Introduction

The Treasury Department and the Internal Revenue Service (the IRS) recently issued a second set of proposed regulations concerning the taxation of qualified opportunity zone funds (OZ funds) and their investors. In our previous client alerts “Opportunity Zone Funds Offer New Tax Incentive for Long-Term Investment in Low-Income Communities” and “New Guidance for Opportunity Zone Funds Clarifies Important Issues, Leaves Door Open to Additional Guidance,” we outlined the basic rules of the opportunity zone (OZ) regime, described the first set of proposed OZ regulations and identified a number of issues that were left unresolved. Like the initial proposed regulations, the new proposed regulations provide thoughtful, pragmatic, policy-oriented guidance on key issues and can be expected to encourage the formation and capitalization of OZ funds by:

- allowing investors to enjoy the tax exemption for gain on OZ fund investments held for 10 years (the OZ tax exemption) in cases where the OZ fund sells assets;

- providing a grace period to allow an OZ fund to deploy cash in a commercial manner following a capital raise;

- clarifying that an investor’s outside basis in an OZ fund partnership interest is increased by the investor’s share of the OZ fund partnership’s debt, which is critically important for OZ fund partnerships focused on real estate;

- clarifying that an OZ fund can own and develop operating companies, including technology companies and service businesses;

- clarifying that an OZ fund can retain its status as such, notwithstanding certain unforeseen delays in the development of its property or the start-up of its business;

- providing rules pursuant to which an OZ fund or a qualified opportunity zone business (QOZB) (i.e., a corporation or partnership in which an OZ fund owns an interest) can lease its assets, including from related parties;

- clarifying the “substantial improvement” requirement;

- clarifying that certain real property leasing activities will satisfy the “active trade or business” requirement;

- providing safe harbors for the 50% income test applicable to QOZBs;

- clarifying that an OZ fund can reinvest asset sale proceeds in qualified opportunity zone property (QOZP);

- narrowing the types of events that will trigger an OZ investor’s deferred gain; and

- clarifying that an investor can use OZ-eligible capital to acquire an OZ fund interest on the secondary market, which will increase the liquidity of OZ fund interests generally and provide OZ fund sponsors with the ability to warehouse OZ fund interests pending syndication to OZ fund investors.

Although the regulations will become effective once finalized, a taxpayer may generally rely on them before then as long as the taxpayer applies the rules consistently and in their entirety. A taxpayer’s ability to rely on the rules, however, does not extend to certain rules regarding the application of the OZ tax exemption to the disposition of an OZ fund interest. Although these rules will not become relevant until January 1, 2028 (at the earliest), they may be germane to structuring decisions made when the OZ fund is formed and acquires a QOZB, and the inability of taxpayers to rely on them is of concern.

Below is a summary of key provisions of the new proposed regulations and a discussion of important issues that remain unaddressed.

I. OZ Tax Exemption Available for Certain OZ Fund Asset Sales

Perhaps the most powerful incentive provided by the OZ regime is the OZ tax exemption, which allows eligible investors to exclude gains realized on the sale of an OZ fund interest held for at least 10 years. The statute is unclear whether the exemption applies in circumstances other than the sale by an investor of its OZ fund interest. This caused concern particularly among investors in and sponsors of multi-asset OZ funds organized as partnerships or REITs, where, but for the requirements of the OZ regime, liquidity events would generally take the form of asset sales by the OZ fund or its subsidiaries. The new proposed regulations helpfully allow investors that satisfy the 10-year holding period to enjoy the OZ tax exemption on certain gains passed through to them when the OZ fund sells its assets.

