The Tax Cuts and Jobs Act enacted in late December 2017 created a new capital gains exemption for taxpayers who make long-term investments in low-income communities that have been designated by the Treasury Department as “opportunity zones.” Following the completion of the six-month designation process, such zones now exist in every state, and roughly 12 percent of the nation’s land mass, including all of Puerto Rico, lies in an opportunity zone. Every major city has at least one opportunity zone, and the zones also exist in suburban and rural areas. Some opportunity zones in the West and Southwest appear to be larger than some of the smaller states in the Northeast.

The centerpiece of the opportunity zone legislation is a new type of investment vehicle called an opportunity zone fund (an “OZ fund”). The legislation encourages investment in opportunity zones by permitting a taxpayer to sell existing appreciated assets and “roll” the amount of realized gain (the “qualified gain amount”) into an OZ fund within 180 days of realization. Thus, the opportunity zone legislation does not seek merely to increase investments in low-income communities; its goal is to reallocate capital to these investments from appreciated investments outside the zone.

The opportunity zone legislation provides a powerful tax incentive to encourage such capital reallocation: If an investor rolls the qualified gain amount into an OZ fund and holds the OZ fund interest for at least 10 years, the taxpayer will not recognize any gain on the post-acquisition economic appreciation in its OZ fund interest (the “OZ tax exemption”).

The legislation does not seek merely to increase investments in low-income communities; its goal is to reallocate capital to these investments from appreciated investments outside the zone.

The capital reallocation feature gives rise to the key limiting feature of the legislation: A taxpayer is entitled to the OZ tax exemption only with respect to an OZ fund interest (an “eligible OZ fund interest”) acquired by the taxpayer for an amount no greater than the qualified gain amount. The portion of an OZ fund interest attributable to any capital invested in excess of the qualified gain amount is not eligible for the OZ tax exemption. Thus, although a taxpayer is free to invest cash into an OZ fund in unlimited amounts, the benefit of the OZ tax exemption is limited to the portion of the OZ fund interest acquired with respect to a qualified gain amount realized on the sale of an existing appreciated asset. In addition, it is extremely difficult for a taxpayer to contribute appreciated assets to an OZ fund; indeed, such a contribution could prevent the OZ fund from qualifying as an OZ fund.

The requirement that a taxpayer sell an existing appreciated asset in order to benefit from the opportunity zone legislation amounts to a toll charge on the acquisition of an eligible OZ fund interest. To mitigate the toll charge, the recognition of gain realized on the sale of the appreciated asset is deferred until the end of 2026, and the amount of gain ultimately subject to tax is reduced by 10 percent for a taxpayer who holds its OZ fund interest for at least five years, and by an additional 5 percent (for a total of 15 percent) for a taxpayer who holds its OZ fund interest for at least seven years. Thus, a taxpayer desiring to take maximum advantage of the toll-charge reduction needs to make its OZ fund investments by the end of 2019, and there will be no reduction in the toll charge for a sale of an existing asset after 2021. Appendix A contains examples illustrating the operation of the OZ tax exemption and the deferral feature.

Although it can accommodate a wide variety of businesses, an OZ fund is particularly well-suited for certain types of real estate development projects, certain infrastructure and energy projects, and certain types of technology and service businesses. As follow-up to this mailer, which provides a broad overview of the opportunity zone legislation, we expect to address narrower, industry-specific considerations in one or more future mailers.

Summary of the Statute

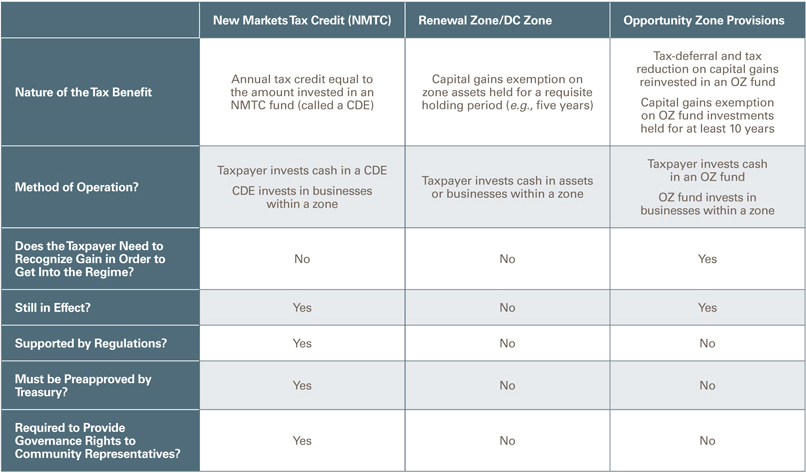

The opportunity zone legislation is the latest in a series of tax-incentive programs designed to encourage investment, jobs and economic growth in low-income or economically distressed communities. In terms of operational provisions and statutory language, the opportunity zone legislation draws substantially from the new markets tax credit (NMTC) and empowerment zone provisions. Appendix B describes the similarities and differences among the three regimes.

