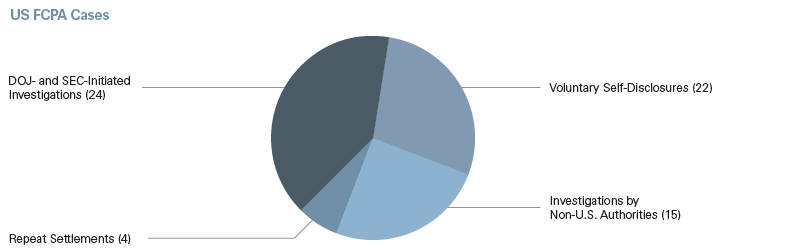

There have long been questions as to how the Department of Justice (DOJ) and Securities and Exchange Commission (SEC) begin their Foreign Corrupt Practices Act (FCPA) cases. We have analyzed 65 publicly reported FCPA corporate resolutions by the DOJ and SEC from January 2015 to the present and grouped the cases into three general categories:

- voluntary self-disclosure cases, which constitute just over one-third of settled FCPA matters during the time period;

- DOJ- or SEC-initiated investigations, which constitute the plurality of settled FCPA matters from this period; and

- investigations initiated by authorities outside the U.S. and that the DOJ or SEC joined, which have significantly increased over the past three years.

In addition, four of the publicly disclosed resolutions in the period are repeat settlements in which the DOJ and SEC noted either a breach of a prior agreement or focused on conduct similar to the prior violations. As set forth with examples here, we have identified certain general trends that provide guidance to in-house lawyers, C-suite executives, audit committees and boards in considering their investigation, disclosure and remediation strategies when faced with a potential anti-corruption compliance issue.

Voluntary Self-Disclosures

Of the published settlements since January 2015, 22 were described by the DOJ and SEC as voluntarily self-disclosed to U.S. law enforcement prior to an imminent threat of investigation. We recognize that the public settlements do not account for cases that were voluntarily disclosed and not pursued by authorities or closed without a public declination. Nevertheless, the analysis reflects that two-thirds of cases that are serious enough to proceed to a settlement do not come from voluntary disclosures.

In addition:

- On balance (though with a few exceptions), voluntary disclosure cases involve smaller payments and lower profits than cases initiated by U.S. or non-U.S. authorities.

- In a number of voluntary disclosure cases, the DOJ has entered into Non-Prosecution Agreements (NPAs) or declinations of prosecution. Consistent with DOJ’s FCPA corporate enforcement policy announced in November 2017, recent DOJ declinations have required disgorgement of profits from the improper conduct. SEC resolutions similarly provide credit for self-disclosure.

- Voluntary disclosure cases frequently involve active remediation by the disclosing company and, as a result of self-disclosure and remediation, are less likely to result in the appointment of an independent external monitor.

DOJ- and SEC-Initiated Investigations

Through their own investigative efforts or based on whistleblower or other sources (but not the putative defendant company itself), the plurality of settled cases come from investigations initiated by the SEC and DOJ, a total of 24 cases. Of these, seven involved settlement agreements with both the DOJ and SEC, 14 involved settlements with the SEC only (and either no action by the DOJ or an express declination), and three involved settlements with the DOJ only.

In settlements involving both the SEC and DOJ, the SEC either sought only disgorgement of profit (with prejudgment interest), or disgorgement and a civil penalty but deemed the civil penalty satisfied by a criminal fine paid to the DOJ (such as the settlements with PTC/Parametric Technologies, Credit Suisse and Och-Ziff). In SEC-only matters, the SEC frequently sought both a civil money penalty and disgorgement of profits (such as the settlements with Johnson Controls, Anheuser In-Bev, BHP Billiton and Mead Johnson).

For cases that were serious enough to proceed to DOJ enforcement action in this category, the majority of matters were resolved with a deferred prosecution agreement (DPA) or parent DPA and subsidiary guilty plea. In these investigations, the DOJ is becoming increasingly transparent about the level of credit granted for cooperation, with a 25 percent discount from the low end of the U.S. Sentencing Guidelines range provided for full cooperation (as defined by the DOJ). Unsurprisingly, these cases also included more onerous post-settlement compliance reporting obligations or independent monitoring than voluntary disclosure cases.

In addition:

- Although U.S. officials have spoken publicly about no longer conducting “industry sweeps,” several of the settlements in this category are the result of general inquiries to companies in a specific industry sector. For example, the DOJ- and SEC-initiated investigations to assess whether financial institutions provided jobs or other benefits to relatives of Chinese government officials to secure mandates, which led to broader review of practices in this area. Similarly, the SEC examined practices relating to financial institutions’ business development with sovereign wealth funds, also leading financial institutions to review their policies and practices in this area.

- Regardless of whether the term “sweeps” is used, the DOJ and SEC continue to pursue leads from ongoing investigations, which frequently implicate more than one company in an industry sub-sector and geography. Such investigations underscore the importance of continued risk assessments and enhancements to compliance programs, including ensuring familiarity with the investigations and enforcement actions in a company’s specific industry and places of operation.

