Certain questions seem to recur when it comes to outside counsel’s communications with a company’s auditors about potential exposures as a result of litigation or regulatory/enforcement matters and the underlying accounting for such matters. First, how can clients satisfy auditors’ requests for information without waiving the attorney-client and work-product privileges? Second, how do the standards for accounting for loss contingencies apply in circumstances where a company expects insurance to cover any ultimate losses?

Waiving Privilege in Response to Auditor Requests

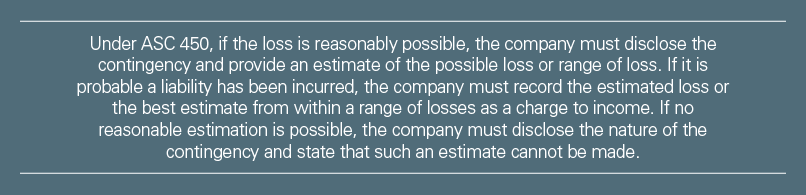

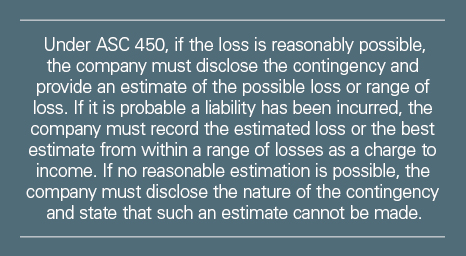

Under the Financial Accounting Standards Board’s Accounting Standards Codification Topic 450 (ASC 450), titled “Contingencies” (formerly Financial Accounting Standards No. 5, “Accounting for Contingencies”), the preparation of financial statements under principles of accrual accounting requires companies to make many judgments about contingent liabilities, including ones arising from pending or anticipated litigation, regulatory or law enforcement proceedings or investigations and in some circumstances, internal investigations. Under ASC 450-20, a contingent loss must be categorized as remote, reasonably possible or probable. Depending on the categorization, the company may have to disclose the nature of the contingency and estimated loss, or record the estimated loss or the best estimate from within a range of losses as a charge to income.

{kind=link}

In the normal course of an external audit, independent auditors routinely request information to support a company’s decision about how to account for these litigation and regulatory-related contingencies. The basic facts, claims and allegations related to a particular contingency generally are not privileged. However, auditors regularly request additional information to evaluate the reasonableness of a company’s judgment on how to apply the contingency standards to a particular or potential claim or exposure. For example, it is common for auditors to ask the company’s in-house and outside counsel for information and perspective on the likelihood (or lack thereof) of any ultimate loss — a request that triggers considerations about whether the information being sought is protected, in whole or in part, by the attorney-client or work-product privileges and, in turn, about the risks of waiving such privileges.

The attorney-client privilege protects the substance of legal advice, including an outside counsel’s assessment of likely exposure. The general rule is that providing a third party with information otherwise protected by the attorney-client privilege waives the privilege and allows third parties, including adverse litigants, to discover that information (assuming the absence of another applicable privilege). Courts generally have held that there is no exception to this principle for companies that choose to share otherwise privileged information with their independent auditors.

To the extent that information shared with a third party is protected by the work-product doctrine, such protection is waived only if the third party is itself adverse to the company or if the disclosure to the third party results in a substantial likelihood that the material will be disclosed to adverse litigants. Applying various formulations of that standard, courts generally have held that the work-product protection is not waived when outside counsel, acting at their client’s direction, share information with auditors. With respect to adversity, as the U.S. District Court for the District of Columbia stated in 2010, “an independent auditor [] cannot be the company’s adversary” in the sense contemplated by the work-product doctrine because “even the threat of litigation between an independent auditor and its client can compromise the auditor’s independence and necessitate withdrawal.” As to creating a substantial likelihood that the otherwise protected information would be disclosed to adverse litigants, that court recognized companies’ reasonable expectation of confidentiality for information conveyed to auditors because independent auditors’ professional obligations require them to maintain the confidentiality of client information.

However, the work-product doctrine should not be viewed as an absolute backstop to disclosure of attorney-client privileged information. In addition to the fact that it can be overcome or waived under certain circumstances, the doctrine applies only to analyses prepared in anticipation of litigation. For example, if an auditor asks for support for a company’s judgment not to record a litigation reserve for a potential breach of contract claim, the company should be cautious of providing (in form or substance) an attorney’s analysis if it was prepared before any reasonable expectation of litigation. This includes, for instance, a memo from outside counsel addressing potential legal risks prepared at the time the contract was originally negotiated. If the legal analysis was not prepared in anticipation of litigation, it might not be covered by the work-product doctrine and thus might be discoverable.

