On October 10, 2018, the Department of the Treasury, as the chair of the Committee on Foreign Investment in the United States (CFIUS), issued two sets of interim regulations implementing certain provisions of the Foreign Investment Risk Review Modernization Act of 2018 (FIRRMA), the CFIUS reform legislation enacted in August 2018.1 The first set of regulations is largely administrative, implementing certain FIRRMA provisions that took immediate effect but were in some cases inconsistent with existing CFIUS regulations.2 The second set of regulations details a FIRRMA-authorized pilot program expanding CFIUS jurisdiction over noncontrolling foreign investments in critical technology companies and requiring mandatory declarations advising CFIUS of foreign investments in such companies.3

Assuming no changes following a 30-day public comment period, the interim rules will formally take effect on November 10, 2018, and are expected to remain in effect until final CFIUS regulations implementing all of FIRRMA are issued on or before February 13, 2020. As discussed below, however, certain provisions of the pilot program will apply to transactions taking place as soon as October 11, 2018.

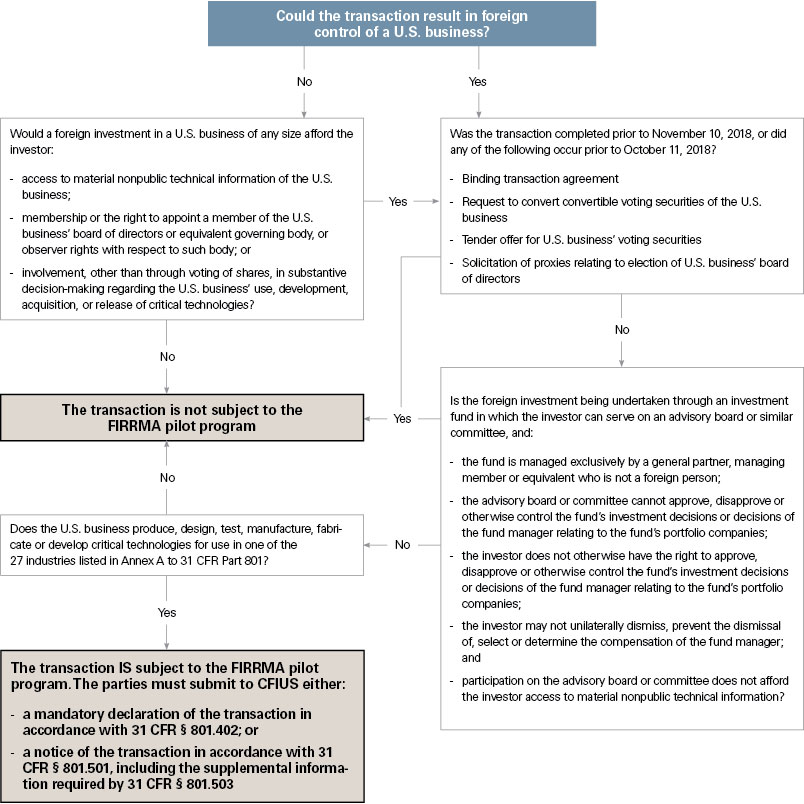

Jurisdiction Over Noncontrolling Foreign Investments in Critical Technology Companies

Historically, CFIUS jurisdiction has been limited to transactions that could result in foreign control of a U.S. business. FIRRMA expands CFIUS’ jurisdiction to certain foreign investments regardless of whether the investment provides the investor with control, and the interim regulations establish a pilot program for implementing FIRRMA’s mandate. The pilot program applies to transactions meeting the following criteria:

- Target Industries. The pilot program focuses on 27 designated “Pilot Program Industries,” listed in the table below. These industries closely align with those subject to heightened CFIUS scrutiny in recent years.

- Target Business. The U.S. business must be a “Pilot Program U.S. Business,” meaning it produces, designs, tests, manufactures, fabricates or develops a critical technology that is (i) used in connection with the company’s activity in one or more of the Pilot Program Industries or (ii) designed by the U.S. business specifically for use in one or more Pilot Program Industries.

- “Critical technologies” generally include (i) military technologies subject to the International Traffic in Arms Regulations; (ii) civilian/military dual-use technologies subject to Export Administration Regulations export controls (a) under multilateral regimes relating to national security, chemical and biological weapons proliferation, nuclear nonproliferation or missile technology or (b) for reasons relating to regional stability or surreptitious listening; (iii) nuclear technologies covered by rules relating to foreign atomic energy activities and export and import of nuclear equipment and materials; (iv) select agents and toxins; and (v) emerging and foundational technologies controlled pursuant to FIRRMA’s sister legislation, the Export Control Reform Act of 2018.4

- Notably, the definition of Pilot Program U.S. Business only includes companies involved in various stages of development of relevant critical technologies. It does not extend to companies in Pilot Program Industries that merely use those critical technologies.

