Deutsche | Français | 中文 | 日本語 | 한국어

After significant deliberation and discussion, Congress passed and the president is expected to shortly sign the Foreign Investment Risk Review Modernization Act of 2018 (FIRRMA),1 the first legislation in over a decade to reform national security reviews through the Committee on Foreign Investment in the United States (CFIUS). The resulting legislation will, in large part, codify certain CFIUS regulations and practices of the past several years. But FIRRMA also expands CFIUS’ jurisdiction to cover several previously uncovered transactions, most notably over certain noncontrolling transactions. In addition, FIRRMA provides statutory clarification of CFIUS’ jurisdiction over private investment funds. The legislation also ushers in a number of administrative changes, including updates to review timing, the authorization of filing fees and — in significant departures from current requirements — mandated short-form filings for certain foreign investments and annual disclosures of filers and outcomes of CFIUS cases involving long-form notices. Finally, FIRRMA provides a statutory pathway for judicial review and acknowledges the advent of multilateral national security reviews of cross-border investments.

FIRRMA also expands CFIUS’ jurisdiction to cover several previously uncovered transactions, most notably over certain noncontrolling transactions.

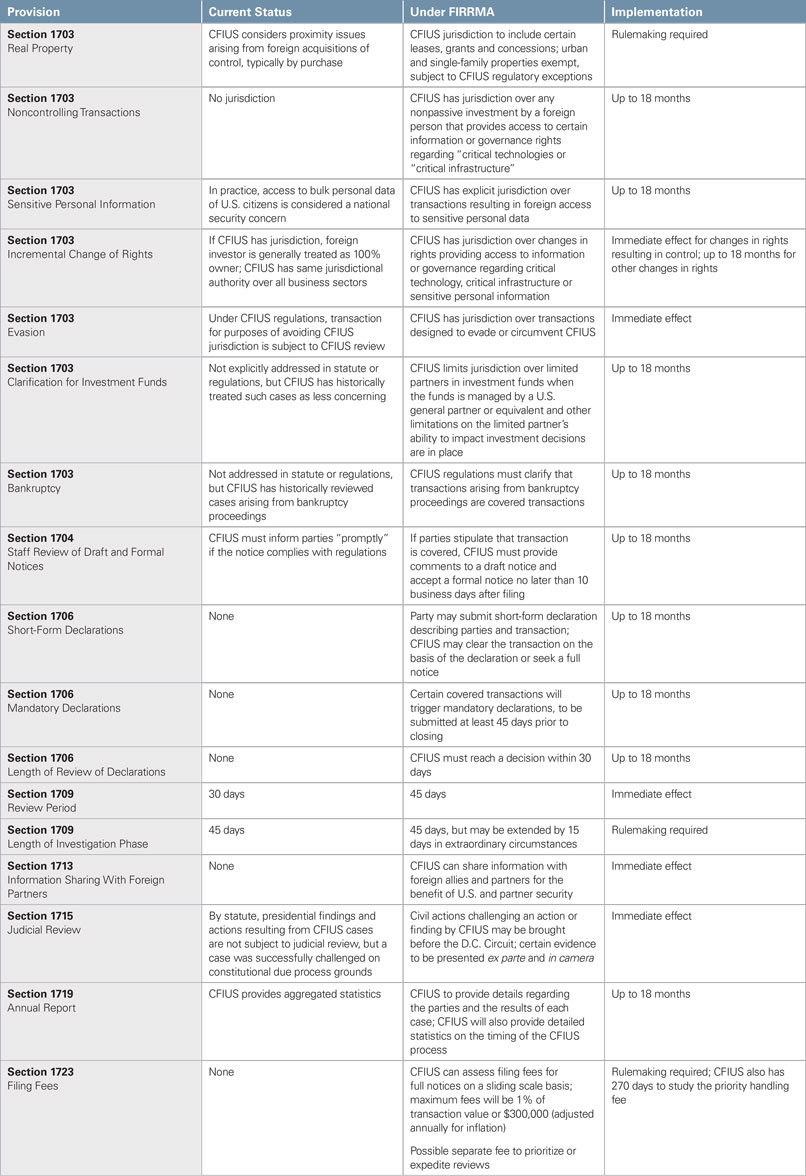

The practical results of most of these provisions will not be seen for up to 18 months, as CFIUS has been granted that time to engage in formal rulemaking to implement many of these changes. Some changes, however, come into effect immediately. The table below summarizes the new provisions and when they will take effect.

