The U.S. high-yield market delivered the third strongest year by volume in 2014, with more than $310 billion of primary issuances,1 thanks in large part to the most active year in the M&A market since before the financial crisis. (See "M&A Activity Jumps to Levels Unseen Since Before Global Financial Crisis.") With promising predictions for M&A in 2015 and several other key drivers of volume in place (including higher yields relative to other asset classes, a strengthening U.S. economy and low default rates generally), the overall outlook for the 2015 high-yield market is positive.

However, investor expectations are tempered because of increased risk and volatility at a time when returns are near record lows. Declines in high-yield bond prices in the second half of 2014 as a result of concerns about higher risk — from both issuer-favorable bond terms and the market impact of geopolitical and macroeconomic factors, in particular the effect of falling oil prices on energy companies — were a reminder that the high-yield market, which has remained robust for several years, is not immune to volatility. Although the market in general rebounded relatively quickly, underscoring the desire for higher-yielding investments, the continued strength of the high-yield market depends on investors' ability to maintain the right balance between risk and return to find opportunities in the face of increased volatility.

Key Trends and Outlook for 2015

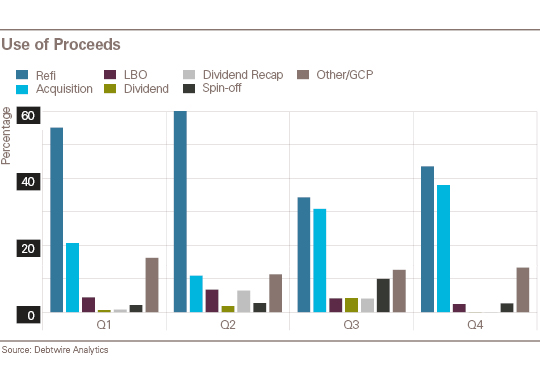

Acquisition Financings. A reflection of the strong M&A market, acquisition financings represented an increased portion of high-yield offerings in 2014, a trend likely to continue in 2015. Of 2014 deal volume, close to 30 percent funded acquisitions (including LBOs), with a greater portion of this activity in the second half of the year. Refinancings made up only around 40 percent of 2014 deal volume, in comparison to more than 50 percent in 2013.

Energy Companies. Energy companies comprised the largest proportion of high-yield issuances by sector in 2014 and represent the second-highest share of the market overall behind media and telecom, at more than 15 percent. Factors that negatively affected this industry, such as falling oil prices and operational cash concerns, also negatively affected the high-yield market. In particular, hard-hit exploration and production and oilfield services companies were some of the principal contributors to the decline in high-yield prices at the end of 2014 and represented a significant portion of the pulled deals for that period. Although the high-yield market as a whole has largely stabilized from the declines (and some sectors, such as consumer retail, may benefit from the decrease in oil prices), the overall outlook for energy-sector high-yield remains recessionary if oil prices remain low. However, increased M&A activity and solid asset coverage may create some opportunities in the sector in 2015, particularly for issuers with strong corporate fundamentals and more diverse energy exposure, including integrated energy companies, and for issuers seeking additional liquidity, including through second-lien deals.

High-Yield Lite. Bond issuers continued to enjoy low coupons and issuer-friendly terms in 2014, with “high-yield lite” bonds accounting for an increasingly greater portion of issuances. A covenant package typically is considered to be “high-yield lite” if it lacks either a debt incurrence covenant or a restricted payments covenant, or both (although high-yield lite deals often also lack other traditional high-yield covenants and have investment-grade style redemption provisions). According to Moody’s, credit quality reached a record-low level at the end of 2014 as a result of lower-rated credits going to market with weaker covenant packages, including high-yield lite structures which accounted for almost half of the issuances in September and October. Historically issued by “fallen angels” — high-yield issuers that were previously investment grade — or by issuers on the cusp of being investment grade, high-yield lite bonds are now frequently issued by first-time high-yield issuers with ratings well below investment grade. High-yield lite is unlikely to disappear in 2015; however, it may become more difficult for companies that do not have strong credits, or historic high-yield lite or investment grade bonds, to depart from traditional high-yield covenant packages to the extent seen in 2014.

Shortened Tenor and Noncall Periods. The weighted average maturity of high-yield issuances has steadily declined over the past two years, reaching a low of around seven years in the first quarter before ending 2014 at slightly above eight years. Increased issuances of five-year and eight-year bonds helped drive the decline in the average. The issuer-favorable trend of the shortened “noncall” period also continued in 2014. Although issuers in the past often paid for this flexibility with a higher first-call premium of 75 percent of the coupon, many issuers in 2014 were able to get the best of both worlds — a shorter noncall period with the traditional 50 percent of the coupon first-call premium.

Heightened Risk and Volatility. In July, Federal Reserve Chair Janet Yellen cautioned investors regarding heightened risks in lower-rated corporate debt. The returns on high-yield bonds (and the spread to U.S. treasuries) are near record lows, with little cushion to protect investors from increased volatility and risk. Meanwhile, the historic demand for high-yield bonds has led to more risk in the market, with more issuer-friendly provisions, including high-yield lite terms and shortened noncall periods, and more speculative issuances, in both use of proceeds and issuer credit quality. As issuers continued to push for increased covenant flexibility, traditionally European high-yield terms — such as a “portable” change-of-control feature and market capitalization-based dividend baskets — began to appear in a few, more aggressive deals; and prior trends of leverage or asset-based restricted payments and debt incurrence baskets continued. In addition, geopolitical risks, broader global economic factors and macroeconomic factors in the U.S. — including a potential rise in interest rates and the impact of sustained low oil prices on the energy sector — could negatively impact bond prices and increase issuer borrowing costs, which may lower demand in 2015.

Leveraged Lending Guidelines. What impact the leveraged lending guidelines will have on the high-yield market, including whether there will be an increase in bond-for-loan refinancings in 2015, also remains to be seen. Although the guidelines apply to loans rather than bonds, with the increased Federal Reserve attention on lower-rated corporate debt generally and difficulties in placing some very highly leveraged bond deals, it is not clear that high-yield bonds will fill the gap for deals with leverage in excess of the amount permitted by the guidelines.

Focus on Credit Quality and Liquidity. As a result of increased risk and volatility, investors may be more selective in 2015. Higher-rated issuers, strong sponsor-owned companies and healthy strategic acquirers should fare best as investors focus on key credit fundamentals, such as leverage, cash flows and credit-enhancing uses of proceeds. Repeat issuers that are able to place larger deals also likely will be in demand as investors seek increased liquidity and flexibility to reduce exposure to macroeconomic factors. The demand by investors for credit quality and liquidity also may contribute to increased M&A activity financed by investment-grade bonds. In contrast, smaller issuers and those with weak corporate or industry-sector fundamentals, aggressive structures or more speculative uses of proceeds may face greater difficulty issuing new debt than in prior years.

__________________

1 Volume and other statistical data discussed in this article are based on information provided by HighYieldBond.com, Thomson Reuters and the Debtwire High Yield Database.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.