Companies would be well served to carefully evaluate how best to respond to auditors’ requests for information from in-house or outside counsel to minimize the potential for exposing privileged communications and analyses to discovery. Companies should consider the circumstances in which information or documents were generated so they understand the applicability of the attorney-client and work-product privileges, and thus the consequences of disclosure. Where alternatives exist, companies can strive to provide information that carries the least severe waiver consequences. For example, providing an analysis protected by both the attorney-client and work-product privileges would be preferable to providing one protected by only the attorney-client privilege. Finally, a company’s representatives should clearly convey to auditors their expectation of confidentiality with respect to the information being provided.

Accounting for Litigation Exposure Covered by Insurance

Companies also frequently encounter the question of how the potential for insurance coverage impacts the accounting for a particular loss contingency. More specifically, companies often encounter circumstances in which a material loss is probable and estimable, but where management expects insurance to cover all or part of the estimated loss.

For example, assume that a fire at a company’s main manufacturing plant leads to the destruction of surrounding businesses and the company anticipates that the ultimate exposure for impacted businesses’ damage and lost income claims will be material to the company but also recovered through insurance. The company in this hypothetical scenario might prefer not to record a material charge when it reasonably expects that there will be no net financial impact from losses from the anticipated litigation. However, the staff of the Securities and Exchange Commission (SEC) has advised that companies should not ordinarily consider the presence of an insurance recovery when accounting for loss contingencies. Instead of offsetting or netting the amount of the expected insurance coverage against the estimated loss, companies should record the full estimated loss independent of any loss recovery from possible insurance recovery.

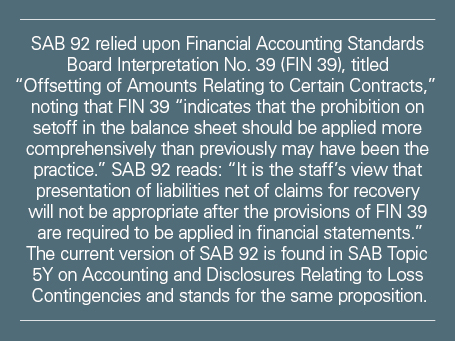

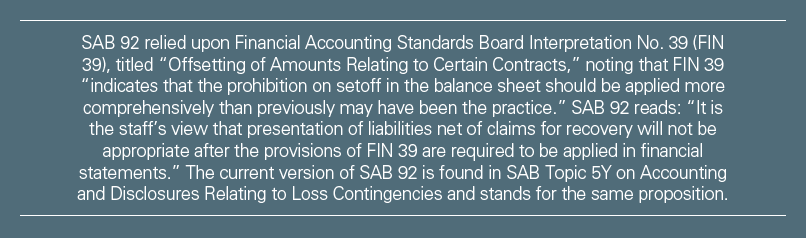

Perhaps the most direct accounting guidance on the issue comes originally from SEC Staff Accounting Bulletin 92 (SAB 92) regarding accounting and disclosures for loss contingencies. Issued in June 1993, and itself the source of controversy at the time, SAB 92 generally prohibits the formerly widespread practice of offsetting insurance coverage before disclosing or accruing a loss contingency. As the SEC staff explained in the original SAB 92, the “separate presentation of the gross liability and related claim for recovery in the balance sheet most fairly presents the potential consequences of the contingent claim on the company’s resources and is the preferable method of display.” The risks surrounding an entity’s contingent liability should be treated as “separate and distinct from those associated with its claim for recovery against third parties,” the staff explained in its original release, as did one of the then-commissioners of the SEC. This is to avoid leaving “investors unaware of the full magnitude of the liability” or even “lull[ing] them into a less rigorous consideration” of the relevant factors defining the full essence of liabilities.

{kind=link}

In accounting for a loss recovery, GAAP (generally accepted accounting principles) permits companies to record an asset only upon a determination that the recovery is probable. Insurance coverage can be uncertain and disputed, and it is often not clear until later stages of a litigation how much of a claim or settlement an insurance carrier will cover under a particular policy. Indeed, despite the insurer acknowledging some coverage, often the insured and insurer engage in extensive negotiations during litigation to determine their relative contributions to any settlement. As a practical matter, this means that it may be difficult to reach a conclusion at the time a litigation reserve is recorded that an insurance recovery is equally probable — thereby creating the prospect of reporting a liability and a loss recovery in different periods.

This perceived mismatch in the timing of when an estimated loss and insurance coverage should be recorded may be an unsatisfying outcome for companies that want to avoid a perception among investors that the company may suffer material, uncovered litigation losses. To help investors understand that insurance coverage for litigation exists and the extent to which it may offset the estimated loss, companies generally can make appropriate disclosures in their financial statements or other public disclosures about their general insurance coverage or coverage specific to a particular claim. The consideration is double-edged, however, as companies often are understandably hesitant to disclose information about the scope of their insurance coverage for fear it will make them a litigation target or paint a picture of a deep, available pocket. Striking the right balance in particular facts and circumstances will continue to present challenges.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.