On November 15, 2022, the U.S. Securities and Exchange Commission’s (the SEC’s or Commission’s) Division of Enforcement (the Division) released its annual enforcement results discussing enforcement-related actions and key initiatives (the Report).1 Notably, the Report — which covered the fiscal year ending September 30, 2022 (FY 2022) — highlighted that the number of SEC enforcement actions filed in FY 2022 increased by approximately 9% from fiscal year 2021 (FY 2021), including a 6.5% increase in stand-alone enforcement actions over FY 2021. Overall monetary remedies obtained by the SEC (penalties, disgorgement and prejudgment interest) totaled nearly $6.43 billion, the most on record in SEC history and up significantly from approximately $3.85 billion in FY 2021. Of the total money ordered, penalties made up nearly $4.19 billion (also the highest on record), and disgorgement made up approximately $2.24 billion (a 6% decrease from FY 2021).

Division Director Gurbir Grewal noted that the Division is continuing to “protect investors, hold wrongdoers accountable and deter future misconduct in our financial markets.”2 Director Grewal further emphasized that the Division is using every tool available, including significant penalties that have a deterrent effect and are viewed as more than “the cost of doing business.”3

The following summarizes the key metrics for FY 2022, and trends and enforcement priorities described in the Report that we expect to continue in the coming year.

Key Takeaways

- There was an overall increase in the number of SEC enforcement actions and penalties imposed in FY 2022, but a decrease in total disgorgement imposed.

- The SEC is keenly focused on deterring misconduct and relying on a wide variety of tools ranging from increased penalties and tailored undertakings to obtaining admissions and imposing individual accountability (including clawbacks).

- The SEC is increasingly focused on hot-button areas like environmental, social and governance (ESG); crypto assets; cybersecurity; private funds; and complex products.

- Core focus areas, such as issuer disclosures (including non-GAAP disclosures), insider trading/10b5-1 plans and the Foreign Corrupt Practices Act (FCPA), will continue to be priorities for the Division.

FY 2022 by the Numbers

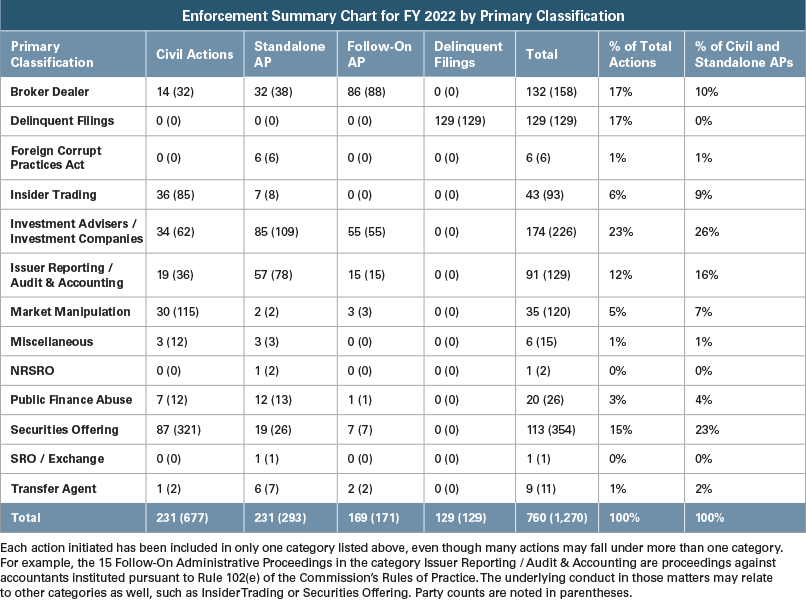

In FY 2022, the Commission brought a mix of 760 enforcement actions.4 The percentage of “stand-alone” actions increased by approximately 6.5% from FY 2021, with a total of 462 stand-alone actions brought in FY 2022. The penalties imposed in FY 2022 also increased to nearly $4.19 billion in FY 2022.5

