A healthy market for M&A activity, particularly cross-border deals, and a strict regulatory environment are the big factors influencing the health and activities of life sciences companies. Skadden partners John T. Bentivoglio, Jennifer L. Bragg, Marie L. Gibson and Graham Robinson discuss the outlook for businesses in this sector.

M&A activity in the life sciences sector has surged in the past year. What has contributed to this trend, and do you see it continuing throughout 2015?

Graham:  One trend that received significant attention last year that may have helped kick off a resurgence in life sciences M&A was deals in which the tax structure produced part of the value thesis. However, this portion of the deal market diminished toward the end of 2014, in large part because of the U.S. Treasury's efforts to discourage these transactions, and I think it has been over-credited. Other factors are at play as well. For starters, we are now several years into a resurgence of the life sciences IPO market and venture capital investment in new life sciences companies. Many of these companies are maturing to the point where they are very attractive investments for larger acquirers. Second, confidence in business conditions has improved in the U.S., which drives the biopharma market in particular. And third, the increase in shareholder activism and hostile M&A activity has created transaction momentum in a number of cases. I believe these factors played a larger role in creating the overall volume of life sciences M&A transactions than tax structuring alone; the life sciences M&A boom has continued even as tax-structured deals have faded. Based on what we hear, we are very optimistic about the life sciences M&A market for 2015.

One trend that received significant attention last year that may have helped kick off a resurgence in life sciences M&A was deals in which the tax structure produced part of the value thesis. However, this portion of the deal market diminished toward the end of 2014, in large part because of the U.S. Treasury's efforts to discourage these transactions, and I think it has been over-credited. Other factors are at play as well. For starters, we are now several years into a resurgence of the life sciences IPO market and venture capital investment in new life sciences companies. Many of these companies are maturing to the point where they are very attractive investments for larger acquirers. Second, confidence in business conditions has improved in the U.S., which drives the biopharma market in particular. And third, the increase in shareholder activism and hostile M&A activity has created transaction momentum in a number of cases. I believe these factors played a larger role in creating the overall volume of life sciences M&A transactions than tax structuring alone; the life sciences M&A boom has continued even as tax-structured deals have faded. Based on what we hear, we are very optimistic about the life sciences M&A market for 2015.

Marie: I agree, 2015 should be another busy year. It's too early to tell whether inversion transactions are completely off the table; we continue to be in a "wait and see" mode until the new Congress begins work and the U.S. Treasury provides further interpretations. In addition, I believe activist scrutiny and shareholder demands for finding and developing more sources of growth will continue to lead to traditional mergers inside (and outside) the life sciences sector. There is a general perception that potential acquirers are still holding onto significant cash balances and need to deploy their capital to achieve desired growth rates.

In the life sciences sector, I also expect to continue to see many small- and medium-sized transactions — especially product acquisitions — in-licensing of products and intellectual property, and collaborations. We have seen not only some large deals involving collaborations between small-cap or private companies and big pharma, but also deals among the big pharma players. More collaborations are likely as companies continue to struggle with ever-increasing costs to bring products to market.

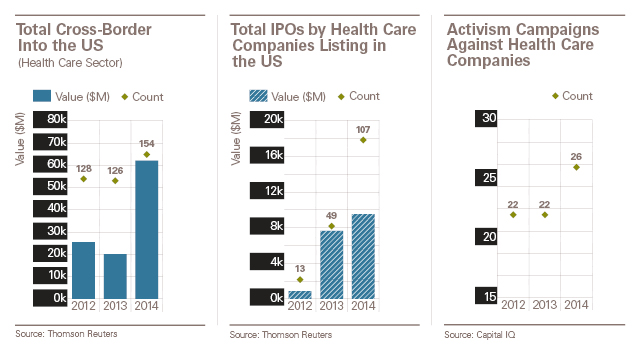

To what extent do you see cross-border transactions being an important part of the M&A market in 2015?

Marie: Our international and U.S. clients think about medicine globally and are looking for ways to expand, deepen vertical integration and enhance their supply chain capabilities — all of which indicate that the cross-border transaction market is likely to remain robust. Local pricing and reimbursement policies will continue to impact how attractive opportunities will be, but the interest is there.

Graham: I see three specific factors driving cross-border activity. First, lower tax rates outside of the U.S. in many cases result in cash-producing pharmaceuticals and medical devices being worth more if owned by a non-U.S. company. In some cases, that leads predictably to their paying a premium relative to how the U.S. market values those companies independently or the price that a U.S. acquirer would pay. Second, in the biopharma sector in particular, the large acquirers are global, but the most valuable market for new drugs is by far the U.S. As a result, many of the most attractive targets are based in the U.S. (or are foreign companies pursuing U.S. approval for their drug candidates). This leads to many non-U.S. buyers pursuing U.S. targets, a trend that should accelerate in 2015. Third, and perhaps more interestingly, we are hearing from a number of larger U.S. companies that they plan to invest significantly in ex-U.S. targets, particularly in Asia. Some of these companies have comprehensive M&A strategies mapped out, with large budgets allocated to the effort. Absent a market setback, I expect these plans will be carried out, leading in 2015 (and beyond) to a significant increase in U.S. companies buying these targets.

How will the regulatory environment play a role in these trends?