Expansion of CFIUS Jurisdiction

Codification of Existing CFIUS Practice and Incremental Jurisdictional Expansion

CFIUS jurisdiction extends only to “covered transactions,” generally defined until now as transactions that could result in foreign control of a U.S. business. In several ways, FIRRMA largely codifies what has become CFIUS’ interpretation of previous authorities and provides marginal expansion of its jurisdiction, but likely not in ways that will radically change CFIUS’ practices.

Real Estate

CFIUS has historically scrutinized transactions in which a foreign party seeks to purchase real estate that is sensitive for national security reasons because it houses sensitive tenants or is in proximity to sensitive sites such as U.S. military installations and training areas. FIRRMA codifies CFIUS’ jurisdiction to review the purchase of U.S. business-owned real estate while also expanding CFIUS’ jurisdiction to include leases and other real estate transactions as well as purchases of vacant land (i.e., true “greenfield” investments). Subject to exceptions to be defined in regulations, the new provisions omit single housing units and properties in certain urbanized areas and no longer include real estate transactions that involve proximity to land ports (i.e., border crossings), as had been previously proposed by some lawmakers. CFIUS is authorized to issue regulations narrowing the scope of these new real estate provisions to investors from certain countries.

Sensitive Personal Data

CFIUS has in recent years also heavily scrutinized transactions in which a foreign party could gain access to personal information of U.S. citizens, especially when it is in bulk form. FIRRMA codifies CFIUS’ jurisdiction over transactions that provide investors access to the sensitive personal data of U.S. citizens, with specifics to be defined in CFIUS regulations.2

Definition of US Business

FIRRMA also broadens the definition of a U.S. business — the key asset that must be involved in order for CFIUS to have jurisdiction — by requiring merely that it be a person “engaged in interstate commerce” in the U.S. This approach eliminates some prior elements of the U.S. business definition, although in practice CFIUS was routinely aggressive in its interpretation of what constitutes a U.S. business.

Significant Expansion of CFIUS Jurisdiction Over Noncontrolling Investments

In its most significant jurisdictional expansion, FIRRMA now provides CFIUS authority to review transactions that are not “controlling” investments — an increasing area of concern in the executive and legislative branches.3 Although CFIUS has long aggressively interpreted what constitutes a “controlling” and hence covered transaction,4 FIRRMA expressly provides that certain smaller, noncontrolling investments will fall within CFIUS’ jurisdiction. Such noncontrolling investments only apply in cases in which the foreign acquirer is investing in a U.S. business that involves “critical technologies,” “critical infrastructure,” or “sensitive personal data of U.S. citizens.” This significant expansion will, however, only apply to countries specified by subsequent CFIUS regulations, which should — according to FIRRMA — “limit the application” of this jurisdictional expansion to countries of particular concern.

Largely consistent with current CFIUS regulations, FIRRMA also provides further definition of “critical technologies,” principally centered on restrictions imposed by the Commerce (Export Administration Regulations) and State (International Traffic in Arms Regulations) departments. In addition, FIRRMA calls on CFIUS to develop regulations narrowly interpreting a broad statutory definition of “critical infrastructure.” With respect to personal data of U.S. citizens, we expect CFIUS will continue to focus — as it previously has — on financial services, health care and insurance information, as well as other consumer data.

Although CFIUS will engage in further rulemaking to clarify how these provisions will work in practice, we expect this aspect of FIRRMA to have a potentially significant impact on deal structuring. Not only does this aspect of FIRRMA create an entirely new area of jurisdiction, it will — in certain cases — also limit the use of a common phased-structuring of transactions in which a foreign buyer immediately acquires 9.9 percent of a U.S. business but then pauses further investment or governance rights pending CFIUS approval. In cases involving this jurisdictional expansion, such an approach would be problematic given even the initial investment would constitute a covered transaction.