On the other hand, disgorgement of profits for FY 2022 totaled nearly $2.24 billion, a decrease over the prior fiscal year of approximately 6%.6 This decrease may be attributable, at least in part, to the effect of implementing the new disgorgement parameters following the combination of (1) the 2017 U.S. Supreme Court opinion in Kokesh v. SEC, which held that SEC claims for disgorgement are subject to a five-year statute of limitations, thereby limiting the Commission’s ability to collect disgorgement in long-running cases; (2) the 2020 U.S. Supreme Court opinion in Liu v. SEC, which affirmed the SEC’s power to seek disgorgement as equitable relief, but only if it is for the benefit of harmed investors — not based on joint-and-several liability — and excludes any “legitimate expenses”; and (3) passage of the William M. (Mac) Thornberry National Defense Authorization Act (NDAA) for Fiscal Year 2021, which codified the SEC’s ability to seek disgorgement in federal court and established separate limitations periods for different claims the SEC may bring.7

Similar to FY 2021, stand-alone enforcement actions concerning investment advisers/companies and securities offerings made up the bulk of the SEC’s actions, amounting to approximately 26% and 23%, respectively, of the total 462 stand-alone cases.8 For both categories though, we see a decrease in the percentage compared to FY 2021. A significant number of stand-alone actions brought in FY 2022 also involved issuer reporting/audit and accounting misconduct (16%) and broker-dealer misconduct (10%), an increase over FY 2021 for both categories.9 FCPA cases remained consistent at 1% of the stand-alone actions in FY 2021 and FY 2022.10

The following chart shows the number of cases by category:11

The enforcement statistics for FY 2022 make evident that the Division continues to execute on its mission and is filing an increasing number of actions.

Deterring Misconduct by Focusing On Individual Accountability and Imposing Effective Remedies

Individual Accountability

The SEC continues to stress individual accountability as a “pillar of the SEC’s enforcement program,” especially as it relates to senior corporate officers and other prominent figures within organizations. We expect that focus to continue in the coming years.12 In FY 2022, more than two-thirds of the SEC’s stand-alone enforcement actions involved charges against at least one individual, including the former CEOs of an airline manufacturer and a community bank, as well as the former chief investment officer of a registered investment adviser.13 The SEC also charged several executives under Sarbanes-Oxley (SOX) Section 304, resulting in bonus and compensation clawbacks following alleged misconduct at their firms even though the executives were not personally charged with the misconduct.14 The Division noted that such actions are designed to ensure accountability from senior executives at public companies and incentivize them to prevent misconduct.15

Given the Division’s enforcement results and recent statements by SEC officials, we expect the Division to increasingly seek individual accountability and clawbacks in 2023.

Penalties, Undertakings and Admissions

The Division noted that a “hallmark” of the enforcement program in FY 2022 was robust enforcement through resolutions that “imposed penalties designed to deter future violations, establish accountability from major institutions, and order tailored undertakings that provide potential roadmaps for compliance by other firms.”16

The SEC highlighted the recent off-channel communications sweep involving 16 broker-dealers and an investment adviser for allegedly failing to maintain and preserve work-related text message communications on personal devices, resulting in approximately $1.23 billion in penalties, as an example of these robust enforcement efforts.17 This sweep also involved undertakings by the firms, as well as admissions of wrongful conduct.18 Recent statements by Director Grewal suggest that large attention-getting sweeps that may better educate market participants and deter similar misconduct are likely to continue.19

In the SEC’s action against a multinational, universal bank for an alleged over-issuance of securities, the Commission imposed a $200 million penalty, and required undertakings to implement enhancements to ensure compliance with Section 5 of the Securities Act of 1933 and submit a resulting report to the firms’ board of directors and the SEC staff.20

The Commission’s action against an investment firm for an alleged fraudulent scheme regarding the concealment of downside risks of a complex options trading strategy resulted in more than $1 billion in combined penalties, disgorgement and prejudgment interest, as well as an admission by the firm.21

Robust Enforcement Across Wide Array of Substantive Areas and Market Participants

In FY 2022, the SEC brought actions in a wide variety of substantive areas and against a similarly diverse set of defendants and respondents. These range from trending areas like crypto and ESG to enforcement mainstays like financial fraud/issuer disclosure and market abuses.

