This update provides an overview of key regulatory developments from Q4 2021 relevant to companies listed or planning to list on The Stock Exchange of Hong Kong Limited (HKEx) and to their advisers. In particular, it covers amendments to the Rules Governing the Listing of Securities on HKEx (Listing Rules) as well as announcements, guidance and enforcement-related news from HKEx and the Securities and Futures Commission (SFC). Other recent market developments may also be included. We do not intend to cover all updates that may be relevant, but we welcome feedback, so please contact us if you would like to see analysis of other topics in the future.

- HKEx Finalizes New Rules on Listings for Overseas Issuers

- HKEx To Allow SPAC Listings

- HKEx Consults on New Rules for Listed Company Share Schemes

- SFC Publishes Consultation Conclusions on Code of Conduct on Bookbuilding and Placing Activities

- HKEx Revises Corporate Governance Code

- HKEx Publishes Guidance on Climate Disclosures

- Enforcement Matters

HKEx Finalizes New Rules on Listings for Overseas Issuers

Following a consultation process conducted in 2021, HKEx announced amended listing rules for overseas companies undertaking dual-primary or secondary listings in Hong Kong. The new rules provide additional flexibility that is expected to facilitate more companies listing on HKEx and clarify the paths for converting a secondary listing to a primary listing. The amendments took effect starting 1 January 2022.

Please refer to our 14 December 2021 client alert “HKEx Finalizes New Rules on Listings for Overseas Issuers” for more details on this topic.

HKEx To Allow SPAC Listings

Following a consultation process in 2021, HKEx announced its new regime for the listing of Special Purpose Acquisition Companies (SPACs) in Hong Kong.

We reported on the consultation in our October 2021 Hong Kong Regulatory Update. The final rules have moderated some of the proposals in the consultation paper in an attempt to make the final SPAC regime more attractive to potential SPAC promoters and de-SPAC targets while retaining most of the investor protection features HKEx initially proposed.

Key changes from the initial proposals include the following:

- The threshold for distribution in a SPAC IPO has been reduced from 30 institutional professional investors to 20 institutional professional investors. A SPAC will still be required to distribute to a minimum of 75 professional investors overall.

- SPACs will still be obliged to refund 100% of IPO proceeds in case of redemption, but will not be required to refund interest accrued, which may be used for the SPAC’s operating purposes.

- The requirement to align redemption with voting has been dropped, such that shareholders voting for a de-SPAC transaction may still opt to redeem their shares.

- The size of the mandatory PIPE investment that a SPAC must undertake in conjunction with any de-SPAC transaction will be based on a sliding scale, with a minimum PIPE investment of 25% for a de-SPAC valuation of less than HK$2 billion to as low as an investment of 7.5% for a de-SPAC valuation of HK$7 billion or more. At least 50% of the PIPE investment must be contributed by at least three sophisticated investors (defined as investors with assets under management of at least HK$8 billion).

The new regime came into effect starting 1 January 2022.

