On March 21, 2022, the Securities and Exchange Commission (SEC) voted 3-1 to propose long-anticipated rules mandating climate-related disclosures in companies’ annual reports and registration statements. The proposed rules would add extensive and prescriptive disclosure items requiring companies, including foreign private issuers, to disclose climate-related risks and greenhouse gas (GHG) emissions. In addition, the proposed rules would require the inclusion of certain climate-related financial metrics in a note to companies’ audited financial statements.

Key takeaways and proposed disclosure requirements are described below.

Key Takeaways

Extensive and prescriptive disclosure requirements. The proposed rules would require companies to provide climate-related information in a separately captioned section of annual reports and registration statements based on a detailed list of specific disclosure items. Proposed disclosure items include, among other things, climate-related risk oversight and governance, climate-related risks and their impacts on business strategy and outlook, Scopes 1 and 2 GHG emissions1 and, for certain companies, Scope 3 GHG emissions (i.e., indirect emissions from upstream and downstream activities in a company’s value chain). The proposal also would require a new note to companies’ audited financial statements addressing climate-related impacts on financial statement line items. In addition, large accelerated and accelerated filers would be required to obtain independent third-party assurance of their GHG emissions.

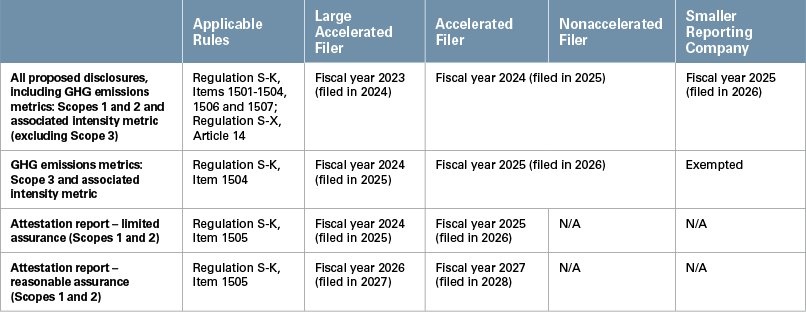

Phase-in periods. The proposed rules contemplate phase-in periods based on SEC filer status, with extended phase-in periods for Scope 3 disclosures and third-party attestation requirements. For example, if the final rules are effective by December 2022, large accelerated filers would begin providing the new disclosures in 2024 with respect to fiscal year 2023. Proposed phase-in periods are summarized in the annex of this publication.

Preparing for new disclosures. As proposed, the rules could apply to large accelerated filers as soon as their annual report on Form 10-K or Form 20-F for fiscal year 2023. Companies may not be in a position to wait for the final rules before they consider how to begin collecting 2023 GHG emissions data and other information necessary to comply with the potential disclosure and financial statement requirements. Relatedly, companies should begin preparing for the new rules by evaluating the impact on their existing disclosure controls and procedures, as well as internal control over financial reporting with respect to GHG emissions and other climate-related disclosures. For additional considerations, see our publication “Enhancing Disclosure Controls and Procedures Relating to Voluntary Environmental and Social Disclosures.”

Background

As noted in our previous publications, SEC commissioners and senior staff indicated throughout 2021 the SEC’s growing focus on climate-related disclosure in public company filings (or lack thereof).2 In the proposing release, the SEC expressed its concern that even as investors have increased their demand for more detailed information about climate-related risks that companies face, the existing disclosures “do not adequately protect investors” because to the extent they are provided at all, they often appear outside of SEC filings and provide “different information, in varying degrees of completeness, and in different documents and formats.” The SEC noted in the release that the proposed rules are intended to address such information gap by eliciting “consistent, comparable, and reliable — and therefore decision-useful — information” from companies regarding the impact of climate-related risks.

Key Proposed Climate-Related Disclosure Requirements

Highlights of the proposed disclosure and other requirements include the following:

- Climate-related disclosure in a separately captioned section of registration statements and annual reports. A proposed new subpart 1500 to Regulation S-K would add extensive and prescriptive disclosure requirements for certain climate-related information, including the following:3

- the oversight and governance of climate-related risks by the board and management;

- climate-related risks reasonably likely to have a material impact on the company’s business or consolidated financial statements;

- whether and how any identified climate-related risks have affected or are reasonably likely to affect the company’s strategy, business model and outlook;

- the company’s risk management system or process and transition plan regarding climate-related risks;

- Scopes 1 and 2 GHG emissions;

- Scope 3 GHG emissions and intensity if material or the company has set a GHG emissions reduction target or goal that includes its Scope 3 emissions;4 and

- the company’s climate-related targets or goals, if any, and transition plan for achieving them and annual progress updates.

- Climate-related financial risks, metrics and related disclosure in a note to the audited financial statements. New proposed Article 14 of Regulation S-X would require a note to the audited financial statements relating to disaggregated climate-related impacts on existing financial statement line items, including financial impacts related to severe weather events and other natural conditions as well as climate-related transition activities. As part of the audited financial statements, this new disclosure would be subject to audit by an independent auditor and fall within the scope of the company’s internal control over financial reporting.

- Independent third-party assurance for Scopes 1 and 2 GHG emissions and climate-related financial disclosures (for large accelerated filers and accelerated filers only and subject to phase-in periods). The proposed rules also would prescribe minimum standards for the required independent third-party assurance.

Next Steps

Potential legal challenges. If adopted, the new rules are expected to face legal challenges, which may delay implementation of the disclosure requirements. Proposal critics include SEC Commissioner Hester Peirce who voted against the proposal and noted numerous potential “deficiencies” in a lengthy dissenting statement. In addition, in a Wall Street Journal opinion article, former SEC Chairman Jay Clayton and Congressman Patrick McHenry characterized the proposal as overreaching and outside the SEC’s authority, jurisdiction and expertise, which “will deservedly draw legal challenges.”

Public comments. The comment period will end on the later of May 20, 2022, or 30 days after the proposal is published in the Federal Register. The proposal includes specific requests for comment on numerous aspects of the proposed rules in addition to soliciting comments generally.

Phase-in Periods for Compliance With Proposed Climate Change Rules5

__________

1 Scope 1 emissions are direct GHG emissions that occur from sources controlled or owned by the company. Scope 2 emissions are indirect GHG emissions associated with the purchase of electricity, steam, heat or cooling by the company.

2 For example, see “SEC Primed To Act on ESG Disclosure,” “SEC Chair Gensler Outlines Roadmap for Climate Risk Disclosure Rulemaking” and “SEC Staff Issues Detailed Form 10-K Comments Regarding Climate-Related Disclosures.”

3 In the proposing release, the SEC noted that the proposed climate-related disclosure framework is based in part on the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD) and the standards and guidance of the GHG Protocol.

4 Notably, in light of the difficulties in calculating Scope 3 emissions, companies providing Scope 3 emissions disclosures would not be subject to liability for making a fraudulent statement unless such disclosure was made without a reasonable basis or not in good faith.

5 Assumes final rules become effective by December 2022 and the company has a December 31 fiscal year end. A company with a different fiscal year end that results in its fiscal year 2023 commencing before the final rules’ effective date would not be required to comply until the following fiscal year. For example, a large accelerated filer with a March 31 fiscal year end would not be required to comply with the new rules until its Form 10-K for fiscal year 2024, due 60 days after March 31, 2024.

_______________

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.