ESG

The Commission’s growing emphasis on ESG issues continued in FY 2022. The Division has focused attention on ESG in the context of public companies as well as investment products and strategies. While proposed rulemaking has yet to be finalized, the SEC is relying on existing authority to pursue these actions. The Division brought the following notable actions:

- An action against an investment adviser for, as alleged, materially misleading statements and omissions about its consideration of ESG principles in making investment decisions.22

- A litigated action against a South America-based metals and mining company, in which the SEC alleged that the company made false and misleading claims to local governments, communities and investors about the safety of its dams prior to the collapse of one of them in Brazil, allegedly causing environmental and social harm. The SEC’s complaint pointed out several market and financial factors in alleging that the disclosures were material, including that the dam collapse led to a loss of $4 billion in the company’s market cap, its ADRs lost more than 25% of their value and its credit rating was downgraded to junk status.23

- An action against a robo-adviser for allegedly marketing itself as providing advisory services compliant with Islamic law, but failing to adopt and implement written policies and procedures addressing how it would assure Islamic law compliance.24

Crypto/Cybersecurity

The Division continues to scrutinize the rapidly evolving crypto securities space, as evidenced by the additional resources dedicated to the Crypto Assets and Cyber Unit. Notable actions include:

- an action against a crypto platform for allegedly failing to register offers and sales of a retail crypto-lending product, and, in a first-of-its-kind action against a crypto-lending platform, allegedly violating registration requirements of the Investment Company Act of 1940;25 and

- an action against an individual for allegedly obtaining material nonpublic information in his former role as a product manager at a cryptoasset trading platform and tipping information regarding cryptoasset securities that would be made available for trading on the platform.26

Gatekeepers

The Division’s enforcement metrics demonstrate a growing emphasis on charging gatekeepers that fail to live up to their heightened responsibility in the securities markets. In FY 2022, the SEC brought charges against auditors, transfer agents and lawyers,27 which included:

- an action against an auditor concerning allegations of cheating on the ethics component of CPA exams, resulting in the largest penalty ever imposed by the SEC against an audit firm, in addition to an admission from the firm;28 and

- a settled action against an attorney for his role in an allegedly unregistered, fraudulent securities offering regarding multiple private investment funds.29 The Commission alleged that the lawyer knew or was reckless in not knowing that there was no exemption from registration available for the offerings.30

Private Funds

The growth in the amount of assets managed by advisers to private funds and the unique features of private fund investment that may lend themselves to certain recurring issues (e.g., undisclosed conflicts of interest, fees and expenses, valuation, custody and controls around material nonpublic information) have made private funds a growing focal point for the Division.31 In the last two years, the SEC has brought more cases in this area than any other class of registrant.

In FY 2022, the SEC brought actions concerning conduct by private fund advisers and associated individuals for alleged schemes to conceal the downside risks of a complex options trading strategy. These actions alleged a failure to comply with the Custody Rule or to update Forms ADV to accurately reflect the status of their private fund clients’ financial statements, and a failure to properly offset management fees charged to private equity funds and making misleading statements to investors in those funds about the fees and expenses charged.32

Complex Products

The SEC brought an action against a multinational investment bank for allegedly failing to adequately train its financial advisors and alert them of the risks associated with a particular strategy resulting in losses to clients.33 In another notable action, the Division charged the owner and other senior officers of a private investment firm, as well as the firm itself, for allegedly orchestrating a fraudulent scheme that resulted in billions of dollars in trading losses to the firm’s counterparties.34

Continued Focus on Traditional Enforcement Priorities

Although hot-button issues like ESG and crypto dominate the media, the SEC has continued to pursue actions in core focus areas like issuer disclosures, insider trading and the FCPA.