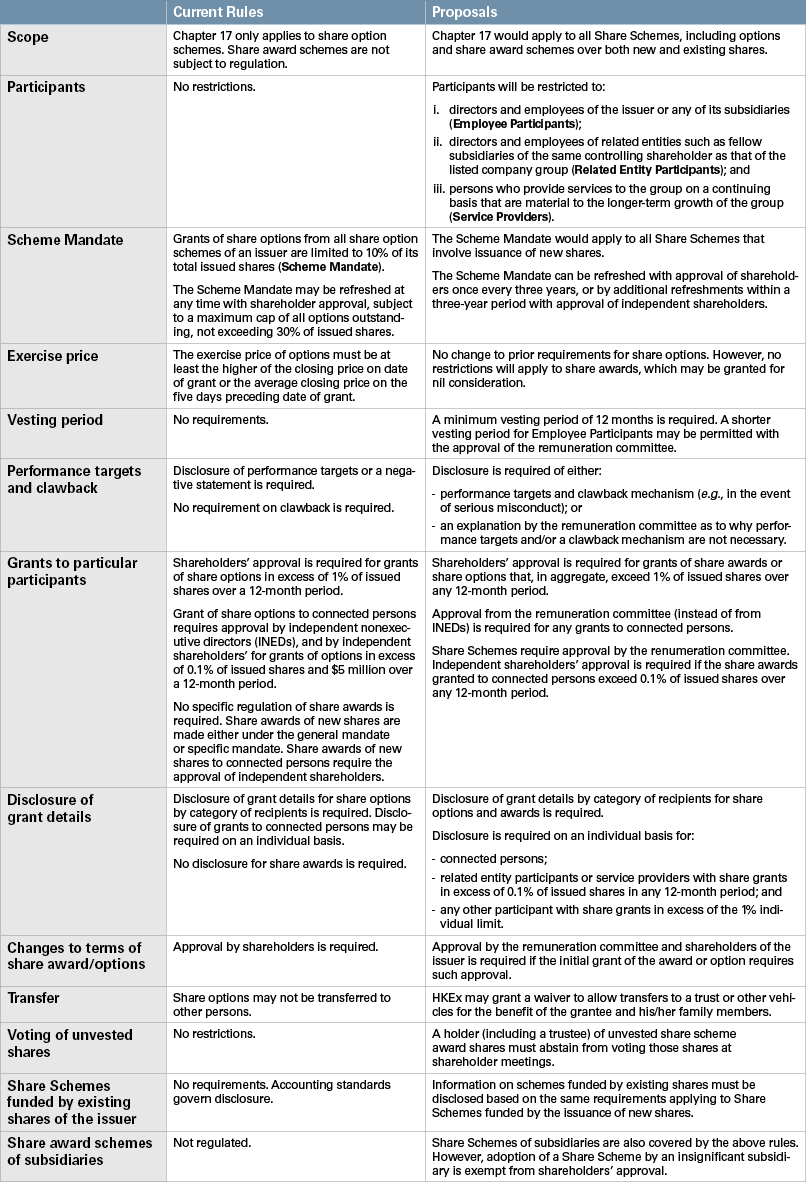

HKEx Consults on New Rules for Listed Company Share Schemes

A large number of issuers listed on the HKEx have share option schemes and share award schemes (Share Schemes) to incentivize employees and service providers by aligning their interests with those of the issuers and their shareholders.

HKEx recently published a consultation paper proposing to amend the Listing Rules regarding Share Schemes. The new rules would extend the current regulation of share options to cover share award schemes, as well as introduce new restrictions to the terms of Share Schemes. The consultation period ended on 31 December 2021.

A summary of the key proposed amendments is set out below.

If the proposed amendments are adopted, the new rules would apply to new Share Schemes adopted on or after the effective date of the amended rule. For all existing Share Schemes (whether funded by new or existing shares), issuers would also be required to comply with the new disclosure requirements from the effective date. For Share Schemes that are still valid, share awards or options may continue to be granted to eligible participants. Share award schemes involving grants of new shares under general mandate must comply with the new requirements by the first annual general meeting after the effective date.

SFC Publishes Consultation Conclusions on Code of Conduct on Bookbuilding and Placing Activities

Following the SFC’s consultation paper on the conduct requirements for bookbuilding and placing activities (covered in our April 2021 Hong Kong Regulatory Update), the SFC has announced its consultation conclusions and amended its Code of Conduct for Persons Licensed by or Registered With the Securities and Futures Commission (Code of Conduct) governing bookbuilding and placing activities in equity capital market and debt capital market transactions. The amended Code of Conduct introduces a number of new requirements for investment banks working on capital market transactions in Hong Kong.

Key requirements under the amended Code of Conduct include:

- Advice on fee arrangements: The overall coordinator (OC) is required to provide guidance to the issuer on market practices for the total fee and fee split ratio in the case of an IPO. The SFC considers current market practice to feature a 75% fixed and 25% discretionary fee split, and the commission expects issuers to assess whether to deviate significantly from the 75:25 fee split ratio.

- Timing for appointment of OCs and syndicate members and fee determination: (i) OCs are required to inform the SFC of the composition of the entire syndicate or the allocation of fixed fees to individual syndicate capital market intermediaries (CMIs) at the time of publication of the prospectus, consistent with existing practice; (ii) OCs must be appointed no later than two weeks after the A1 submission; and (iii) OCs are required to inform the SFC of all the OCs participating in the IPO, the fixed fee payable to each of them, the total fees and the fee split ratio four full business days before the Listing Committee hearing.

- Disclosure of identities of underlying investors for orders placed on an omnibus basis: CMIs must disclose the identities of underlying investors to OCs to enable OCs to manage the order book and identify and eliminate duplicate orders, inconsistencies and errors. When CMIs provide information of underlying investors to the relevant OC when placing orders, (i) the CMI must provide the client’s name and unique identification number, and (ii) CMIs (including OCs) that receive information about investors in a share or debt offering may use the information only for that specific offering.