It is important to note, however, that, depending on the structure of the OZ fund and the level at which gain is recognized, similarly situated investors may experience disparate tax results, although it is not clear that these differences were intended. For example, it is clear under the new proposed regulations that an eligible investor that sells an OZ fund interest will not be subject to depreciation recapture with respect to assets held directly or indirectly by the OZ fund and that the investor can avail itself of the OZ tax exemption even if the OZ fund holds assets that are not QOZP. This is true regardless of whether the OZ fund is a partnership, an S corporation, or a REIT. Conversely, it would appear that, in the case of an OZ fund organized as a partnership or an S corporation, eligible investors will enjoy the OZ fund tax exemption only with respect to capital gains recognized by the OZ fund on the sale of QOZP and not with respect to gains characterized as ordinary income1 or gains recognized by the OZ fund on the sale of non-QOZP assets (such as intangibles and securities other than equity interests in a QOZB). The exemption also does not seem to apply to gains recognized on the sale of assets by a QOZB, whether or not such assets constitute QOZP. Accordingly, although the new proposed regulations expand the options for an OZ fund to exit an investment, these differences in income tax consequences may limit the ability of investors to avail themselves of these options.

In the case of an OZ fund REIT, the OZ tax exemption seems to apply with respect to any capital gain dividends attributable to long-term capital gains, whether recognized at the OZ fund level or by a QOZB, although it is unclear whether the exemption is limited to capital gains recognized on the sale of QOZP. In addition, because the new proposed regulations specifically extend the OZ tax exemption only to REIT capital gain dividends, it seems dividends attributable to depreciation recapture would not be eligible for the exemption. As a consequence, some REIT OZ funds may find it prudent to structure a liquidity event as a sale of REIT assets followed by a series of liquidating distributions, rather than as a series of non-liquidating capital gain dividends. This is because the former structure entitles the OZ fund investor to the OZ tax exemption on all distributions made by the REIT in liquidation, including distributions in respect of non-QOZP assets and attributable to depreciation recapture.

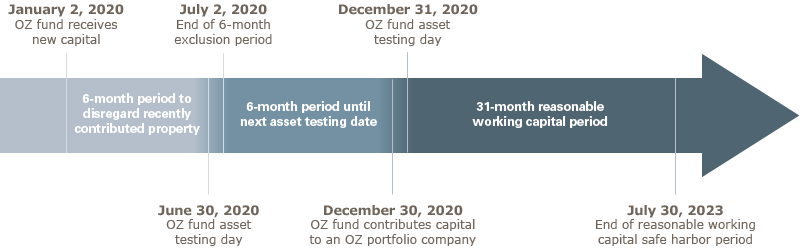

II. 90% Asset Test Excludes Newly Raised Capital for Six Months, Potentially Extending Capital Deployment Period to as Long as 43 Months

Under the statute, no more than 10% of an OZ fund’s assets may consist of non-QOZP, including cash held as working capital, and a QOZB can hold only limited amounts of cash in excess of its reasonable working capital needs. These restrictions, together with the requirement that investors acquire their OZ fund interests within 180 days of a capital gain realization event, hindered the capital raising efforts of many OZ funds because a large enough inflow of capital shortly before an asset testing date could cause an OZ fund to fail the 90% asset test if the cash could not immediately be put to use. This issue was particularly pronounced for OZ funds that rely on a continuous equity offering mechanism given the increased likelihood that such funds might receive significant equity capital shortly before the June 30 testing date, which is the last opportunity for investors to roll over capital gains realized in the prior calendar year.

The new proposed regulations provide relief by permitting an OZ fund to exclude contributed capital from the 90% asset test for six months after it is received from investors, as long as it is held in cash, cash equivalents, or short-term debt instruments. This rule, combined with the reasonable working capital safe harbor discussed below and in our previous client alerts, can provide an OZ fund with a capital deployment period that is as long as 43 months. For example, a previously existing calendar-year OZ fund that raises capital on January 2 could disregard the capital until July 2 and, therefore, would not be required to include the capital in its June 30 asset test. On December 30 (the day before its next asset testing date) the OZ fund could contribute the capital into a QOZB, which would have 31 months to use the capital under the reasonable working capital safe harbor. This would give the OZ fund 43 months to deploy the capital, as depicted in the following timeline (dates for illustration only):

III. OZ Fund Partnership Liabilities Increase Outside Basis of OZ Fund Partnership Interests

The OZ regime encourages new development of real estate, as well as the rehabilitation of existing structures. It is common for a property-owning partnership engaged in such a project to refinance the project upon stabilization to repay acquisition and construction loans and distribute excess cash to investors. Ordinarily, such a leveraged distribution does not give rise to investor-level gain because each investor’s basis in its partnership interest will generally include its share of the partnership’s liabilities, such that the cash distributed to an investor will generally not exceed the investor’s basis in its partnership interest. In addition, the additional basis increase attributable to the partnership’s debt typically allows an investor to take depreciation deductions in excess of its investment in the partnership.