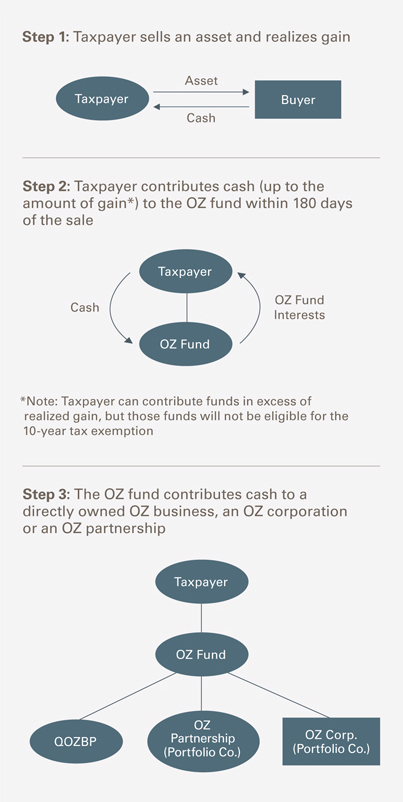

As illustrated in Figure 1 below, at a high level, the OZ fund concept is simple: A taxpayer sells appreciated assets and, within 180 days, contributes cash in an amount not greater than the qualified gain amount to an OZ fund in exchange for an eligible OZ fund interest; the OZ fund uses that cash to invest in one or more opportunity zone businesses, either directly or through a subsidiary partnership or corporation; and the taxpayer reports the deferred gain in 2026 (such gain reduced, as appropriate) and, after 10 years, can sell its eligible OZ fund interest free of U.S. federal income tax, regardless of how much the eligible OZ fund interest has increased in value.

Figure 1

Despite this conceptual simplicity, the details of structuring an OZ fund can be complicated by certain statutory requirements. Compliance with the technical provisions of the statute are important, as a failure to comply could disqualify the OZ fund, potentially resulting in a significant penalty tax (discussed in more detail below) or even eliminating the deferral of gain and the OZ tax exemption.

In order to qualify as an OZ fund, an entity must establish that at least 90 percent of its assets, calculated as the average of two semiannual testing dates, are qualified opportunity zone property (QOZP). QOZP consists of (i) qualified opportunity zone business property (QOZBP), (ii) qualified opportunity zone corporate stock, or (iii) qualified opportunity zone partnership interests. For simplicity, we refer to issuers of qualified opportunity zone corporate stock and qualified opportunity zone partnership interests as “OZ portfolio companies.”

The key definitions of the opportunity zone legislation are:

- Qualified Opportunity Zone Business Property. The term “QOZBP” is central to the definitions of OZ fund and OZ portfolio company. QOZBP means tangible property used in a trade or business if (i) such property is acquired by purchase after 2017; (ii) the original use of the property in the zone commences with the tested entity (e.g., an OZ fund or an OZ portfolio company) or the tested entity substantially improves the property; and (iii) during substantially all of the tested entity’s holding period for the property, substantially all of the use of the property is in the zone. An entity is treated as substantially improving property if, during any 30-month period, the entity makes capital expenditures with respect to such property at least equal to the property’s acquisition cost.

- OZ Portfolio Company Requirements. In order for equity of an OZ portfolio company to qualify as QOZP in the hands of an OZ fund, (i) the OZ fund must acquire its equity interest in the OZ portfolio company for cash at original issuance after 2017; (ii) the OZ portfolio company must be a qualified opportunity zone business (or, if newly formed, organized for the purpose of becoming a qualified opportunity zone business); and (iii) during substantially all of the OZ fund’s holding period, the OZ portfolio company must be a qualified opportunity zone business.