- Several investigations resulted from whistleblower reports made to the DOJ and SEC. In some instances, the whistleblowers had first contacted the subject company and the company had initiated an internal investigation but had not voluntarily self-disclosed the issue to the DOJ and SEC. In such matters, companies that provided full cooperation to the DOJ received credit for doing so. However, the DOJ and SEC also noted instances in which a company’s initial investigation was insufficiently thorough or robust, or in which disclosures to the agencies were incomplete, and accordingly settlement terms were more stringent. These matters emphasize the care with which a company, its board and its advisers should consider the initial scope of an internal investigation and the decision of whether to make voluntary disclosures, given that regulators have a high level of sophistication when evaluating a company’s response to whistleblower issues.

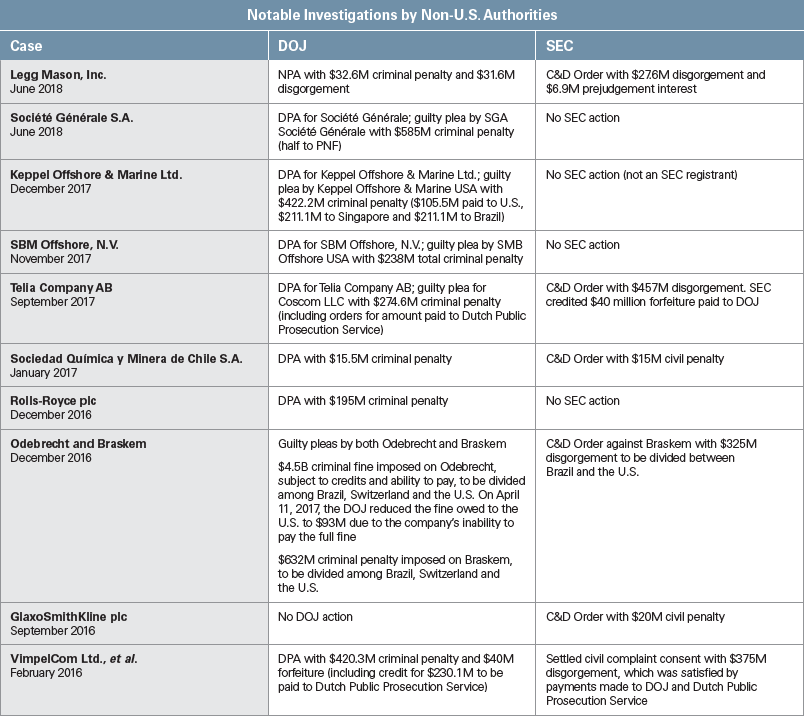

Investigations by Non-U.S. Authorities

There has been a significant increase in enforcement of anti-corruption laws by non-U.S. authorities, resulting in several multijurisdictional investigations that each involve multiple companies and individuals. We have grouped DOJ and SEC enforcement actions into this third category (as opposed to the second category above) where publicly available information indicates that the investigations were initiated by authorities outside of the United States. The Brazilian Lava Jato investigation, for example, has resulted to date in four settlements that include U.S. authorities (Odebrecht and Braskem, SBM, Keppel and, most recently, Petrobras). In the pharmaceutical sector, well-publicized investigations of Glaxo-Smith Kline by Chinese authorities led to inquiries by U.S. authorities to several pharmaceutical companies operating in China. While both the DOJ and SEC are reported to have been involved in the investigations of the matters, the SEC took the lead in settlements and the DOJ largely declined prosecutions (for companies including Mead Johnson, AstraZeneca and Bristol Myers-Squibb). Even where investigations began outside of the U.S., the experience of U.S. authorities and the legal theories available to them have resulted in U.S. authorities taking a significant role in resolving large matters. These cases have tended to involve significant penalties, DPAs or guilty pleas and post-settlement monitorship.

Repeat Settlements

Four of the matters in the period involved companies that had previously settled FCPA investigations with the DOJ and SEC. Of these, one was in the oil and gas services sector and three in the medical device sector — two industries that have been significant focuses of anti-corruption enforcement. The DOJ and SEC press releases accompanying these settlements emphasize the government’s emphasis on ensuring compliance with each company’s initial post-settlement obligations, and three of the four repeat settlements imposed post-settlement independent monitoring.

Remediation

Remediation remains an important issue in the structure of resolutions. The DOJ and SEC take as a baseline that a company subject to investigation will carefully review its existing compliance program and make enhancements to policies, procedures and personnel to address any weaknesses. Our analysis of settlements indicate that two additional factors are frequently cited as demonstrating a company’s commitment to remedial measures: (1) separation of individuals involved in misconduct; and (2) terminating business relationships with and withholding payments to third parties that facilitated or were implicated in improper payments. The agencies appear to acknowledge the challenges faced by non-U.S. labor and employment laws, and have acknowledged remediation credit not only for termination of employees but also for negotiated separations. As to terminating business relationships, the DOJ and SEC credit actions that put compliance interests ahead of business interests and penalize companies for the inverse.

Conclusion

While government investigations are inherently unpredictable, careful analysis of prior settlements can provide a framework for assessing voluntary disclosure advantages and disadvantages, government cooperation expectations, fine calculations and best-practices remediation. We would be pleased to discuss further any areas of our analysis that are of interest.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.