In our August 2015 client alert, we reported on the European Union's tentative efforts to extend the Alternative Investment Fund Managers Directive (AIFMD) marketing passport to managers and funds established in non-EU jurisdictions. Almost a year later, on July 19, 2016, the European Securities and Markets Authority (ESMA) published its long-awaited advice to the European Commission (the Commission) on that extension, which can be found here.

Of the 12 jurisdictions assessed for equivalence, ESMA issued positive advice with respect to five jurisdictions: Canada, Guernsey, Japan, Jersey and Switzerland. Four other jurisdictions (U.S., Australia, Hong Kong and Singapore) received qualified assessments, which may result in conditions being placed by the Commission on managers and funds established in these jurisdictions before the marketing passport is extended to them. ESMA, however, declined to provide definitive advice in relation to the Cayman Islands, Bermuda and Isle of Man due to either impending regulatory changes in these jurisdictions or lack of AIFMD-like regimes.

ESMA's latest advice is a welcome step toward the extension of the marketing passport to third countries and would at first glance suggest that the EU proposes to shed its "Fortress Europe" reputation in the alternative investment funds space. In particular, the third-country passporting regime is expected to benefit non-EU alternative investment fund managers (AIFMs) seeking to market non-EU alternative investment funds (AIFs) in jurisdictions such as Italy, Spain and France that are practically "closed" to marketing under national private placement regimes (NPPR). Nonetheless, it is unclear at this stage whether the Commission will delay the entry into force of the third-country passporting regime until more jurisdictions have received positive ESMA assessments. Notably, certain traditional fund domiciles such as the Cayman Islands and Bermuda are currently in the process of implementing new AIFMD-compliant regulatory regimes, and ESMA has therefore chosen not to given any definitive advice with respect to these jurisdictions at this stage. Market distortions in terms of investor choice could arise if the marketing passport is extended to a select group of "equivalent" third countries ahead of other jurisdictions, and if jurisdictions such as the U.S. are excluded or restricted, these jurisdictions could impose retaliatory measures.

Assuming the Commission decides to extend the marketing passport to the third countries assessed as equivalent in this round of assessment, it would need to adopt a delegated act within three months specifying the date that the marketing passport would be extended to those jurisdictions. Given the concerns of market distortion mentioned above, ESMA has expressly advised that the delegated act be deferred until a sufficient number of third countries are assessed as equivalent. Furthermore, if the European Council or Parliament objects to the terms of the delegated act, the extension of the third-country passporting regime could be further delayed.

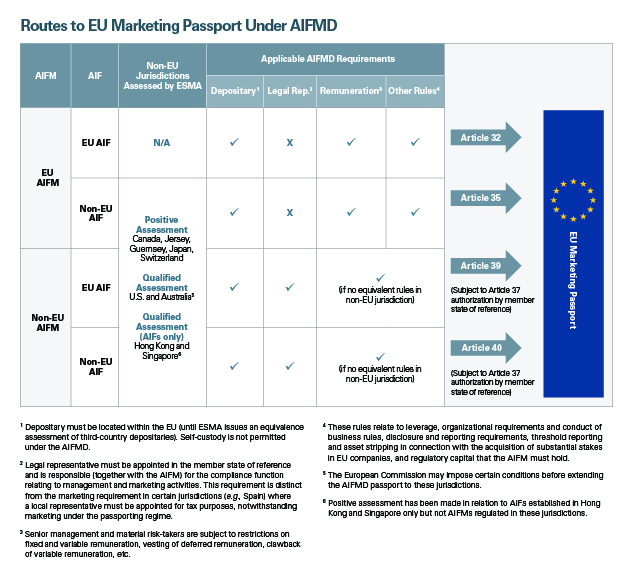

The different routes and applicable rules under the AIFMD that would apply to AIFMs and AIFs once the marketing passport is extended to third countries are summarized in the accompanying chart.

Commentary

Impact on US AIFMs

ESMA's advice concluded that there were a number of differences between the U.S. regulatory framework and the AIFMD with respect to investor protection. Notably, a U.S. fund may act as its own custodian in certain circumstances under applicable U.S. rules, which the AIFMD effectively prohibits because a separate depositary must be appointed. In addition, while the Investment Advisers Act of 1940 includes certain rules on registered fund performance fees, AIFMD-like rules on remuneration do not generally exist in the U.S. yet (although there are currently U.S. regulatory proposals to require bonus deferrals and clawbacks for significant risk-takers).

In the context of funds marketed by managers to professional investors that involve a public offering, ESMA's view was that extending the marketing passport to U.S. fund managers may lead to an unlevel playing field, as EU managers seeking entry to the U.S. market are subject to stringent U.S. registration requirements (and the attendant costs of seeking registration).