- Qualified Opportunity Zone Business. A qualified opportunity zone business (sometimes referred to herein as an “OZ business”) is a trade or business (i) in which substantially all of the tangible property (if any) owned or leased by the business is QOZBP; (ii) at least 50 percent of the gross income (presumably of the OZ portfolio company being tested) is derived from the active conduct of a trade or business in the opportunity zone; (iii) a substantial portion of the intangible property of the entity is used in the active conduct of such business; (iv) less than 5 percent of the basis of the property of such business is attributable to “nonqualified financial property”; and (v) the entity does not engage in, or lease land to, a so-called “sin business” (which includes a golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack, gambling facility and liquor store). The term “nonqualified financial property” means debt, stock, partnership interests and certain types of derivatives but does not include cash and short-term debt instruments held as reasonable working capital.

Issues and Considerations

The foregoing definitions and the other provisions of the opportunity zone legislation create a number of issues and considerations for a taxpayer wishing to avail itself of the OZ tax exemption. These issues and considerations will affect decisions regarding structural and operational matters that affect every stage of an OZ fund investment — from the sale transaction by which the qualified gain amount is recognized, to the formation and financing of the OZ fund itself and any OZ portfolio company, to the acquisition and operation of the OZ fund’s or an OZ portfolio company’s assets, to a taxpayer’s exit from its OZ fund investment. The following is a non-exhaustive list of important issues and considerations.

Who Is the Taxpayer? As currently written, the statute requires that the exact same taxpayer that sold the existing asset at a gain be the investor in the OZ fund. In addition, once an OZ fund interest is acquired, the deferred gain on the existing asset is accelerated if the OZ fund interest is transferred — even upon a transfer to an affiliate in a nonrecognition transaction. Accordingly, if a partnership is the seller of the existing asset, the ownership of the asset or the holdings of the partners may need to be restructured if the partners differ on whether to invest the sales proceeds in an OZ fund. Similarly, if a trust owns the asset that is to be sold, careful consideration must be given to the tax classification of the trust and whether that status is expected to change, as a change could affect the timing of recognition on the deferred gain and, possibly, the availability of the OZ tax exemption itself.

Capital Infusions. Taxpayers will also need to manage the infusion of capital into an OZ fund and any OZ portfolio company owned by the OZ fund. Unlike a typical investment fund, no more than 10 percent of an OZ fund’s assets can consist of cash and intangible assets as of its six-month and year-end testing dates. In addition, if an OZ portfolio company maintains cash beyond its then-current reasonable working capital needs, such excess cash may not represent more than 5 percent of the assets of such OZ portfolio company. If an OZ portfolio company fails this test, an OZ fund that owns equity in the OZ portfolio company may lose its status as an OZ fund. These issues can be managed through a variety of techniques, including staging capital calls into OZ funds and using revolving credit facilities and other forms of leverage at the OZ portfolio company to ensure that cash in excess of reasonable working capital is available to be deployed in a way that complies with the asset tests.

Capital Structure. The use of a capital structure that provides for non-pro rata distributions — such as a structure that has both common and preferred interests or certain structures that involve “carried interests” — may not be appropriate for an OZ fund. The opportunity zone legislation provides Treasury with broad power to issue rules to “prevent abuse,” and it is important to bear in mind that the NMTC regime, from which large portions of the opportunity zone legislation was drawn, views certain types of non-pro rata distributions as abusive. If non-pro rata economics are desired, it may be prudent to use a structure in which multiple OZ funds (each one providing for pro rata sharing) own different classes of interests in the applicable OZ portfolio company.