- Sponsor coupling: Issuers must appoint at least one OC to act as an independent sponsor (Sponsor OC) that has obtained a thorough understanding of the issuer through due diligence and is in a position to give quality advice to the issuer throughout the transaction. This requirement to appoint a Sponsor OC will only be applicable to Main Board IPOs.

The new rules take effect in August 2022.

HKEx Revises Corporate Governance Code

HKEx has revised its Corporate Governance Code (CG Code) for listed companies and related Listing Rules, following a consultation process in 2021. HKEx has also published a new corporate governance guide to help listed companies comply with the new requirements.

Key changes introduced by the new rules include the following:

- Board diversity: HKEx will no longer permit listed companies to have single-gender boards. Any existing company with a single-gender board must appoint a director of a different gender no later than December 31, 2024 (and is encouraged to make such an appointment at any such earlier time that an existing director retires by rotation). The new rules require a listed company to make detailed diversity disclosures in its annual Corporate Governance Report (CG Report), including numerical targets and timelines for board and workforce diversity and for the board to conduct an annual review of the effectiveness of its diversity policies.

- A nomination committee: All listed companies are required to establish a nomination committee chaired by either the board chairperson or an INED and comprising a majority of INEDs.

- INEDs rotation: Starting January 1, 2023, if all INEDs on a board have served more than nine years (Long-Serving INEDs), the listed company must appoint a new INED at the forthcoming annual general meeting. If a company proposes to reelect a Long-Serving INED, the board must set out reasons why it believes the Long-Serving INED is still independent and should be reelected, and the reelection by the shareholders must be subject to a separate resolution. In addition, a new recommended practice suggests a listed company should not grant equity-based remuneration with performance-related elements (e.g., share options or grants) to INEDs, as HKEx believes this may lead to bias in their decision-making and compromise their objectivity and independence.

- Board independence: A listed company must establish mechanisms to ensure independent views and inputs are available to the board and disclose such mechanisms in its CG Report.

- Culture expectations: Listed company boards are required to actively consider company culture, and seek to align that culture with a clearly articulated purpose, values and strategy. HKEx expects directors to act with integrity, lead by example and promote the desired culture and to seek to align that culture throughout the organisation. HKEx notes that corporate culture should include values of acting lawfully, ethically and responsibly.

- Anticorruption and whistleblowing policies: All listed companies must establish policies and systems that support anticorruption laws, as well as a whistleblowing policy providing for employees and those who deal with the company (e.g., customers and suppliers) to confidentially and anonymously raise concerns about improprieties.

- Communication with shareholders: A listed company must maintain a shareholders’ communication policy that includes channels for shareholders to communicate their views on matters affecting the listed company. The company must also make several disclosures on shareholder communications in its CG Report.

- An ESG reporting timeline: HKEx has clarified the timing for publication of environmental, social and governance (ESG) reports, now requiring a listed company to publish its ESG report as part of or at the same time as its annual report.

The revised CG Code took effect on 1 January 2022 (unless otherwise noted above), and the requirements of the new CG Code will apply to CG Reports for financial years commencing on or after that date.

HKEx Publishes Guidance on Climate Disclosures

HKEx has published its Guidance on Climate Disclosures to provide practical guidance for listed companies in complying with the recommendations by the Task Force on Climate-Related Financial Disclosures, which practices will become mandatory across relevant sectors no later than 2025. The guidance provides details on the specific climate-related disclosures a listed company should make.

Some of the key requirements include:

- Governance structure on climate-related issues: The listed company should have an appropriate governance structure for overseeing climate-related issues, for example, maintaining a separate committee to track climate-related issues or integrating climate-related issues into the terms of reference of existing committees. The board and management team should have the necessary expertise to manage climate-related risks.

- Climate scenarios impact analysis: The listed company should consider best-case and worst-case climate scenarios, drawing on publicly available scenarios developed by organizations such as the Intergovernmental Panel on Climate Change and the International Energy Agency; identify the relevant risks resulting from climate change; and analyze how those risks will impact the listed company’s assets and operations.

- List of prioritized climate-related risks: The listed company should disclose: (i) a list of material climate-related risks to the company; and (ii) how it identified and prioritized those material risks, including any quantitative or qualitative assessment conducted.