Consequently, ESMA has suggested the following options for extending the marketing passport to the U.S.:

- granting the passport to U.S. funds dedicated to professional investors and marketed in the EU without any public offering;

- granting the passport to U.S. funds that are not mutual funds under the Investment Company Act of 1940; and

- granting the passport to U.S. funds that are marketed to professional investors only.

To the extent the Commission agrees with these options, most U.S. private investment funds that are intended to be offered in the EU are likely to be able to comply with the relevant conditions because such funds tend to be offered to EU professional investors through private placement. However, U.S. AIFMs wishing to market under the passporting regime will still need to seek authorization from an EU member state of reference under Article 37 of the AIFMD. Crucially, authorization is contingent on the U.S. AIFM's compliance with most of the AIFMD's regulatory requirements, including the appointment of an EU-based depositary, implementation of the relevant remuneration rules (subject to proportionality) and any other regulatory rules under the AIFMD (e.g., leverage limits, threshold reporting and asset stripping in connection with EU companies) if there are no equivalent rules in the U.S. that have the "same regulatory purpose and offer the same level of protection to investors." Furthermore, a legal representative also must be appointed in the member state of reference, and that representative will be responsible (together with the AIFM) for the compliance function relating to the AIFM's management and marketing activities.

U.S. AIFMs who do not wish to assume the marketing passport's additional regulatory burden and costs may continue to market in the EU under the NPPR for at least the three-year transition period during which the NPPR will operate alongside the third-country passporting regime, to the extent the NPPR is not withdrawn under local law. Notably, we understand the current position under German law is that the NPPR will terminate automatically in Germany once the third-country passporting regime comes into effect.1

In the near term, the NPPR will continue to be attractive for certain U.S. AIFMs, especially if the marketing effort is targeted at jurisdictions such as the U.K. and Luxembourg where the NPPR requirements are relatively light, as opposed to at other jurisdictions such as Denmark, where a “depositary-lite” must be appointed.

Brexit and Impact on UK AIFMs

Should the U.K. leave the EU and a negotiated deal for passporting is not available to U.K. AIFMs, the extension of the marketing passport to U.K. AIFMs should in theory be straightforward, as the U.K. has already implemented the AIFMD. However, extension of the marketing passport to the U.K. depends on the adoption of a delegated act by the Commission (which must not be vetoed by the European Council and Parliament), and any such step will ultimately be driven by political considerations that are intertwined with the broader Brexit negotiations. This also assumes the U.K. does not water down the regulations applicable to U.K. fund managers.

Even if the U.K. is granted full equivalence, U.K. AIFMs seeking to market under the passporting regime will still be subject to an additional layer of compliance costs, because in addition to the delay associated with any authorization process in the member state of reference, an EU-based depositary and legal representative will need to be appointed. U.K. AIFMs should therefore consider the viability of alternative solutions currently adopted by non-EU AIFMs, including establishing an EU AIFM subsidiary or adopting a "hosted-platform" solution provided by third-party EU AIFMs, to ensure their continued access to the marketing passport should that passport be commercially necessary.

Continued Availability of NPPR

The extension of the marketing passport to third countries triggers a three-year transition period during which the NPPR will continue to be available alongside the passporting regime (unless it is withdrawn under local law, such as in Germany). Thereafter, Article 68 of the AIFMD requires ESMA to advise on whether to terminate the NPPR regime. Assuming ESMA issues positive advice in this respect and the Commission adopts a delegated act within three months of specifying the date that the NPPR will cease to be available, the passporting regime will become the "sole and mandatory" regime applicable in all member states.

With respect to any jurisdiction that has not been assessed as equivalent by the time the NPPR regime terminates, AIFs and AIFMs established in such jurisdictions are effectively closed off from EU investors until they receive the marketing passporting (or rely on a valid claim of reverse solicitation). This risks a step backward in terms of investor choice compared to the NPPR regime and would further cement the EU's "Fortress Europe" reputation.

Application to Subthreshold Non-EU AIFMs

Article 37 of the AIFMD requires non-EU AIFMs seeking the marketing passport to seek authorization from its member state of reference; however, no provision has been made for subthreshold non-EU AIFMs.

Smaller non-EU AIFMs would welcome clarity on whether subthreshold non-EU AIFMs are able to register with a member state of reference or are required to undergo the full authorization process under Article 37.

_____________

1 Once the NPPR is terminated, marketing in Germany by AIFMs of AIFs established in equivalent jurisdictions will only be possible with the marketing passport. However, transitional relief is available to AIFMs from equivalent jurisdictions who have received marketing approval for their AIFs under the German NPPR prior to its termination. Such AIFMs may continue to market in Germany without applying for the third-country passport, provided they do not market the AIF in another EU member state. We understand the German Federal Financial Supervisory Authority (BaFIN) has indicated informally that the NPPR will continue to be available to jurisdictions that have not received their equivalence assessment yet, although no official written announcement has been published by BaFin to confirm this point.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.