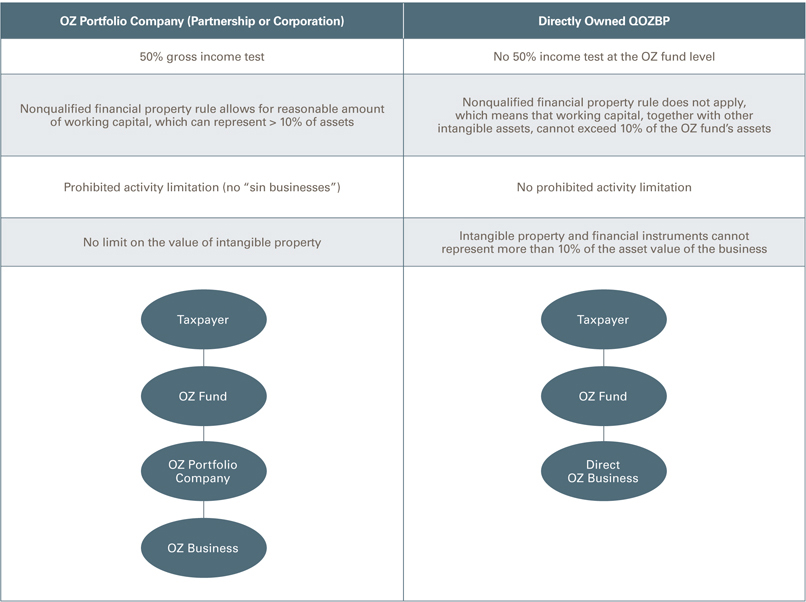

Use of OZ Portfolio Companies. The most basic structural decision that any OZ fund must make is whether to invest in an OZ business directly or whether to hold its OZ business through an OZ portfolio company. Because of the different rules that apply under these circumstances (the key examples of which are illustrated in Appendix C), this decision is surprisingly consequential. Below are some of the key differences and uncertainties that will inform that decision.

- Intangibles and Working Capital. Among the most surprising differences between the rules governing OZ funds and OZ portfolio companies are that the OZ fund asset test that applies to a directly conducted business requires the business to own tangible property and significantly limits the ability of the business to own intangible property or reasonable working capital; by contrast, the test applicable to an OZ portfolio company does not require the business to own tangible property and does not limit the amount of intangible assets or reasonable working capital that the business can own,1 as long as a substantial portion of its intangible assets are used in the active conduct of a trade or business within the opportunity zone.2 Thus, the statute would appear to prohibit an OZ fund from directly conducting a business that relies heavily on intangible assets and reasonable working capital. For this reason alone, we anticipate that, pending further guidance, most OZ businesses will be conducted through portfolio companies. Except as otherwise indicated, the balance of this piece assumes that an OZ business will be operated through one or more OZ portfolio companies.

- Startup OZ Portfolio Companies. One of the primary goals of the opportunity zone legislation is the creation of new opportunity zone businesses. One prong of the OZ fund asset test allows an OZ fund to hold equity of a new OZ portfolio company formed for the purpose of becoming a qualified OZ business in the future. The next prong provides that, in order for equity in an OZ portfolio company to constitute QOZP, the OZ portfolio company must be engaged in a qualified OZ business during substantially all of the OZ fund’s holding period in the portfolio company’s equity. Given that a business may require a year or more to become operational (and thereby satisfy the trade or business test), and that the OZ fund asset test is effectively tested every six months, some commentators have expressed concern that the statutory language could conceivably be interpreted as precluding startups that take more than a few months to become operational. By analogy, the NMTC regulations treat a startup business as an active trade or business if the business is reasonably expected to produce revenue within the first three years. If this rule were applied to, or incorporated into, the OZ fund regime, it would facilitate the creation of startup businesses in an opportunity zone.

- OZ Portfolio Company Income Test. An OZ portfolio company must satisfy the 50 percent gross income test described above. If an OZ business fails this test (for example, during the start-up period), the status of the OZ fund, and thus the effectiveness of the initial deferral of gain recognition and the availability of the OZ tax exemption, could be jeopardized. Again, the NMTC regime may provide some guidance. An NMTC business must pass a gross income test that is similar to the gross income test applicable to OZ businesses. Under a safe-harbor rule, an NMTC business is deemed to have gross income commensurate with the amount of assets it possesses, and the amount of services it provides, inside a low-income community. Until more specific guidance tailored to the opportunity zone legislation is developed, a similar safe-harbor rule could provide clarity to taxpayers with respect to OZ fund investments.

Acquired by Purchase. In the real estate sector, one complication is the manner in which an OZ fund or OZ portfolio company obtains real estate. In order for a property to constitute QOZBP in the hands of an OZ fund or an OZ portfolio company, it must have been acquired from an unrelated party by purchase. It is common for real estate joint ventures to be formed between a property owner who contributes property in exchange for an equity interest and a developer who contributes development capital and/or services. The requirement that the property be acquired by purchase from an unrelated third party will preclude an OZ fund or an OZ portfolio company from utilizing that structure. The parties would need to consider other options, perhaps using separate land and development joint ventures, with ground leases and other forms of financing between the ventures. Even in situations where the current property owner is willing to sell property for cash and reinvest the cash proceeds in the OZ portfolio company, these types of parallel structures may need to be utilized if the existing owner would own a large enough interest in the OZ portfolio company to be treated as a “related party.”