Limitation of CFIUS Jurisdiction Over Certain Investment Funds

In a major win for U.S. private equity managers, FIRRMA clarifies that in investment funds, limited partners may qualify as passive investors when certain conditions are met, including: (i) the fund being managed by a U.S. general partner or equivalent and (ii) limitations on the ability of the limited partner to impact certain investment decisions whether through the advisory board, a committee or some other form of authority.

Specifically, as set forth in FIRRMA, in order to be classified as a passive investor, the limited partner must meet the following criteria:

- The fund is managed exclusively by a general partner, a managing member or an equivalent who is not a foreign person;

- If the limited partner serves on an advisory board or committee: (i) the advisory board or committee does not have the ability to approve, disapprove or otherwise control investment decisions of the fund or decisions made by the general partner, managing member or equivalent related to entities in which the fund is invested; and (ii) the foreign person does not have access to material nonpublic technical information as a result of its participation on the advisory board or committee; and

- The foreign person does not otherwise have the ability to control the fund, including the authority (i) to approve, disapprove or otherwise control investment decisions of the fund; (ii) to approve, disapprove or otherwise control decisions made by the general partner, managing member or equivalent related to entities in which the fund is invested; or (iii) to unilaterally dismiss, prevent the dismissal of, select or determine the compensation of the general partner, managing member or equivalent.

Although CFIUS had historically treated investment funds with U.S. general partners and foreign limited partners with traditional rights as less concerning than other forms of investment, in recent years the committee had become much more aggressive asserting jurisdiction over investments by such funds. FIRRMA’s provisions relating to investment funds may represent a congressional determination that such funds are an important method for facilitating foreign investment in a manner that is less problematic for national security purposes.

Changes to the CFIUS Process

FIRRMA introduces a number of administrative changes to the CFIUS process, including adjustments to the CFIUS timeline, the establishment of filing fees and the creation of short-form summary filings that in some cases will be mandatory. CFIUS will also disclose, as part of its annual report, more details about CFIUS reviews, including the parties to CFIUS notices and the results of each CFIUS case.

Timing

Prior to FIRRMA, CFIUS operated under a statutory time frame that included a 30-day initial review period and, when necessary, a second-stage 45-day investigation stage. Under FIRRMA, CFIUS will immediately expand the initial review phase from 30 days to 45 days and also allow a potential 15-day extension of the second-stage investigation phase (currently 45 days) in extraordinary circumstances to be defined in regulations.

In addition, when parties stipulate that a transaction is subject to CFIUS jurisdiction, CFIUS must provide comments on the draft CFIUS notice and accept the formal notice within 10 business days after submission. This provision may not take effect for up to 18 months, by which time CFIUS is expected to have the necessary resources in place to speed the current intake process.

These provisions seek to minimize two factors contributing to the growing length of the CFIUS process. The 10-day comment and acceptance periods cap the previously unregulated intake period, and the longer review and investigation periods are intended to obviate the frequent need for withdrawals and refilings of CFIUS notices to “restart the clock.”

Filing Fees

FIRRMA grants CFIUS the ability to impose a new filing fee, which will be based on a sliding scale to be established in regulations. The fee cannot exceed the lesser of 1 percent of the transaction value or $300,000 (adjusted annually for inflation). CFIUS will need to work within appropriations guidelines and engage in formal rulemaking to determine the precise fee structure.

Short-Form Declarations

Under FIRRMA, foreign investors who believe they are pursuing less sensitive transactions will be permitted to submit a shorter (five pages or less) “declaration” to potentially gain a faster response from CFIUS. Following submission of the new declaration, CFIUS will have 30 days to respond, either by clearing the transaction, seeking (by request or by suggestion to the parties) a full notice of the transaction or by initiating a unilateral review of the transaction if the parties are uncooperative. Notably, CFIUS filing fees are not required for declarations, making them a less expensive option for obtaining CFIUS clearance of transactions unlikely to raise national security concerns.