The OZ statute, however, states that an investor’s basis in its OZ fund interest is initially zero and is adjusted upwards only after certain holding period requirements are satisfied. Although Congress clearly contemplated that an OZ fund could be formed as a partnership and could invest in lower-tier partnerships, neither the statute nor the initial proposed regulations addressed how the general rules of partnership taxation, including the rules that determine an investor’s basis in an OZ fund partnership interest, would apply. As a consequence, it was unclear whether, prior to the time at which an investor’s basis in its OZ fund interest is stepped up under the OZ rules, leveraged distributions made by an OZ fund partnership would cause its investors to recognize gain and depreciation deductions that might otherwise be enjoyed would be deferred or disallowed.

The new proposed regulations generally eliminate these uncertainties and provide that an investor’s basis in an OZ fund partnership interest is increased by its share of the OZ fund partnership’s liabilities (including liabilities allocated to the OZ fund by a partnership in which the OZ fund is a partner), just as it would be outside the OZ regime. This basis increase, in most cases, should be sufficient to allow an investor in an OZ fund partnership to avoid gain recognition as a result of its allocable share of the OZ fund partnership’s leveraged distributions and to enjoy depreciation deductions as it otherwise would under the partnership tax regime.

The beneficial rules for partnership distributions are subject to an important caveat: a distribution made by an OZ fund partnership will cause an investor to recognize gain and cause an investor’s interest in the OZ fund to lose its status as a qualifying OZ fund investment if the distribution, together with the investor’s contribution to the OZ fund, is characterized as a disguised sale. For these purposes, any cash contributed by the investor is treated as non-cash property (thus potentially subject to the disguised sale rules) and the exception to disguised sale treatment for leveraged distributions is unavailable. Accordingly, as a practical matter, leveraged distributions that occur within two years of an investor’s contribution to an OZ fund partnership will be treated as a disguised sale, causing the investor to recognize gain and disqualifying all or a portion of its interest as a qualifying OZ fund investment. Conversely, leveraged distributions occurring two years after the investor’s contributions should not result in disguised sale treatment.

An investor in an OZ fund organized as a C corporation, an S corporation, or a REIT will generally not enjoy similar benefits because the investor’s basis in its OZ fund interest will not be adjusted for debt incurred at the OZ fund level or below. As a consequence, investors that prioritize leveraged distributions and depreciation deductions will likely prefer OZ fund partnerships for real estate development projects.

IV. Reasonable Working Capital Safe Harbor Expanded

As described above and in our prior client alerts, the statute imposes strict limitations on the amount of cash and cash equivalents that both OZ funds and QOZBs may hold. At the QOZB level, however, the limitations do not apply to “reasonable” working capital. The initial proposed regulations clarified that the amount of working capital maintained by a QOZB would be deemed to be reasonable if the following requirements were satisfied:

- The amount is designated in writing for the acquisition, construction and/or substantial improvement of tangible property within the opportunity zone;

- The QOZB prepares a written schedule that provides for the expenditure of the amount within 31 months of the QOZB’s receipt thereof and is consistent with the ordinary start-up of a trade or business; and

- The working capital assets are actually used in a manner that is “substantially consistent” with the previous two requirements.

Although helpful with respect to amounts necessary for the acquisition and improvement of tangible property, this initial version of the safe harbor failed to provide guidance with respect to amounts necessary for other business expenses, such as payroll, which was of particular concern for OZ funds engaged in businesses other than real estate development. For example, QOZBs in the services or technology industries may require significant working capital to fund the formation, acquisition, or expansion of a business and to pay employees and contractors pending revenue sufficient to cover expenses.