Jennifer: The global uptick in M&A that Graham and Marie describe can present regulatory challenges. Companies must evaluate the quality of the manufacturing operations in the organizations they acquire in order to ensure they meet FDA regulations. When the operations are located in geographies distant from the parent — like when a U.S. company purchases a target in Asia — this becomes more challenging. Overall, the globalization of the supply chain that has taken place over the last decade has resulted in increased efforts by the FDA to ensure that manufacturing operations outside the United States are commensurate with the standards applied to domestic operations. This appears to be part of a broader effort by the FDA to focus its enforcement resources on core public health issues, such as ensuring product quality. The FDA has a variety of regulatory enforcement tools that it can employ when it believes a company has systemic shortcomings in its manufacturing operations, and some are quite potent. This means that what may initially have seemed like a simple regulatory issue can become much more significant, sometimes having a material effect on a company's bottom line.

John: In addition to those issues, life sciences companies continue to face a challenging regulatory environment in getting their products to market — and getting reasonable reimbursement for their products once they are approved. The FDA approved 35 new molecular entities (NMEs) and biological license applications (BLAs) through December 15, 2014. That figure is up from the 27 NME and BLA approvals in 2013 but is essentially flat when compared to the 39 approvals in 2012. Also, criticism of the FDA's device approval and clearance process, including front-page investigative stories in leading national publications, poses a risk of stricter approval and clearance requirements in 2015. On the reimbursement side, the Obamacare medical device tax continues to be a focus of policy and legislative lobbying as manufacturers contend the tax is curbing profits and stifling innovation. Drug and device companies also face other pressures as public- and private-sector health care reform efforts focus on reimbursement rates tied to cost effectiveness and cost savings. This will require companies to gather data — above and beyond what's necessary to support approval or clearance — to ensure adequate coverage and reimbursement.

Kickback and off-label promotion issues are another area where drug and device companies have endured a very tough enforcement environment. Do you see enforcement continuing at its current pace in 2015? What other areas of enforcement should companies be considering?

John: The good news is that industrywide compliance efforts are having a positive impact — we didn't see a settlement above $1 billion in 2013 or 2014. Such "blockbuster" settlements will continue to be rare in the next several years — and possibly beyond. But the amount of enforcement activity reflected in the total number of investigations and settlements is likely to continue at a high tempo as qui tam relators continue to file hundreds of cases each year — many targeting life sciences companies — and the U.S. Department of Justice is obligated by law to investigate these complaints. We have seen an increased willingness of qui tam relators to pursue active litigation even when the DOJ declines to intervene, and we predict this trend will continue. We also believe the DOJ will bring criminal charges against individuals in cases where it believes the conduct has been egregious, as we've seen in the Otis Medical and Vascular Solutions cases this year.

Jennifer: I agree. Unfortunately, government enforcement efforts directed at life sciences companies are not likely to stop in the near term. There are simply too many financial incentives for relators to bring cases and for the DOJ to pursue them. Nevertheless, we have seen the nature of these cases change and expect some of these changes to continue. In addition to fewer ultra-large settlements, as John mentioned, our sense is that the DOJ has begun to focus more on the financial relationships between physicians and life sciences companies, particularly on the reimbursement process and the role that life sciences companies play in it. Additionally, look for the FDA to recommend cases to the DOJ when it believes it has uncovered serious manufacturing lapses that may impact public health.

The Second Circuit's decision in United States v. Caronia was heralded by some lawyers as a big loss for the DOJ's prosecution of truthful, off-label promotional activities. What impact, if any, has the decision had in the current cases you're handling?

Jennifer: To understand the impact of Caronia, it's important to start with some background. Historically, the DOJ and FDA have been the two important players policing life sciences companies' promotional efforts. The FDA developed policy and referred cases to the DOJ in instances where it believed its policies had been flouted in an aggravated fashion. For much of the last decade, however, a third player — relators — began to impact policy. The civil False Claims Act, with bounty provisions that provide tremendous incentives for relators to bring claims to the government rather than the life sciences company, required the DOJ to investigate these cases. Ultimately, the DOJ had to construct legal theories to support enforcement decisions in an area where neither the case law nor the regulations were well-developed.

Over time, the DOJ’s theories of wrongdoing, as articulated through settlement materials, grew further afield from the text of the statute or the regulations. The company under investigation could ill afford to risk the consequences of conviction — which can include exclusion from federal health care programs — by seeking review of the legal issues before a judge at trial. Thus, company after company reluctantly settled cases premised on legal theories that were sometimes untested and poorly supported without having a meaningful opportunity to challenge those theories. Too often, the FDA did not appear to have a meaningful voice in determining whether the legal theories were consistent with its policy.

Today, the FDA appears to have reclaimed its voice in setting policy as it pertains to how companies can lawfully promote their products. The FDA has spent considerable time and effort developing guidance documents that articulate how it views various practices and how it believes its policy can be achieved in a compliant manner. While many are unsure that FDA policy aligns with the First Amendment, these guidance documents have been a welcome development and have been extremely useful in fostering a dialog regarding promotional practices that for many years resided in the “gray area.” At the same time, the DOJ seems to be less focused on cases involving solely promotional speech. While we don't know why this shift has occurred, it is possible that the decision in Caronia played a role. The reality of Caronia, two years later, is that it has almost certainly been more impactful than the government publicly acknowledged.

John: I agree. Many DOJ prosecutors have said publicly that Caronia has had no effect on their enforcement efforts, but this is not what we're seeing in the current cases we're handling. The DOJ is now — appropriately, in our view — focused on promotional activity that involves false or misleading information and is steering away from purely truthful, nonmisleading promotional activities. We think this new, more narrow approach will continue until other federal circuits or the Supreme Court squarely address the issue.

Looking more broadly at the industry and the year ahead, all of these factors — a strong pace in M&A and corporate activity and the accompanying regulatory challenges of that activity, as well as the current enforcement environment — indicate that companies should continue to bolster their compliance programs, incorporate robust pre- and post-closing regulatory diligence in their acquisition efforts, and heed developments on the enforcement front.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.