Certain covered transactions will trigger the filing of mandatory declarations at least 45 days prior to closing. A declaration will be required if the transaction is a covered transaction, a foreign government has a substantial interest in the foreign investor and the U.S. business involves critical technology or infrastructure. CFIUS regulations will be required to implement the new declaration provisions of FIRRMA. Specifically:

- The information to be provided in declarations must be specified;

- CFIUS must engage in further rulemaking to augment the definition of “substantial interest” for this section, including considerations of potential influence through board membership, ownership interests and shareholder rights; and

- CFIUS will also have discretion to require declarations for certain other covered transactions related to critical technologies.

CFIUS may waive the declaration requirement for parties able to demonstrate that (i) the foreign investor is not controlled by a foreign government and (ii) the foreign investor has a history of cooperation with CFIUS. Parties failing to file a declaration when it is mandatory may face penalties under the new rules. Alternatively, parties may elect to submit a full notice in lieu of a mandatory declaration.

FIRRMA’s establishment of mandatory declarations reverses prior CFIUS authorities in which, with extremely rare exceptions, the CFIUS process was nominally voluntary. The requirement is the embodiment of Congress’ frustration with certain transactions not being brought to CFIUS’ attention.

Increased Transparency of Process

FIRRMA requires a substantial increase in the level of disclosure required in CFIUS’ annual report to Congress. The report, which historically has focused on aggregated statistics, will now list details on each CFIUS case involving a full CFIUS notice, including, “basic information” on the parties (presumably including their identities) and the results of the case. Aggregated information on declarations will also be included in the report. The report will also track CFIUS’ handling of cases, including the time required to comment on draft notices and accept formal notices, and the length of time required to complete reviews and investigations.

These changes to the annual report do not take immediate effect, but when implemented, they will greatly increase the transparency of the CFIUS process and may cause CFIUS to treat cases identified in annual reports as precedents for its handling of future transactions. However, CFIUS has been notorious for failing to issue its annual reports on a timely basis, so the benefits of these changes will be diluted unless Congress requires CFIUS to be more diligent.

Expansion of CFIUS Resources

According to the Government Accountability Office, between 2011 and 2016, CFIUS reviews have increased by 55 percent while CFIUS staff has increased by only 11 percent. The CFIUS caseload increased even more during 2017 and remains heavy in 2018.

FIRRMA addresses this issue in a number of ways. To provide additional resources to augment CFIUS staff, Congress has authorized the appropriation of $20 million per year for the next five fiscal years to seed a fund supporting CFIUS. This fund will also receive the CFIUS filing fees described above. In addition, FIRRMA creates two additional positions of assistant secretary of the treasury, to be appointed by the president. These new officials will help bolster senior-level engagement by the Department of the Treasury in its position as CFIUS chair.

To address resource constraints within the U.S. Intelligence Community, which provides foreign threat assessments to CFIUS for each case, the director of National Intelligence (DNI) is authorized to provide an abbreviated threat analysis when a transaction (i) is a covered real estate transaction, (ii) involves foreign investors who filed CFIUS notices within the past 12 months, or (iii) meets other conditions approved by CFIUS and the DNI. This provision may be particularly helpful to repeat CFIUS filers submitting short-form declarations.

Creation of Pathway for Judicial Review of CFIUS

FIRRMA provides for judicial review of CFIUS actions and decisions. Civil actions challenging CFIUS may be brought before the U.S. Court of Appeals for the District of Columbia Circuit, and FIRRMA includes provisions for the handling of classified, privileged and other protected information. FIRRMA does not eliminate the existing prohibition against judicial review of presidential actions and findings resulting from CFIUS cases, but as shown by the D.C. Circuit’s 2014 decision in Ralls Corp. v. CFIUS,5 presidential and CFIUS actions can be challenged on constitutional grounds. It is possible that once CFIUS promulgates regulations implementing FIRRMA’s provisions, future litigation could challenge those rules or their application.