- Impact of material risks: The listed company should: (i) explain how the identified material climate-related risks impact each component of its value chain; and (ii) describe its impact assessment methodology, including any quantitative or qualitative assessment conducted.

- Metrics, indicators and targets adopted to measure and monitor climate-related risks: The listed company should: (i) disclose certain metrics applicable for all industries, including greenhouse gas emissions, carbon price, proportion of assets or business activities materially exposed to climate-related risks, and the amount of expenditure or capital investment deployed toward climate-related risks and opportunities; (ii) develop and disclose other metrics and indicators where doing so facilitates the investors’ understanding of the climate-related risks relevant to the listed company; and (iii) set forward-looking targets for the metrics and indicators.

- Action plan: The listed company should set out a specific and detailed plan to achieve the forward-looking targets, including (i) an implementation timeline, (ii) the department or business unit responsible for implementation, (iii) the progress of the action plan, (iv) the estimated costs of the action plan and (v) the estimated impacts of the action plan.

- Impact on financial performance: The listed company should disclose how climate-related issues affect specific items in its financial statements by conducting qualitative or quantitative assessment.

- Business strategy: The listed company should discuss how its business strategy and strategic direction will change in response to climate-related risks and opportunities.

Enforcement Matters

HKEx Censures Director of Daisho for Breach of Listing Rules

In September 2017, Daisho Microline Holdings Limited entered into an agreement to acquire four vessels. Daisho’s executive director, Ms. Cheung Lai Na, directed Daisho to issue a cheque and promissory note to the vendor despite being aware that one of the conditions for completion had not been satisfied, in that the mortgages for the relevant vessels had not been fully discharged. Subsequently, the 2018 interim results and interim report stated that the acquisition had been completed and the results were prepared on that basis, such that Daisho’s stated financial position regarding its total assets was not accurate.

In November 2021, HKEx found that Ms. Cheung breached the Listing Rules and her director’s undertaking for her failure to (i) properly monitor the acquisition’s progress and ensure its completion was in accordance with the terms of the agreement, (ii) ensure that information disclosed in a corporate communication was accurate (resulting from her failure to follow up on the discharge of the mortgages and completion status), (iii) keep the board informed about the acquisition’s completion status and (iv) ensure the company had an adequate internal control system.

HKEx directed Daisho to retain an independent professional adviser to conduct an internal control review and required Ms. Cheung to attend training.

This case highlights that listed companies must monitor the progress of transactions to ensure the legal terms are met and that financial results accurately reflect the legal status of the transaction.

HKEx Censures Huiyuan Juice for Breach of Connected Transaction Rules

Connected transactions are frequently a compliance risk for listed companies, as a recently resolved case involving Huiyuan Juice Group Limited illustrates. This case also serves to remind directors that delegation does not absolve them from their duty to supervise the delegated functions, for which they collectively and individually retain ultimate responsibility.

Between August 2017 and March 2018, Huiyuan Juice entered into a loan agreement with a borrower that was a connected person to Mr. Zhu Xinli, an executive director of Huiyuan Juice. The loans were unsecured and not recorded in the company’s accounting books until after the loans were discovered months later. The loans constituted a major and connected transaction, to which the company agreed without obtaining board or shareholder approval. In addition, internal control reviews identified a number of internal control deficiencies at the company, including issues concerning fund transfers, late account recording and nonapproved payments.

In November 2021, HKEx censured Huiyuan Juice for failing to (i) comply with the Listing Rules requirements for a major and connected transaction, (ii) ensure Huiyuan Juice’s financial information was accurate and (iii) explain its deviation from CG Code Provision C.1.2, which requires management to ensure the board is provided with monthly updates in sufficient detail.

HKEx also censured executive directors Mr. Zhu and Ms. Zhu Shengqin for failing to (i) avoid actual and potential conflicts of interest, (ii) update the list of connected persons promptly and (iii) ensure the company had an adequate internal control system that could effectively identify transactions connected to them.

In addition, HKEx censured Mr. Zhu for endorsing a further connected transaction with the same borrower when he was already aware of the previous loans at the time of endorsement. Mr. Zhu approved the further connected transaction without (i) informing the board, (ii) declaring and/or avoiding his conflict of interest, (iii) considering and discussing with the board the Listing Rule implications and (iv) taking steps to procure compliance with the Listing Rules.