The new proposed regulations alleviate this concern by expanding the safe harbor to include working capital used for the development of any trade or business in an opportunity zone, including amounts necessary for hiring staff and acquiring intangibles, such as permits.

The new proposed regulations also identify circumstances in which deviation from the written schedule is permissible. Specifically, exceeding the 31-month safe harbor period will not violate the safe harbor if the delay is attributable to a delay in government action on an application, as long as the application was completed during the 31-month period. Although this addition is welcome, it is not entirely clear whether relief is available if, for example, a QOZB knows that a certain government action generally takes no less than 12 months while subsequent construction is likely to take another 20 months. This rule also does not address other legitimate deviations from the plan (e.g., natural disasters, disruption in the credit markets, labor market unrest, etc.).

Finally, the new proposed regulations clarify that the same QOZB can benefit from multiple overlapping or sequential reasonable working capital safe harbor plans. This is particularly helpful for real estate developers seeking phased developments and businesses that wish to capitalize on opportunities to pursue new lines of business.

It is worth emphasizing that the reasonable working capital safe harbor continues to apply only at the QOZB level. Accordingly, an OZ fund cannot hold more than 10% of its assets in cash and other nonqualifying assets.

V. Rules Regarding Leased Tangible Property and Related-Party Leases Clarified

The statute provides that a corporation or partnership will qualify as a QOZB if, among other things, substantially all of the tangible property “owned or leased” by the entity is “qualified opportunity zone business property” (QOZBP). This language leaves little doubt that a QOZB is permitted to lease tangible property. Such property clearly will not be a “good” asset, however, unless it constitutes QOZBP. Under the statute, tangible property will not qualify as QOZBP unless (1) it is acquired by purchase from an unrelated party after December 31, 2017, (2) its original use in the opportunity zone begins with the QOZB or the QOZB substantially improves the property, and (3) during substantially all of the QOZB’s holding period for the property, substantially all of its use is in the opportunity zone. Because leased property is, by definition, not acquired by purchase and because the original use of leased property located inside an opportunity zone will generally begin with the lessor (who placed the property in service), it was not clear how leased property could satisfy these requirements. Because much of the property used in businesses is leased and not purchased, clarity on this point was critical.

Fortunately, the new proposed regulations provide practical guidance. Leased tangible property will generally qualify as QOZBP if four criteria are satisfied: (1) the taxpayer must enter into the lease for the tangible property after December 31, 2017, (2) during substantially all (90% or more) of the period for which the OZ fund or QOZB leases the tangible property, substantially all (70% or more) of the use of the leased property must be in the opportunity zone, (3) the terms of the lease must reflect arm’s-length terms, and (4) for real property (other than unimproved land), there cannot exist, at the time the lease is entered into, a plan, intent, or expectation that the OZ fund will purchase the property for other than fair market value determined at the time of purchase and without regard to prior lease payments.

The new proposed regulations explicitly permit related-party leases, which is especially helpful for investors that already own property in an opportunity zone and wish to lease that land into an OZ fund or QOZB in which the investor owns an interest. Such leases are subject to certain additional requirements, however. Specifically, in the case of a related-party lease, (1) the lessee (OZ fund or QOZB) may not make prepayments in connection with the lease relating to a period of use of the property that exceeds 12 months and (2) in the case of a lease of tangible personal property, the lessee must become owner of tangible QOZBP with a value at least equal to the value of leased tangible personal property before the earlier of the last day of the lease or 30 months after receiving the property under the lease. The latter requirement applies only if the original use of the leased tangible personal property in the opportunity zone did not begin with the lessee.

