The volume of acquisitions involving broker-dealer firms continues to increase as the industry experiences further consolidation and realignment. In 2015, the Financial Industry Regulatory Authority (FINRA) proposed a rule that would clarify prior guidance regarding the legal and regulatory framework applicable to the transfer of customer accounts between broker-dealer firms. The customer accounts of any broker-dealer firm — and the trading and other transactions that are conducted through such accounts — generate the core revenues for most broker-dealers. For that reason, the success of any transaction depends on ensuring that the transfer of customer accounts is carried out properly and effectively.

FINRA, which serves as the principal self-regulatory body for U.S. broker-dealer firms, generally requires broker-dealers to obtain affirmative written consent before transferring a customer’s account to another broker-dealer. In most broker-dealer M&A transactions, however, seeking and obtaining the affirmative written consent of each customer would be impracticable, given that a broker-dealer of significant scale may have thousands — or tens of thousands — of customers.

FINRA’s Prior Guidance

In response to concerns raised by practitioners regarding the transfer of customer accounts “in bulk” — including in the context of an M&A transaction — the National Association of Securities Dealers (NASD), which was the predecessor to FINRA, published Notice to Members 02-57 (2002). In that notice, the NASD staff confirmed its general view that a transfer of a customer account to another broker-dealer requires the affirmative consent of the customer, but prescribed several circumstances — including an acquisition or merger of a member firm — in which broker-dealers could consider a customer to have provided consent even if the customer did not provide its affirmative consent in writing.

The NASD staff acknowledged that, in the context of an acquisition or merger of a member firm, a customer’s consent could be obtained if the transferor broker-dealer notifies a customer that the broker-dealer intends to transfer the customer’s account, and the customer fails to object after some appropriate period of time. This manner of consent is commonly referred to as “negative consent.”

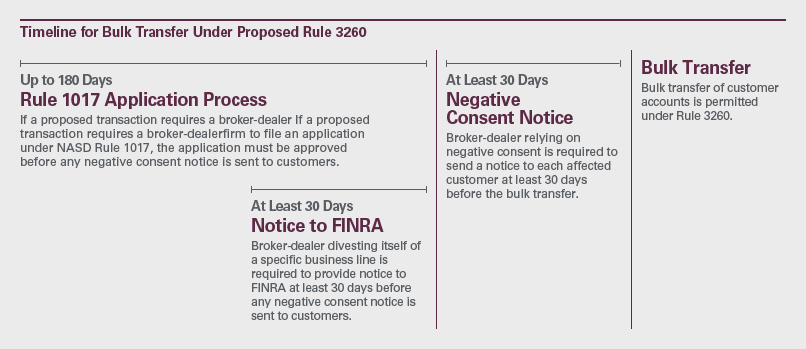

In an M&A transaction, the negative consent process affords speed and efficiency in obtaining customer consents and predictability of overall transaction timing. Broker-dealers using a negative consent process commonly request that customers provide any objection to the proposed transfer within at least 30 days of the customer’s receipt of notice. (Given that almost all brokerage agreements can be terminated on short notice, a customer could at any time elect to terminate its account with the acquirer broker-dealer and transfer its account to a different broker-dealer.) By setting a deadline of at least 30 days, the parties in an M&A transaction can attain certainty regarding the length of time it may take to obtain the customer consents necessary to consummate the transaction. Negative consent would not be permitted if the terms of the agreement between the broker-dealer and the customer expressly require the customer’s written consent for the assignment of the contract. In our experience, however, brokerage customer agreements do not normally require written consent for such purposes.

FINRA’s Proposed Rule

In June 2015, FINRA proposed Rule 3260, which would codify certain of its prior guidance regarding the use of negative consents, including in the context of M&A transactions involving a broker-dealer. If adopted, Rule 3260 would permit a broker-dealer to rely on negative consents to effect a bulk transfer of customers’ accounts when the broker-dealer is:

- divesting itself of a specific business line;

- merging with another broker-dealer; or

- being acquired by another broker-dealer.

If adopted, the rule would codify for the first time FINRA’s guidance regarding the use of negative consent to transfer accounts in bulk.

Conditions for Use of the Negative Consent Procedure

30-Day Notice Requirement

Rule 3260 would require a broker-dealer relying on negative consent to send a notice to each affected customer at least 30 calendar days before it effects the bulk transfer. The notice would be required to contain the following elements:

- a brief description of the circumstances necessitating the transfer or change in broker-dealer of record;

- a statement that the customer has the right to object to the transfer or change, and the date by which the customer must respond if such objection is to be made (at least 30 calendar days after the letter is sent);

- information on how the customer can effectuate a transfer or change in broker-dealer of record to another firm;

- disclosure of any costs to the customer if the customer initiates a transfer of the account or change in broker-dealer of record after the account is moved or the broker-dealer of record has been changed; and

- a statement regarding the broker-dealer’s compliance with SEC Regulation S-P (Privacy of Consumer Financial Information) in connection with the transfer or change in broker-dealer of record.

Prohibition Against Charging Transfer Fees

Rule 3260 would not permit a broker-dealer that utilizes a negative consent to charge a fee for the related transfer of a customer’s account. In addition, the broker-dealer would be prohibited from charging a fee to a customer who, in response to receiving a notice, decides to move his or her account to another broker-dealer during the allowed opt-out period.

Special Requirements for Divestments of a Line of Business

If a broker-dealer is divesting itself of a specific business line, Rule 3260 would require the broker-dealer to provide a letter to FINRA (at least 30 days prior to sending customers the notice letter pursuant to which negative consent is sought), along with any legal agreements entered into with the receiving broker-dealer detailing the terms of the transfer of accounts.

Additionally, Rule 3260 would provide that, if the broker-dealer seeks to effect a bulk transfer of customers’ accounts because of a divesture:

- the accounts can only be transferred to one introducing or clearing broker-dealer;

- the accounts subject to transfer must be currently held at a clearing broker-dealer that is a FINRA member, whether or not the transfer of the accounts will result in a change in clearing broker-dealer;

- the transfers cannot occur until there is a fully executed agreement between the divesting and receiving broker-dealer; and

- the transfers can only be to entities that are permitted, due to the nature of their registration with the appropriate regulatory authorities, to service the accounts transferred.

Transactions That Require Rule 1017 Applications

If a proposed divestiture, acquisition or merger requires one or more of the broker-dealer firms involved in the transaction to file an application with FINRA under NASD Rule 1017 (see 2015 Insights article “Broker-Dealer M&A Transactions: Toward a More Accommodating Regulatory Process”), the application must be approved before the applicable firm sends the notice pursuant to which negative consent is sought under Rule 3260. The 30-day period described above would begin to run after the completion of the period required for Rule 1017 approval, and as a result, the total time for the approval of that application and the subsequent notice and waiting period for obtaining negative consent would be at least three months and as much as six months (or longer).

Conclusion

As M&A transactions involving broker-dealers become more frequent, participants in these transactions are placing greater emphasis on the rules governing the bulk transfer of customer accounts. Once implemented, Rule 3260 would provide participants with clear rules and expectations for the treatment of customer accounts in such transactions. We expect that these rules would ultimately enhance the efficiency of broker-dealer M&A by allowing participants to more accurately assess and more effectively plan for the execution risk and conditionality of such transactions.

Former counsel David E. Barrett and former associate Jonathan A. Dhanawade contributed to this article.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.