Background

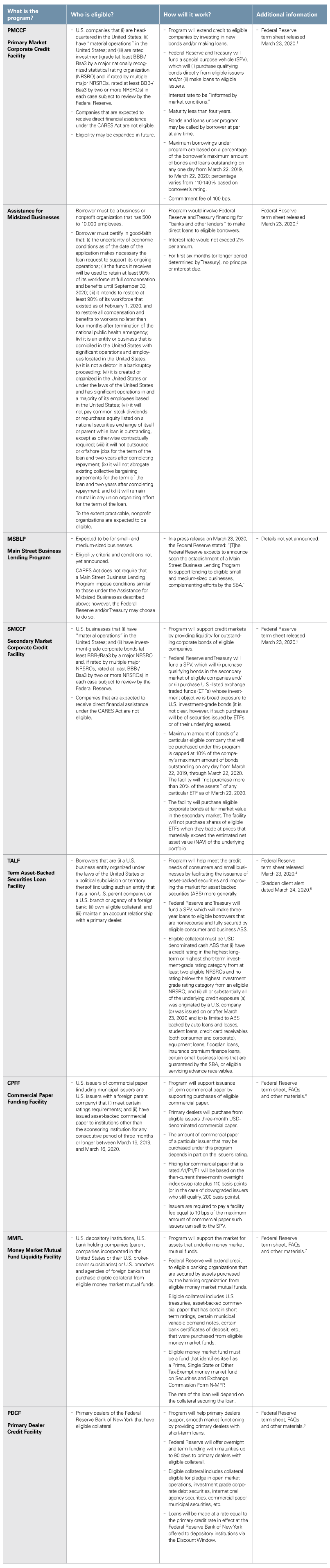

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) became law on March 27, 2020. The economic stimulus package in the CARES Act includes federal funding for business stimulus across three broad categories: (i) grants and direct lending dedicated to specific sectors, such as airlines and national security businesses; (ii) expanded eligibility and payroll support for small businesses through programs administered by the Small Business Administration (SBA); and (iii) Treasury funding for several lending programs administered with the Federal Reserve. More than $450 billion of the allocated funds is directed toward this last category, which is the focus of this summary. The table below summarizes eight programs recently announced, expanded or expected by the Federal Reserve in response to the COVID-19 pandemic.

See all our COVID-19 publications and webinars.

Implementation

The terms of most of these programs are outlined publicly only at a high level through some combination of press release, one-page term sheet or general text in the CARES Act. The CARES Act requires the Department of the Treasury to promulgate regulations by April 6, 2020, to implement some of these stimulus initiatives. However, the Treasury and Federal Reserve face the daunting task of standing up multiple, complex programs, in a short time, with scrutiny and second-guessing both in real time and in hindsight — all while the agency staff are themselves facing challenging work conditions. Thus, we expect the implementation of these programs will be uneven and iterative, with questions and ambiguities being addressed over time rather than in a single set of comprehensive final regulations to be issued in the next week or two.

Generally Applicable Conditions

The lending programs summarized below are generally available only if the recipient is solvent and unable to secure adequate credit from other banking institutions. The Federal Reserve has discretion to make a determination of inadequate credit availability based on generally applicable considerations related primarily to market conditions — rather than on an individual recipient basis.

If a lending program below derives any portion of its funding from Treasury under the CARES Act, then the recipient must be a business that (i) is created or organized in the United States or under the laws of the United States; (ii) has significant operations in the United States; (iii) has a majority of its employees based in the United States; (iv) has not otherwise received adequate economic relief in the form of loans or loan guarantees provided under the CARES Act; and (v) is consistent with certain conflict-of-interest provisions prohibiting participation by entities in which elected federal officials, the heads of executive branch departments or their family members have a controlling influence.

Additional Conditions for Direct Loan Programs

If a lending program below derives any portion of its funding from Treasury under the CARES Act and the program provides “direct loans” (a term defined in the CARES Act), then the recipient must also meet the two additional conditions below.

Prohibition on Certain Buybacks and Capital Distributions. First, the recipient will be prohibited, until 12 months after the loan is no longer outstanding, from (i) repurchasing equity securities of itself or its parent that were listed on a national exchange while the loan is outstanding, except as otherwise contractually required; or (ii) paying dividends or making other capital distributions on common stock.

Limits on Compensation. Second, the recipient must comply with the following compensation limitations until one year after the loan is no longer outstanding.

- An officer or employee of the recipient whose total compensation exceeded $425,000 in calendar year 2019 may not receive (i) total compensation from the recipient during any 12 consecutive month period that exceeds the total compensation that individual received in calendar year 2019 or (ii) severance pay or other benefits upon termination of employment that exceed twice the total compensation that individual received in calendar year 2019. This limitation does not apply to employees whose compensation is determined through an existing collective bargaining agreement entered into prior to March 1, 2020.

- An officer or employee of the recipient whose total compensation exceeded $3 million in calendar year 2019 may not receive total compensation from the recipient during any 12 consecutive month period in excess of the sum of $3 million plus 50% of the total compensation over $3 million the individual received in calendar year 2019.

_______________

1 See https://www.newyorkfed.org/markets/primary-market-corporate-credit-facility

2 See https://www.newyorkfed.org/markets/primary-market-corporate-credit-facility

3 See https://www.newyorkfed.org/markets/secondary-market-corporate-credit-facility

4 See https://www.federalreserve.gov/monetarypolicy/talf.htm

5 See https://www.skadden.com/insights/publications/2020/03/in-response-to-covid-19

6 See https://www.newyorkfed.org/markets/commercial-paper-funding-facility

7 See https://www.federalreserve.gov/monetarypolicy/mmlf.htm

8 See https://www.newyorkfed.org/markets/primary-dealer-credit-facility

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.