The SEC brought actions against several issuers for misleading investors in their disclosures.35 Examples include:

- a settled action against an airplane manufacturer for allegedly misleading investors about the safety of a particular plane model following crashes in 2018 and 2019;36

- a settled action against a producer of minerals for allegedly misleading investors about a technology upgrade that the company claimed would reduce costs but ultimately increased them, and for failing to properly assess whether to disclose financial risks created by their excessive discharge of mercury in Brazil;37 and

- a first-of-its-kind settled action against a multinational technology company for allegedly having inadequate disclosures concerning the impact of cryptomining on the company’s gaming business. Even though the revenue and accounting were accurate, the company did not sufficiently disclose, as part of its risks and management discussion and analysis disclosures, earnings and cash flow fluctuations related to volatile cryptomining business.38

We anticipate that the Earnings Per Share Initiative will continue to focus on earnings management practices that result in immaterial adjustments that nonetheless have qualitatively material impact on revenue or earnings guidance. In addition, the SEC continues to be focused on sales practices, including pull-in practices and order backlog management, where the revenue is correct under the Financial Accounting Standards Board’s (FASB’s) Accounting Standards Codification (ASC) 606, but disclosures surrounding financial performance — such as ability to meet revenue guidance, maintain year-over-year growth or have customer demand for a product — are inaccurate or misleading.

- A notable action in FY 2022 included a settled action against a cloud computing and virtualization technology company for allegedly not properly disclosing its order backlog management practices, which enabled the company to push revenue into future quarters by delaying product deliveries to customers and improperly disclosing the company’s slowing performance relative to its projections.39

As a recurring theme in 2022, the Division brought cases in areas that are the subject of SEC rulemakings to reinforce the need for additional, and likely more prescriptive, regulation. Chairman Gensler made his view known that 10b5-1 plans are subject to potentially abusive practices, and the SEC has proposed rulemaking to address these practices.40 At the same time, the SEC charged a public company’s executives with insider trading in connection with such executives establishing a 10b5-1 trading plan after allegedly becoming aware of material nonpublic information.41

The Division remains committed to enforcing the FCPA and brought several cases in this space, consistent with the pace from FY 2021.42

Market participants can expect to see these core areas continue to be a priority for the Division in 2023.

_______________

1 U.S. Securities and Exchange Commission Division of Enforcement, SEC Announces Enforcement Results for FY22 (the Report).

2 See id.

3 See id.

4 See Report at 1.

5 See id.

6 See id.

7 Kokesh v. SEC, 137 S. Ct. 1635 (2017); Liu v. SEC, 140 S. Ct. 1936 (2020); 15 U.S.C. § 78u(d).

8 See U.S. Securities and Exchange Commission Division of Enforcement, Addendum to Division of Enforcement Press Release Fiscal Year 2022.

9 See id. at 1.

10 See id.

11 See id.

12 See Report at 2-3.

13 See id. at 2.

14 See id.

15 See id.

16 See id.

17 See id.

18 See id.

19 See Gurbir S. Grewal, Remarks at Securities Enforcement Forum.

20 See Report at 2.

21 See id.

22 See id. at 6.

23 See id.

24 See id.

25 See id. at 5.

26 See id.

27 See id.

28 See Report at 2.

29 See id. at 5.

30 See In the Matter of John W. Pauciulo, Esq.

31 See Report at 6.

32 See id.

33 See Report at 7.

34 See id.

35 See id. at 4-5.

36 See id. at 4.

37 See id. at 4-5.

38 See id. at 5.

39 See Press Release 2022-160, SEC Charges VMware with Misleading Investors by Obscuring Financial Performance.

40 See Chair Gary Gensler, Statement on Rule 10b5-1 and Insider Trading.

41 See Report at 7.

42 See Report at 8.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.