Finally, the new proposed regulations provide rules for determining the value of leased property for purposes of the 90% asset test at the OZ fund level and the 70% QOZBP asset test at the QOZB level. Like purchased property, leased tangible property may be valued as reported on an applicable financial statement prepared according to GAAP, but only if GAAP requires recognition of the lease. Alternatively, a taxpayer may treat leased tangible property as having a value equal to the sum of the present values of all payments to be made under the lease, discounted at the applicable federal rate. A taxpayer must apply its chosen method consistently across all of its leased property.

VI. ‘Substantial Improvement’ Determined on an Asset-by-Asset Basis

Under the statute, if tangible property has been previously used in an opportunity zone, such property cannot constitute QOZBP unless it has been substantially improved, i.e., the OZ fund or the QOZB must, within 30 months, make capital improvements to the property in amounts greater than its initial tax basis in the property. Under the new proposed regulations, the substantial improvement requirement must be applied to purchased tangible property on an asset-by-asset basis. Thus, for example, if an OZ fund acquires four buildings for $100x each as part of a single project, it must double the tax basis of each and every building it needs to qualify as QOZBP. This is so even if, from a commercial perspective, it would make sense to invest an aggregate of $401x in only one or two of the buildings. As a consequence, the asset-by-asset approach may discourage investments that would otherwise represent the most efficient use of capital. It can also be onerous and impractical, especially for operating businesses with significant and diverse assets, a concern explicitly acknowledged in the preamble. In fact, Treasury and the IRS requested comments on this point, including whether a group of interrelated tangible assets should be aggregated as a single asset for purposes of the substantial improvement requirement.

VII. Active Trade or Business Requirement Clarified

The statute requires that a QOZB derive at least 50% of its gross income from the active conduct of a trade or business in an opportunity zone and that it use a substantial portion of its intangible assets in such trade or business. Similarly, tangible property must be used in a trade or business to qualify as QOZBP. Yet neither the statute nor the initial proposed regulations define “trade or business” (or the active conduct thereof) for these purposes. As a consequence, it was not clear whether businesses historically considered passive under the tax law, such as certain real estate leasing businesses, could satisfy these requirements.

The new proposed regulations provide guidance by clarifying that “trade or business” generally has the same meaning in the opportunity zone context as it has for other purposes of the Internal Revenue Code.2 Although the determination whether an activity is a trade or business under other code sections is highly fact-dependent and can, in many cases, be uncertain, the new proposed regulations helpfully provide that, for purposes of the section 1397C requirements incorporated into the definition of “qualified opportunity zone business,” the ownership and operation (including leasing) of real property constitutes the active conduct of a trade or business. Under this rule, ownership and operation of real property requires something more on the part of the taxpayer than “merely entering into a triple-net-lease,” but the regulations provide little insight as to the level of activity required to distinguish a “good” lease from a triple-net- lease for these purposes, other than implying existing law on triple-net-leases applies.

VIII. Three Safe Harbors Provided for the 50% Gross Income Test

Under the statute, a QOZB must derive at least 50% of its gross income from the active conduct of trade or business within an opportunity zone, but neither the statute nor the initial proposed regulations provide any rules on how to determine whether the requirement is satisfied. The lack of guidance caused uncertainty regarding whether operating businesses located inside an opportunity zone could derive “good” income from services or products delivered to customers located outside the zone.

The new proposed regulations provide three safe harbors under which a QOZB will be deemed to satisfy the 50% gross income test:

- At least 50% of the services performed by employees and independent contractors, based on hours, are performed within the opportunity zone;

- At least 50% of the services performed by employees and independent contractors, based on the amounts the QOZB pays for such services, are performed in the opportunity zone; or

- The tangible property of the business in the opportunity zone and the management or operational functions performed for the business in the zone are each necessary to generate at least 50% of the gross income of the business.

If none of these safe harbors apply, the determination is made based on all the facts and circumstances.