- Access of Noncontrolling Investors. A noncontrolling foreign investment in a Pilot Program U.S. Business is subject to the pilot program if it would afford the foreign investor (i) access to material nonpublic technical information held by the Pilot Program U.S. Business; (ii) membership or observer rights on the board of directors or similar governing body of the Pilot Program U.S. Business; or (iii) the right to appoint a member of the Pilot Program U.S. Business’ board of directors; or (iv) any involvement, beyond the mere voting of shares, in substantive decision-making regarding the Pilot Program U.S. Business’ use, development, acquisition or release of critical technology. These provisions highlight the care with which foreign investors should focus on their information and decision rights in transaction agreements.

- Timing. Transactions that could result in foreign control of a Pilot Program U.S. Business, if completed after November 10, 2018, fall within the scope of the pilot program. In addition, the pilot program applies to the following noncontrolling transactions taking place on October 11, 2018, or later:

- Entry into a binding agreement establishing the terms of a foreign investment, of any amount, in an unaffiliated Pilot Program U.S. Business;

- Public offer by a foreign party to buy shares of a Pilot Program U.S. Business;

- Solicitation of proxies by a foreign party in connection with the election of the board of directors of a Pilot Program U.S. Business; or

- Foreign request for conversion of convertible voting securities in a Pilot Program U.S. Business.

Notably, the interim rules explicitly list joint ventures as transactions that could result in foreign control of a Pilot Program U.S. Business. Practically speaking, however, if the U.S. party is contributing a U.S. business, joint ventures are already viewed as control transactions under the existing CFIUS regulations.

Passive Investments Through Investment Funds Generally Exempted From Pilot Program

Although FIRRMA expands CFIUS’ jurisdiction, it also provides an exemption from jurisdiction for certain foreign investments in U.S.-managed investment funds, including those with advisory boards or similar investor committees. This exemption extends to the pilot program under the interim regulations. As a result, a foreign party may invest indirectly in a Pilot Program U.S. Business via a U.S.-managed investment fund and participate as a member of the fund’s advisory board, provided that (i) neither the foreign investor nor the advisory board is able to approve, disapprove or otherwise control the fund’s investment decisions or decisions of the fund manager relating to the fund’s portfolio companies; (ii) the foreign investor may not unilaterally dismiss, prevent the dismissal of, select or determine the compensation of the fund manager; and (iii) participation on the advisory board or committee does not afford the foreign investor access to material nonpublic technical information of the Pilot Program U.S. Business.

The flow chart below addresses the applicability of the pilot program to prospective transactions.

CFIUS Requires Mandatory Declarations for Transactions Within the Scope of the Pilot Program

It will be mandatory for parties to file a declaration advising CFIUS of transactions that meet the terms of the pilot program. Notably, as authorized by FIRRMA, CFIUS did not limit the scope of this requirement to transactions involving foreign government-controlled parties. This may reflect the inherent difficulty of requiring parties to determine for themselves whether a foreign investor would qualify as a foreign government-controlled investor for CFIUS purposes.

Parties to an implicated transaction must file a declaration at least 45 days prior to completing the transaction, or — for transactions that will be completed between the interim regulations’ effective dates of November 10, 2018, and December 25, 2018 — on or promptly after the effective date. Any party failing to comply with this requirement to submit a mandatory declaration may be liable for a civil penalty in an amount not to exceed the value of the transaction.

After parties file a declaration, CFIUS will have 30 days to respond by either clearing the transaction, requesting or suggesting the parties file a full notice, or initiating a unilateral review of the transaction if the parties are uncooperative. If CFIUS clears a transaction based on a declaration, the clearance is expected to provide the same “safe haven” from subsequent, future CFIUS review that currently applies to formal notices, except for incremental investments resulting in the receipt of additional rights, discussed further below.

The parties may elect to file a full, formal CFIUS notice in lieu of a declaration, including additional pieces of information noted in the pilot program rules. In some cases, especially when a complex or higher-risk transaction is unlikely to receive CFIUS clearance in the 30-day period allotted for declarations, it may be advisable for parties to submit a full notice.

Note that FIRRMA’s provision allowing the filing of voluntary declarations is not covered by the interim regulations and is not yet in effect.

Format for Mandatory Declarations

The interim regulations list the following requirements for mandatory declarations:

- Information identifying the parties to a transaction, the subject of the transaction and a brief description of the nature and structure of the transaction, including what will be acquired;

- Additional information clarifying the ownership of the foreign investor and its activities;

- A statement explaining how the Pilot Program U.S. Business is subject to the pilot program;

- Information about the Pilot Program U.S. Business’ previous U.S. government contracts, grants and funding;

- A description of the parties’ prior history with CFIUS; and

- A statement as to whether the parties stipulate that the transaction is covered by CFIUS’ jurisdiction, including through the pilot program.

Jurisdiction Over Incremental Changes in Control and Other Clarifying Rules

In a separate interim rulemaking, CFIUS has clarified certain FIRRMA provisions that had been in effect since August 2018 but in some cases were inconsistent with existing CFIUS rules. These interim rules take effect on October 11, 2018, and apply to any covered transaction for which a CFIUS review is initiated on or after that date.

