Connecticut has implemented changes to its transfer tax and probate laws that affect nearly every decedent leaving even a modest estate via will or nonprobate transfer (such as a revocable trust). A new $20 million cap for transfer taxes places a limit on how much estates and cumulative gifts can be taxed, but a change in probate fees could offset any tax savings realized.

The new system for calculating probate fees in Connecticut is in stark contrast to its counterparts in New York and New Jersey, creating significant disparities in court costs between otherwise similarly situated tri-state area neighbors. As more fully explored below, Connecticut's new probate fees rise indefinitely based on the value of a decedent's estate and are no longer subject to a $12,500 cap. Although probate fees in New York increase with the size of a decedent's estate, they are capped at $1,250 for any estate valued at or over $500,000. New Jersey's probate fees are technically uncapped but increase based on the length of the decedent's will — $100 for the first two pages and $5 for each page thereafter — and are not based on the value of the underlying probate estate. Connecticut's system imposes the highest cost on families of both moderate and substantial means.

$20 Million Estate and Gift Tax Caps

Estates of both resident and nonresident decedents dying on or after January 1, 2016, are subject to an estate tax of no greater than $20 million, regardless of the size of the estate. The tax on estates of decedents dying between January 1, 2011, and January 1, 2016, is not subject to a cap. This means that a $500 million estate of a decedent dying on July 31, 2015, would be subject to an estate tax of $59.5 million — $39.5 million more than the $20 million cap now in place.

Connecticut’s gift tax — the only state-level tax on gifts in the country — also is subject to the $20 million cap for gifts made on or after January 1, 2016. The amount of gift tax paid during an individual's life continues to credit, on a dollar-for-dollar basis, the amount of estate tax payable at death. For example, the estate of an individual who paid $5 million in gift tax during his or her life would have a maximum estate tax liability of $15 million under the cap.

With both caps in place, the total amount of estate and gift tax payable for transfers made on or after January 1, 2016, by decedents who die on or after that date cannot exceed $20 million. The combined caps will help those with high net worth plan accordingly and limit their exposure to transfer tax liability.

Unlimited Probate Fees

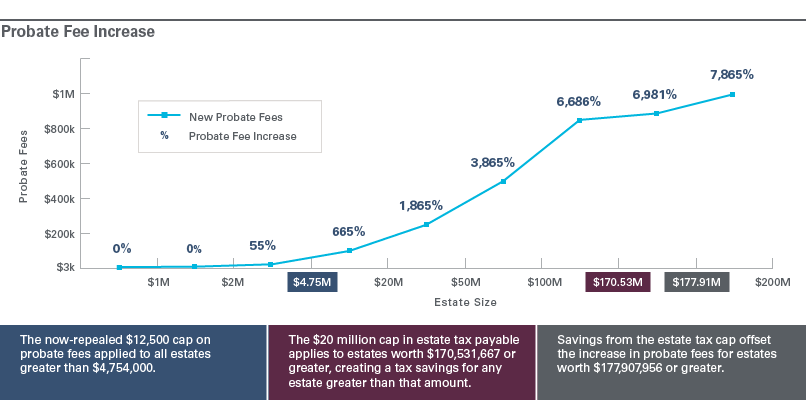

Probate fees in Connecticut were subject to a $12,500 cap for any estate over $4.7 million until 2015, when the state legislature passed and Gov. Dannel P. Malloy signed into law a budget that cut all funding for the state's probate system. Probate fees now increase proportionally with the size of a decedent’s estate.

Uncapped probate fees, retroactively applying to the estates of decedents who died on or after January 1, 2015, will ostensibly make up the $32 million budget shortfall over the next two years. The new probate fees are $5,615 plus 0.5 percent of the decedent's gross estate exceeding $2 million. (Under Connecticut and federal law, the decedent's gross estate is calculated before taking marital, charitable or other deductions into account.)