Original Use of the Property. Another requirement for property to qualify as QOZBP is that either (i) the original use of the property must commence with the OZ fund or OZ portfolio company or (ii) the OZ fund or OZ portfolio company must make capital expenditures with respect to the property in an amount at least equal to the property’s acquisition cost. This requirement may prove challenging for an OZ fund or OZ portfolio company looking to invest in real estate. It may be impossible for the OZ fund or OZ portfolio company to prove that it is the first one to use a property during the property’s existence, leading to the conclusion that Congress did not intend that the word “original” be interpreted literally. In connection with empowerment zone provisions that contain similarly worded “original use” requirements, the Treasury Department has enacted a fair and common sense rule under which a taxpayer can satisfy the original use test with respect to any real property that has been vacant for at least a year. Until a similar rule is incorporated into the opportunity zone context, real estate developers who cannot satisfy the “substantial improvement” standard will need to either incur a degree of risk concerning the definition of “original use” or consider alternate development structures, such as those outlined above.

Activities Outside the Opportunity Zone. Any business that aspires either to grow outside an opportunity zone or locate facilities (e.g., offices, factories or warehouses) outside the zone will need to adopt an extremely flexible corporate structure and set of commercial arrangements. The statute requires that substantially all of the tangible property of an OZ portfolio company be located within the opportunity zone. The “normal” business reaction to this limitation — forming subsidiaries that operate outside the zone — is unavailable, because the statute prohibits an OZ portfolio company from owning equity in subsidiaries if such equity represents more than 5 percent of the value of the assets of the OZ portfolio company. Even if an OZ portfolio company manages to operate outside an opportunity zone without owning or leasing tangible property, more than 50 percent of the gross income of an OZ portfolio company must be attributable to business activity in the zone — a standard that, under the NMTC rules, can be satisfied through the use of tangible property or the provision of services inside the zone. Given these constraints — particularly those relating to the ownership of subsidiary equity — business expansion may have to be facilitated through more complicated arrangements, such as the use of sister companies that are owned outside an OZ fund structure or through independent service providers. This will necessarily complicate financing arrangements, licensing agreements and vendor contracts, among other things.

OZ Fund Partnerships and the Zero-Basis Rule. The opportunity zone legislation provides that a taxpayer’s basis in its eligible OZ fund interest is zero, except to the extent necessary to reflect: (i) the recognition of deferred gain; (ii) the reduction in deferred gain for OZ fund interests held for at least five years; and (iii) the OZ tax exemption. In the case of an OZ fund that is organized as a partnership, the statute, read literally, does not provide for any adjustments to the taxpayer's basis in its eligible OZ fund interest pursuant to the normal operation of Subchapter K, such as for income, losses or liabilities allocated by the OZ fund to its partners. This could result in permanent double taxation of partnership income and capital distributions (including distributions that would otherwise be eligible for tax deferred treatment due to the allocation of liabilities by the partnership to the partners). This rule also calls into question the availability of cost-recovery deductions for assets acquired by an OZ fund partnership and the extent to which any suspended losses will be available. Congress and Treasury are aware of these issues. Nevertheless, given the complexity of integrating the zero-basis rule into the existing partnership tax regime, it may be some time before these issues are addressed.

The Penalty Tax. If an OZ fund fails the asset test, the OZ fund statute imposes a monthly penalty equal to the product of the excess nonqualifying assets and the annual underpayment rate in effect for the month of the failure. Some commentators have suggested that the penalty is too large for the offense and that perhaps the penalty base should equal the amount of tax that would be due on the deferred gain, and that a monthly penalty should be based on the monthly (not annual) underpayment rate. In addition, it is not at all clear what, if anything, happens if the OZ fund fails the asset test in the same month in which a taxpayer either contributes cash to the OZ fund or sells its interest in the OZ fund. The statute could be interpreted to disqualify the fund as an OZ fund as of the sale date or contribution date, as the case may be, resulting in no deferral of gain and no OZ tax exemption. Until the consequences of such a failure are clarified, taxpayers would be well-advised to assume that an OZ fund asset test failure coinciding with either an OZ fund contribution or OZ fund sale could be catastrophic to their tax-planning objectives, and to structure accordingly.

Exiting an OZ Fund. Exiting an OZ fund investment requires particularly careful planning. The OZ tax exemption is only available if an investor sells its interest in the OZ fund. Thus, for an OZ fund that is organized as a partnership (which is likely to describe most OZ funds), the exemption does not apply when the OZ fund sells an OZ portfolio company or any other assets it owns, or when an OZ portfolio company sells its assets. Unless Congress amends the statute, this limitation is likely to discourage the creation of diversified OZ funds, which was arguably one of the goals for the opportunity zone legislation. In the meantime, it may be prudent for taxpayers to structure OZ funds with a view toward an exit through a sale of fund interests.

