally segregated and thus not available for the Clearing Firm to use as leverage.

As a result (albeit unintended) of the Basel III leverage ratio treatment of their exposure from client clearing services, Clearing Firms may need to hold more capital than they have available or reduce their leverage, or both. Faced with an increased capital requirement, Clearing Firms may pass capital costs to cleared derivatives clients, which might in turn forgo trading cleared derivatives. Clearing Firms also may have to off-board certain clients or, if costs become prohibitive, cease offering client clearing services altogether. At least for futures and certain standardized swaps, which must be cleared under U.S. law, a market participant's inability to access clearing services would effectively preclude that participant from entering into these products. Overall, the reduced availability of clearing services would run counter to the globally endorsed and Dodd-Frank-codified goal of promoting clearing to address systemic risk.

CFTC Chairman Massad recognizes this issue and is working toward a proposed solution. In a 2015 speech before the Institute of International Bankers, Chairman Massad stated in regard to the U.S. implementation of the Basel III leverage ratio: “I am concerned that the rule as written could have a significant, negative effect on clearing, which is obviously a key policy goal of the Dodd-Frank Act. I have spoken with my fellow regulators on this issue and our staffs are talking to see if there is a way to address these concerns.”

We hope that in 2016 the CFTC, bank regulators and the BCBS will collaborate to resolve the unintended consequences of the leverage ratio in order to avoid discouraging (at best) the salutary effects of clearing.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.