For all but the wealthiest decedents, the significant increase in probate fees outweighs the tax savings provided by the estate tax cap. The estate tax cap legislation did not decrease estate tax rates, meaning that decedents with estates under $170.5 million will pay the same estate tax regardless of the decedent's date of death. Conversely, the new probate fee structure increases probate fees for estates as small as $2 million that are subject to probate at any time after January 1, 2015. The savings afforded by the estate tax cap will only offset the increase in probate fees for estates greater than $177.9 million.

The chart below illustrates the magnitude of the new fee structure, which substantially increases probate costs for even modest estates.

On the other end of the spectrum, an estate will incur a filing fee if it has assets of any value titled in the decedent's name and requires a probate court filing of the decedent’s will. Thus, even estates under $2 million that are exempt from paying the estate tax are subject to probate fees. Rather than filing estate tax returns with the Connecticut Department of Revenue Services, these “nontaxable” estates must file the returns directly with the probate court so the court can assess probate fees. Meanwhile, taxable estates file estate tax returns with the Department of Revenue Services and will send the probate court a copy. And estates of a decedent, resident of Connecticut or otherwise, must file an estate tax return with the probate court if any of the decedent’s real or tangible personal property is located in Connecticut. As a result, no matter the value of assets, if an estate needs to probate the decedent's will in a Connecticut probate court, a filing fee will be imposed.

Transfers outside the probate system are unlikely to mitigate the increased costs of probate in Connecticut because transfers in trust and other traditional “nonprobate” transfers may be included when calculating probate fees. The basis for the probate fee calculation is the greater of the gross estate for federal estate tax purposes or the gross estate for Connecticut transfer tax purposes. Regardless of any changes to the calculation for federal tax purposes, the gross estate for Connecticut transfer tax purposes includes all property transferred (a) by will, (b) by intestate succession, (c) in contemplation of death and within three years of the date of the decedent’s death, and (d) where the gift or grant is intended to take effect at the decedent’s death.

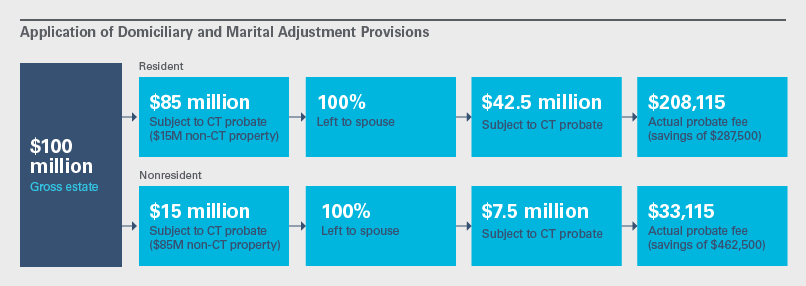

Two aspects of Connecticut probate law relating to domiciliary and marital status mitigate the effect of using a decedent’s entire gross estate to calculate the probate fee. First, only a decedent’s property physically located in Connecticut will factor in the probate fee calculation, whether or not the decedent was a Connecticut resident. Second, a decedent’s gross estate for purposes of calculating the probate fee is subject to reduction if any part of the gross estate will pass to the decedent’s surviving spouse. Any portion of the decedent’s gross estate that passes to the surviving spouse is included in the probate fee calculation at half of its fair market value.

Other common deductions for federal and state estate tax purposes, including charitable deductions, do not factor in the calculation of probate fees and will not reduce the amount due to the probate court.

Looking Ahead

Connecticut’s new estate and gift tax caps offer significant savings for very wealthy decedents who have made substantial amounts of taxable gifts during life and for large estates at death. However, the general increase in probate fees — which, unlike the estate tax, affects all who transfer property at death in Connecticut — adds complexity and creates an additional need for planning. Regardless of their personal states of residency, all individuals owning property located in Connecticut should consider the costs of probate under the new fee structure when crafting an estate plan that meets their needs.

The authors of this article are not admitted to practice in Connecticut. This article is for general informational purposes only.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.