The Securities and Exchange Commission (SEC) recently adopted amendments to disclosure requirements applicable to various registration statements and periodic reports, including minor changes to applicable form cover pages (which will impact upcoming quarterly reports on Form 10-Q for calendar year companies), as summarized below.

Updated Definition of Smaller Reporting Company

Effective September 10, 2018, the SEC’s definition of “smaller reporting company” (SRC) has been revised so that companies qualify as an SRC if they have less than $250 million of public float or less than $100 million in annual revenues for the previous year and no public float. This increase in the threshold, which may be relied on in connection with the filing of Forms 10-Q for the quarter ending September 30, 2018, substantially expands the number of companies that qualify for the reduced disclosure requirements permitted to SRCs.1 Companies should consider whether they may qualify as an SRC and, if so, if they intend to rely on the relief in connection with the next applicable SEC filing.

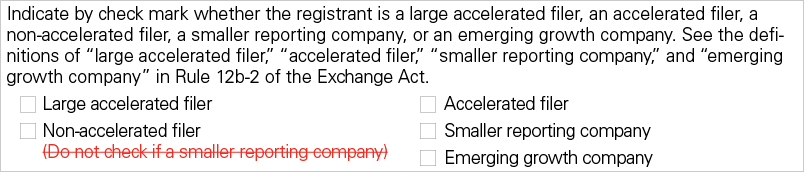

Regardless of filer status, the amended definition also produces changes in cover pages to various registration statements and periodic reports. Importantly, a registrant may now indicate that it qualifies as both an SRC and a non-accelerated filer. Accordingly, the related parenthetical to the non-accelerated filer status check box was deleted in the form cover pages of registration statements (Forms S-1, S-3, S-4, S-8, S-11 and 10) and periodic reports (Forms 10-K and 10-Q), as shown below:

New Inline XBRL Requirements

In connection with the SEC’s adoption of new rules requiring inline eXtensible Business Reporting Language (XBRL) tagging of financial information in SEC filings (which are subject to transition periods starting in 2019), companies are no longer required to post Interactive Data Files on their websites, effective September 17, 2018.2 Accordingly, references to “posting” Interactive Data Files have been removed from cover pages of periodic reports (Forms 10-K, 10-Q, 20-F and 40-F), as shown below:

No Impact Yet for Recent Amendments to Streamline Certain Disclosure Requirements

On August 17, 2018, the SEC adopted a number of amendments to certain disclosure requirements that have become duplicative or outdated. These amendments are largely technical and will become effective 30 days after publication in the Federal Register, which has yet to occur. Although the timing of the amendments’ applicability remains uncertain, such amendments are not expected to impact disclosures in upcoming quarterly reports on Form 10-Q for calendar year companies. In addition, the SEC staff will likely issue guidance on how to implement the new requirements. Nonetheless, companies should consider the potential impact of these amendments on future SEC filings. A marked version showing amendments to the disclosure rules is available here.

__________________

1 For additional information, see our July 9, 2018, client alert, “SEC Expands ‘Smaller Reporting Company’ Definition,” and the SEC’s adopting release.

2 For additional information, see the SEC’s adopting release.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.