Key provisions in the interim regulations include:

- Contingent Equity. Addressing FIRRMA’s introduction of “contingent equity” as a form of investment, the interim rules include in the definition of “transaction” both the acquisition and conversion of convertible voting instruments of an entity. CFIUS will still consider on a case-by-case basis whether the acquisition of convertible securities is a qualifying transaction for purposes of CFIUS jurisdiction, but based on the treatment of convertible securities in the context of the pilot program regulations, it appears likely that the issuance of convertible securities will be more likely to trigger CFIUS jurisdiction.

- Incremental Changes in Rights. FIRRMA provided CFIUS with expanded jurisdiction over transactions involving incremental changes in rights that result in foreign control of a U.S. business. For example, a foreign person who now owns 10 percent of the equity in a U.S. business and who, through a new arrangement, would acquire no additional ownership interest but would gain the governance rights to appoint the CEO and chief technical officer of the U.S. business, would be entering into a covered transaction. In light of this clarification, foreign investors should closely consider the outcome of increasing investment levels, renegotiating governance terms and exercising contingent interests in any U.S. business in which they hold an existing interest.

- Stipulations as to CFIUS Jurisdiction and Foreign Government Control. The interim regulations permit parties to stipulate in a CFIUS notice that a transaction is subject to CFIUS jurisdiction and that the foreign party is a foreign government-controlled entity. FIRRMA contemplates such stipulations as a condition for limiting to 10 business days the amount of time CFIUS could take to comment on draft notices and accept formal notices, but the interim regulations do not include such time limits. In all likelihood, this reflects the fact that CFIUS has not yet been able to expand its resources sufficiently to meet these timelines or the other expanded obligations of FIRRMA.

The updates and clarifications in these interim rules also include, among other changes, the lengthening of the review period from 30 to 45 days, clarification of the process to request a 15-day extension to the investigation phase for extraordinary circumstances, and removal of the requirement to file hard copies of CFIUS notices. Notably, the interim rules also expand CFIUS’ enforcement authority for noncompliance with prior mitigation agreements and for material misstatements in or omissions from CFIUS notices.

____________

Listing of Critical Technology Industries for FIRRMA Pilot Program

Aircraft Manufacturing

NAICS Code: 336411

Aircraft Engine and Engine Parts Manufacturing

NAICS Code: 336412

Alumina Refining and Primary Aluminum Production

NAICS Code: 331313

Ball and Roller Bearing Manufacturing

NAICS Code: 332991

Computer Storage Device Manufacturing

NAICS Code: 334112

Electronic Computer Manufacturing

NAICS Code: 334111

Guided Missile and Space Vehicle Manufacturing

NAICS Code: 336414

Guided Missile and Space Vehicle Propulsion Unit and Propulsion Unit Parts

Manufacturing

NAICS Code: 336415

Military Armored Vehicle, Tank, and Tank Component Manufacturing

NAICS Code: 336992

Nuclear Electric Power Generation

NAICS Code: 221113

Optical Instrument and Lens Manufacturing

NAICS Code: 333314

Other Basic Inorganic Chemical Manufacturing

NAICS Code: 325180

Other Guided Missile and Space Vehicle Parts and Auxiliary Equipment Manufacturing

NAICS Code: 336419

Petrochemical Manufacturing

NAICS Code: 325110

Powder Metallurgy Part Manufacturing

NAICS Code: 332117

Power, Distribution, and Specialty Transformer Manufacturing

NAICS Code: 335311

Primary Battery Manufacturing

NAICS Code: 335912

Radio and Television Broadcasting and Wireless Communications Equipment

Manufacturing

NAICS Code: 334220

Research and Development in Nanotechnology

NAICS Code: 541713

Research and Development in Biotechnology (except Nanobiotechnology)

NAICS Code: 541714

Secondary Smelting and Alloying of Aluminum

NAICS Code: 331314

Search, Detection, Navigation, Guidance, Aeronautical, and Nautical System and

Instrument Manufacturing

NAICS Code: 334511

Semiconductor and Related Device Manufacturing

NAICS Code: 334413

Semiconductor Machinery Manufacturing

NAICS Code: 333242

Storage Battery Manufacturing

NAICS Code: 335911

Telephone Apparatus Manufacturing

NAICS Code: 334210

Turbine and Turbine Generator Set Units Manufacturing

NAICS Code: 333611

Source: Excerpted from the Determination and Temporary Provisions Pertaining to a Pilot Program to Review Certain Transactions Involving Foreign Persons and Critical Technologies, to be published in the Federal Register on October 11, 2018.

____________

1 See our August 6, 2018, alert, “US Finalizes CFIUS Reform: What It Means for Dealmakers and Foreign Investment,” for an overview of the key provisions of FIRRMA.

2 The set of interim regulations is available here.

3 The pilot program regulations are available here. Note that although this program targets the development of critical technologies for certain specified industries, FIRRMA also contemplates the expansion of CFIUS jurisdiction over transactions involving critical infrastructure and sensitive personal data of U.S. citizens as well as mandatory declarations for certain critical infrastructure transactions.

4 See our September 11, 2018, alert, “Tightened Restrictions on Technology Transfer Under the Export Control Reform Act,” for an overview of the Export Control Reform Act.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.