Recent efforts by the Securities and Exchange Commission (SEC) to bring concentrated regulatory attention to investment managers sharpened over the past year to include a particular focus on the private equity and hedge fund industry and on a variety of monetary arrangements between advisers and the funds they manage. Earlier this year, the SEC’s Office of Compliance Inspections and Examinations formed a new group tasked with overseeing the private equity and hedge fund industries. That group cooperates with and complements the existing Asset Management Unit in the SEC’s Division of Enforcement. Last year, those efforts resulted in public SEC pronouncements, including through enforcement actions, regarding fees and expenses charged by private funds and private fund advisers. Moreover, managers and investors have responded to the issues identified by regulators in ways that are altering past fee and expense practices.

The SEC identified several practices that it asserts were implemented without adequate disclosure and investor consent and therefore resulted in deficiencies during exams, including:

- Moving expenses from the management company into funds through (1) the use of related-party service providers who appear to be part of the manager's team (e.g., operating partners, senior advisers or consulting firms); (2) automated standard processes with costs paid by the funds; and (3) outsourcing traditional back-office functions (such as legal, accounting and risk) to related parties;

- Generating additional revenues that reduce cash available to funds through (1) monitoring fees that accelerate and have evergreen provisions; and (2) use of related-party service providers that kick back cash to the manager and may provide services of questionable value (e.g., captive consulting firms and group purchasing programs);

- Charging undisclosed "administrative" or other fees not contemplated by the partnership agreement; and

- Exceeding the limits in the partnership agreement regarding transaction fees or charging transaction fees in cases not contemplated by the partnership agreement, such as for reorganizations.

Implications for 2015

In this new environment, general disclosure of fee and expense arrangements may be subject to challenge, particularly in situations where provisions appear ambiguous when judged in hindsight as failing to have adequately alerted investors to particular charges. Given the heightened investor scrutiny and the fiduciary issues raised by such scrutiny, advisers should ensure that (1) their initial and ongoing fee and expense disclosure is clear and complete; (2) their fee and expense practices are consistent with prior disclosure or they obtain investor consent; and (3) the substance of their practices is justifiable.

__________________

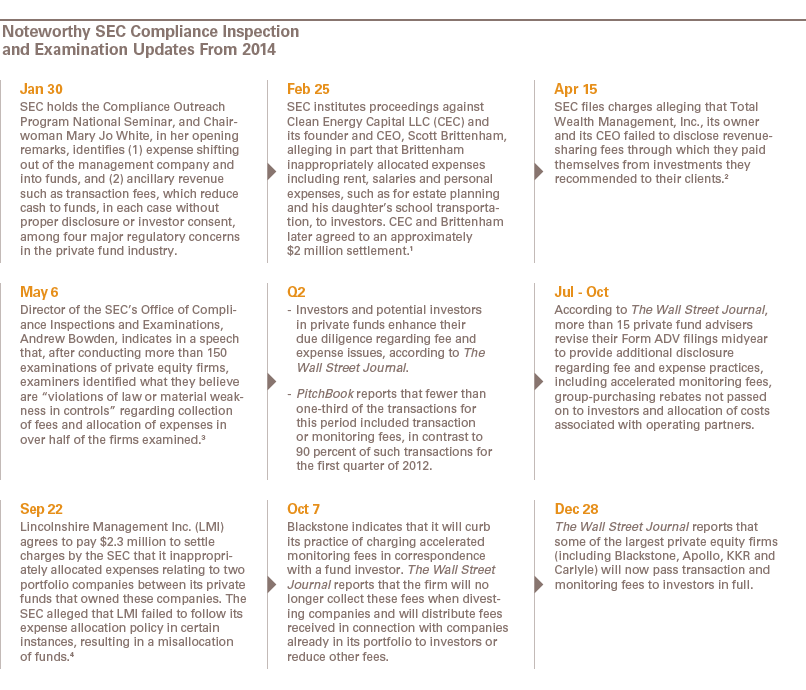

1 Clean Energy Capital, LLC, Securities Act Release No. 9667, Exchange Act Release No. 73,386, Investment Advisers Act Release No. 3955, Admin. Proc. No. 3-15776 (Oct. 17, 2014).

2 Total Wealth Management, Inc., Securities Act Release 9575, Exchange Act Release No. 71,948, Investment Advisers Act Release No. 3818, Investment Company Act Release No. 31,107, Admin. Proc. No. 3-15842 (April 15, 2014).

3 Speech, Andrew J. Bowden, Director, Office of Compliance Inspections and Examinations, at the Private Equity International Private Fund Compliance Forum (May 6, 2014), available at www.sec.gov/News/Speech/Detail/Speech/1370541735361.

4 Lincolnshire Management, Inc., Investment Advisers Act Release No. 3927, Admin Proc. No. 3-16139 (Sept. 22, 2014).

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.