Although it is useful to understand that the 50% gross income test can be satisfied based on hours worked and amounts paid, there is no guidance on how to determine whether services will be treated as performed within an opportunity zone or which types of service providers will qualify as independent contractors (rather than vendors) under these rules. For example, it is not clear whether a QOZB is required to treat amounts paid for third-party data-center or tech-support services provided from outside the opportunity zone as “bad” in its safe harbor calculations, nor is it clear whether the relationship between a QOZB and a data-center operator is one of customer and service provider or tenant and landlord. The rules also fail to prescribe standards for tracking hours worked and amounts paid for safe harbor purposes and it is not clear how, as a practical matter, such data is to be obtained from independent third-party vendors and service providers. For example, will QOZBs subject service providers to cumbersome and off-market record-keeping and reporting requirements? What about employees of a QOZB that sometimes work remotely or respond to emails while traveling? What if a QOZB operating in an opportunity zone hires an agency to advertise its business outside the zone? Without additional guidance, neither of the first two safe harbors can be relied upon without significant analysis regarding whether and the extent to which meaningful services provided by anyone outside the opportunity zone must be taken into account. To avoid these issues, many OZ funds will likely prefer to rely on the third safe harbor, which, in the first instance, may be best suited for OZ funds in the real estate industry.

IX. New Capital Redeployment Rules Provide 12-Month Reinvestment Period

The statute directs Treasury to provide rules allowing an OZ fund a reasonable period of time to reinvest the proceeds from the sale or disposition of QOZP. In response, the new proposed regulations provide that, for purposes of the 90% asset test, any such proceeds will be treated as QOZP as long as they are reinvested in QOZP within 12 months after the OZ fund’s receipt thereof and, prior to reinvestment, the proceeds are held in cash, cash equivalents, or short-term debt instruments. As in the working capital safe harbor provisions, the regulations grant relief if a failure to meet the 12-month deadline is attributable to a delay in government action if the application for the action was completed during the 12-month period. Combining the 12-month reinvestment period with the 31-month working capital safe harbor, as well as the fact that an OZ fund’s 90% asset test is tested every six months, could provide up to 49 months for capital redeployment.

Note, however, that this reinvestment rule does not defer the recognition of gain on the assets sold, as section 1031 would, for example. Thus, the OZ fund (and, in the case of an OZ fund that is a partnership or a REIT, its investors) will recognize the gain notwithstanding the reinvestment. Because the most salient tax benefit offered by the OZ legislation is the OZ tax exemption, and because any capital redeployment is likely to occur prior to 2028 (when all OZ designations expire), this provision likely will not be useful for appreciated QOZP, although it will certainly help OZ funds redeploy capital out of losing investments.

X. Narrowing of Potential ‘Inclusion Events’

Under the statute, an OZ fund investor must include its deferred gain in income on the earlier of (1) the date on which the investment is sold or exchanged or (2) December 31, 2026. Because the tax law defines “exchange” to include a wide variety of transactions in which property is moved from one regarded entity to another, there was concern that routine transactions, such as holding company formations and intragroup restructurings, might result in the acceleration of deferred gain and loss of the OZ tax exemption. The new proposed regulations address this concern by identifying those transfers that will be treated as “inclusion events,” those that will not be treated as inclusion events, and those that will allow the transferee to step into the shoes of the transferor with respect to the OZ tax exemption.

Except in certain cases where the transaction would otherwise be tax-free, an inclusion event will generally occur when an OZ fund investor cashes out or reduces its equity interest in the OZ fund. Notably, distributions (even pro rata distributions) from an OZ fund in excess of basis can be inclusion events that accelerate an investor’s deferred gain. This rule seems particularly harsh in the case of pro rata distributions of operating cash flow by OZ fund corporations, given that the OZ asset tests restrict the ability of OZ funds and QOZBs to hold cash.

Transactions that are not inclusion events include, for example, the contribution of an OZ fund interest to a partnership in exchange for a partnership interest, certain mergers involving OZ funds and entities that own interests in OZ funds, and certain corporate spin-offs. The rule that permits an OZ fund corporation to divide into two OZ funds would not appear to apply to OZ fund partnerships, although it is not clear whether this omission (if it exists) was intentional.