Finally, in situations where an investor makes multiple capital contributions to a partnership OZ fund over time, it is critical to bear in mind that the Internal Revenue Service views a partnership interest as a unified security with multiple or segmented holding periods based on when contributions are made. Consequently, for a partnership OZ fund to which the investor has made capital contributions over time, the sale of a portion of the OZ eligible fund interest before the 10th anniversary of the last OZ eligible contribution will not fully qualify for the OZ tax exemption. There may be more flexibility to make partial sales of equity interests in an OZ fund organized as a corporation if the taxpayer can specifically identify and sell only those shares that satisfy the requisite holding period.

Conclusion

If the level of investor interest and activity that we have witnessed over the past six months is any indication, the opportunity zone legislation has the potential to be a powerful driver of investment activity. The uncertainties associated with certain aspects of the legislation may, however, hamper that activity, and the manner in which these uncertainties are resolved by Congress and Treasury will likely determine the ultimate success of the program.

The following examples address only U.S. federal income tax consequences and do not include state, local or other tax consequences.

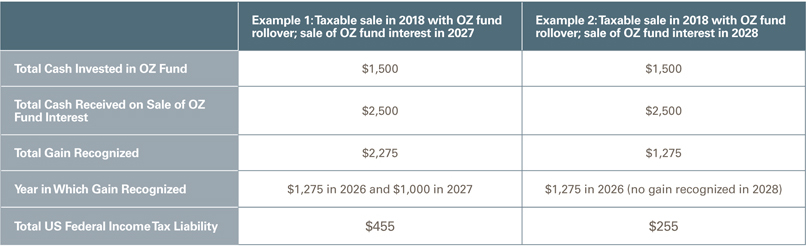

Example 1: OZ Fund Interest Sold Before Year 10

- Facts

- In 2018, taxpayer sells an asset with a basis of $1,000 and a fair market value of $2,500 for $2,500 in cash, realizing a gain of $1,500

- Taxpayer contributes $1,500 of cash to an OZ fund

- The OZ fund contributes that cash to an OZ partnership

- Taxpayer sells the OZ fund interest for $2,500 in 2027 (i.e., without satisfying the 10-year holding period)

- Tax Consequences

- Taxpayer does not recognize $1,500 of gain in 2018

- Taxpayer takes a $0 basis in its OZ fund interest

- Taxpayer’s basis in its OZ fund interest increases from $0 to $150 in 2023

- Taxpayer’s basis in its OZ fund interest increases from $150 to $225 in 2025

- Taxpayer recognizes $1,275 of gain in 2026 ($1,500 of deferred gain minus $225 of basis step-up)

- Taxpayer’s basis in its OZ fund interest increases to $1,500 as a result of 2026 gain recognition

- Taxpayer recognizes $1,000 of gain in 2027 ($2,500 minus $1,500 basis)

Example 2: OZ Fund Interest Sold After Year 10

- Facts

- Same as Example 1, except that the taxpayer sells the OZ fund interest for $2,500 in 2028 (after holding the OZ fund interest for more than 10 years) instead of 2027

- Tax Consequences

- Taxpayer does not recognize $1,500 of gain in 2018

- Taxpayer takes a $0 basis in its OZ fund interest

- Taxpayer’s basis in its OZ fund interest increases from $0 to $150 in 2023

- Taxpayer’s basis in its OZ fund interest increases from $150 to $225 in 2025

- Taxpayer recognizes $1,275 of gain in 2026 ($1,500 of deferred gain minus $225 of basis step-up)

- Taxpayer’s basis in its OZ fund interest increases to $1,500 as a result of 2026 gain recognition

- Taxpayer recognizes $0 of gain on the $1,000 of economic appreciation in the OZ fund interest between 2018 and 2028

Example 1 and Example 2 Comparison Table

_________________

1 It is, however, unclear how this rule applies to an OZ business that sells or licenses intangible assets to customers, many of whom are likely to purchase the intangibles from outside the zone.

2 The statute also seemingly permits an OZ fund to operate a sin business directly while prohibiting an OZ portfolio company from doing so. We assume that the prohibition on the operation of a sin business will be extended by regulation to businesses directly held by an OZ fund.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.