Acknowledgment of Importance of National Security Reviews in Other Countries

FIRRMA calls for the president to “conduct a more robust international outreach effort” to help allies and other partners establish procedures similar to those employed by CFIUS. To that end, FIRRMA instructs the CFIUS chair to establish a formal process for information sharing with allies and other U.S. partners. This provision, once implemented, will address current limitations resulting from CFIUS confidentiality requirements and better enable CFIUS to inform its decisions using input from foreign government partners. Moreover, with stronger foreign review processes and greater information sharing, CFIUS will be able to participate in coordinated, multilateral national security reviews of multinational cross-border investments. This provision embodies — and will likely accelerate — a trend that has emerged over the past several years: deeper communication and cooperation in national security reviews, especially among the United States, the United Kingdom, Canada, Australia, France and Germany.

Widely Discussed Proposals Not Included in FIRRMA

While FIRRMA includes several novel provisions, some of the more sweeping reforms that lawmakers, industry representatives and other stakeholders had been discussing for over a year were ultimately abandoned:

- Proposed restrictions on foreign joint ventures aimed at reducing outflows of U.S. technologies were not included in FIRRMA. However, CFIUS continues to have jurisdiction over joint ventures in which the foreign partner is deemed to be acquiring control over a U.S. business.

- CFIUS is no longer required, as previously proposed, to define and restrict investments in “emerging technologies.” Recognizing that this would cause an untenable overlap with existing export control regimes, Congress instead passed the Export Control Reform Act of 2018, which establishes a new process, led by the Department of Commerce with support from the Department of Defense, to identify and protect emerging technologies.

- “Countries of special concern,” defined in earlier drafts of FIRRMA as including China and Russia, are not subject to more stringent statutory requirements in law as enacted. However, FIRRMA includes a “sense of Congress” statement expressing concerns with such countries, and CFIUS’ annual report must include a section on Chinese investment. In practice, CFIUS has demonstrated its intent to carefully scrutinize and limit transactions involving China and Russia; this is unlikely to change.

Summary of Key FIRRMA Provisions

The following is a nonexhaustive summary of key provisions within FIRRMA and when they take effect. In general, FIRRMA provisions generally take effect either:

- immediately upon FIRRMA’s enactment, or

- the earlier of (i) 18 months after FIRRMA’s enactment or (ii) after CFIUS has determined that the necessary regulations, organizational structure, personnel and other resources necessary to implement the provisions have been put in place.

Given the complexity of FIRRMA, the need for additional resources, the difficulties in issuing regulations on a piecemeal basis and the length of time it took CFIUS to issue regulations after the law was last changed in 2007, we expect to wait until Congress’ 18-month deadline before such provisions take effect. This will also apply to certain provisions that, although part of sections of FIRRMA that take immediate effect, require the issuance of definitions or other implementing regulations.

_______________

2 The legislation also codifies CFIUS’ jurisdiction over certain transactions in which it already regularly asserts jurisdiction pursuant to regulation or as a matter of practice. These include transactions arising from bankruptcy proceedings and transactions that appear designed to fraudulently avoid CFIUS review.

3 Exemplifying this concern was the January 2018 report by the Defense Innovation Unit Experimental that explored the risk of Chinese investment in venture financing of early-stage technology companies. See China’s Technology Transfer Strategy: How Chinese Investments in Emerging Technology Enable a Strategic Competitor to Access the Crown Jewels of U.S. Innovation at 3 (Michael Brown and Pavneet Singh, 2018).

4 As a general matter, CFIUS has deemed to be “controlling” any equity ownership of (i) more than 9.9 percent or (ii) less than 9.9 percent if other indicia of control exist (e.g., the foreign investor can appoint even a single board member) beyond standard minority investment protections such as tag-along, drag-along and anti-dilution rights.

5 Ralls Corp. v. Committee on Foreign Investment in the United States, 758 F.3d 296 (D.C. Cir. 2014).

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.