With one notable exception, transfers of corporate stock and partnership interests generally do not create adverse results for lower-tier entities that either hold or are classified as OZ funds. The exception applies in the context of transfers of interests in S corporations that directly own interests in OZ funds. If such a transfer results in a greater than 25% change of ownership in the S corporation, then the S corporation must recognize all of its deferred gain and will lose the ability to enjoy the OZ tax exemption. Unless this rule is changed, holding an OZ fund interest at the S corporation level would seem to be ill-advised, and S corporation shareholders experiencing gain through the S corporation itself should consider making their OZ fund investment outside the S corporation chain.

The transfer of an OZ fund interest by reason of an investor’s death also is not an inclusion event, nor is the contribution of an OZ fund interest to a grantor trust deemed to be owned by the transferor. In each such case, the transferee’s holding period for the OZ fund interest will include that of the transferor, which apparently means the transferee will be eligible to enjoy the OZ tax exemption if it completes the 10-year holding period. The pre-death conversion of a grantor trust into a complex trust, or vice versa, is an inclusion event; whereas the conversion of a grantor trust into a complex trust at the grantor’s death is not. The basis of an OZ fund interest is not stepped-up to its fair market value upon a transfer at death; accordingly, any gain deferred at the time of the original investment (reduced by basis adjustments under the OZ regime and any portion of such gain previously taken into account) will be includible by the transferee as income in respect of a decedent on the earlier of (1) the date on which the OZ fund interest is sold or exchanged or (2) December 31, 2026.

Given the disparities in the treatment of transfers of different types of OZ funds to and among different types of business and trust entities, whether an inclusion event has occurred and the consequences thereof will depend on not only the structure of the OZ fund, but also on the level in the investor’s ownership chain at which the OZ fund investment is made and the entity classification of the vehicle used to make the investment. Accordingly, the structure of an OZ fund investment continues to be paramount for maximizing the benefits of the OZ fund regime and should be carefully considered at the outset.

XI. Secondary Market Acquisitions of OZ Fund Interests Eligible for OZ Tax Exemption

The statute and the initial proposed regulations are silent as to whether an otherwise eligible investor can avail itself of the OZ tax exemption with respect to an OZ fund interest purchased on the secondary market (as distinguished from an OZ fund interest acquired at original issuance from the OZ fund itself). This raised concerns that selling an OZ fund interest on the secondary market would be difficult, which, in turn, complicated marketing efforts. It also prevented sponsors from warehousing OZ fund interests prior to syndication, which complicated the formation of OZ funds and the development of QOZBs.

The new proposed regulations address these issues by allowing an investor to make a gain deferral election on the acquisition of an OZ fund interest from a person other than the OZ fund, which may facilitate OZ fund investments where eligible gains are recognized only after an OZ fund has been closed and capitalized, whether by seed investors or by a sponsor. The purchaser would not inherit the seller’s holding period, however, which, in certain cases, might deny the purchaser the opportunity to satisfy the 10-year holding period requirement before the OZ fund experiences a liquidity event. For example, a sponsor may plan for a liquidity event to occur shortly after the 10th anniversary of the final capital contribution to its OZ fund. In this circumstance, a secondary market purchaser that acquires an interest after the date of the final capital contribution might assume the risk that the liquidity event will occur less than 10 years after the beginning of the purchaser’s holding period.

Conclusion

Questions left unaddressed by the initial proposed regulations caused many investors to slow or even table investments in OZ funds. In the new proposed regulations, Treasury and the IRS pragmatically addressed a number of their concerns and established a sensible framework under which many such investors will likely feel comfortable enough to move forward. We are encouraged by the realistic and policy-orientated approach Treasury and the IRS have been taking with respect to the OZ regime, and, although there are still some issues left to be resolved, we believe the regulations to date provide investors a solid path forward as they await further favorable guidance and clarity.

_______________

1 Such as gains attributable to unrealized receivables and inventory items.

2 The new proposed regulations adopt the meaning of “trade or business” from section 162, under which there has been developed an extensive body of case law and authorities as to the meaning of the phrase.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.