Further, HKEx censured the directors of Huiyuan Juice for failing to (i) promptly alert the board of important matters such as the discovery of improperly authorized loans, (ii) take active steps to address internal control deficiencies, (iii) ensure adequate training and supervision was provided to the department that was authorized to approve internal fund transfers, and (iv) apply the degree of skill, care and diligence necessary in their roles.

HKEx ordered the relevant directors to attend 24 hours of training on Listing Rules compliance and issued a prejudicial statement against Mr. Zhu for his willful and persistent breaches of the Listing Rules.

HKEx Sanctions Bonny International for Breach of Connected Transactions Rules

Bonny International Holdings Limited entered into procurement agreements with a connected party, pursuant to which Bonny International made prepayments to the connected party of approximately RMB250 million. Around 75% of the procurement agreements were cancelled shortly after they were entered into and the connected party refunded approximately RMB220 million to Bonny International. However, the cancelled orders counted towards the company’s annual caps, with the result that Bonny International exceeded its annual caps for 2019 and 2020, in breach of the Listing Rules. Bonny International also failed to comply with the requirements for announcements, circulars, independent shareholders’ approval, reporting and annual cap for the prepayments.

In December 2021, HKEx censured Bonny International for failing to consult its compliance advisor prior to entering into the procurement agreements and censured its two directors for failing to comply with the Listing Rules, and ordered the directors to attend training on regulatory and legal topics.

This case highlights that cancelled or refunded orders for continuing connected transactions still count towards the relevant annual transaction caps.

HKEx Criticizes China Ruifeng for Failure To Comply With Major Transaction Requirements

HKEx has criticized a director who unsuccessfully tried to “cure” his breach of the Listing Rules by entering into a supplemental agreement purporting to release the company from the liability established in his initial agreement with a third party.

Mr. Peng Zi Wei, an executive director of China Ruifeng Renewable Energy Holdings Limited, executed a US$100 million guarantee on behalf of China Ruifeng to facilitate the proposed acquisition of an offshore reinsurance company by a third party — without informing the rest of the board or complying with China Ruifeng’s internal control procedures. The guarantee also constituted a major transaction for China Ruifeng under the Listing Rules.

Mr. Peng argued that by signing a supplemental agreement that effectively negated the guarantee and released China Ruifeng from liability in the event that the proposed acquisition was unsuccessful, the arrangement did not constitute a “transaction” under the Listing Rules. However, HKEx did not agree and viewed the guarantee as legally binding if the proposed acquisition had been completed.

HKEx therefore criticized (i) China Ruifeng for failure to comply with the Listing Rules requirements for a major transaction and (ii) Mr. Peng for signing the guarantee without informing the board, obtaining board approval, complying with the China Ruifeng’s internal control procedures or securing the company’s compliance with the Listing Rules.

HKEx directed Mr. Peng to attend training and China Ruifeng to review its internal controls for procuring compliance with the Listing Rules relating to notifiable transactions and connected transactions.

HKEx Takes Disciplinary Action Against Former Director of China Fortune

A recent case highlights the obligations of a director to respond to inquiries from HKEx and to cooperate with any investigations by the exchange, even after he or she ceases to be a director. Former directors must also provide current contact details to HKEx.

Mr. Luo Xi Zhi Peter, an executive director of China Fortune Holdings Limited from September 2002 to April 2018, failed to respond to inquiries from HKEx and to cooperate with the exchange’s investigation as to whether he breached certain Listing Rules. HKEx sent an investigation letter and a reminder to his last known address, but Mr. Luo failed to respond to the inquiries.

As a result, in November 2021, HKEx found that Mr. Luo (i) breached his undertakings to cooperate with the investigation and (ii) obstructed the proper discharge of HKEx’s function to maintain and regulate an orderly market. HKEx considered Mr. Luo’s breach to be serious because his conduct demonstrated willful and persistent failure to discharge his responsibilities under the Listing Rules. Accordingly, HKEx issued a statement that, had Mr. Luo remained on the board of directors of China Fortune, his retention of office would have been prejudicial to the interests of investors.

HKEx Censures China U-Ton for Breach of Listing Rules on Winding-Up Petitions

Listed companies must announce winding-up petitions, and other events relating to winding-up, liquidation or enforcement against the issuer’s assets, as soon as the company becomes aware of them. The obligation to announce arises immediately upon presentation of the petition, and is not contingent on the expected or actual outcome of the petition, including whether the issuer believes that the petition lacks merit or whether an agreement may be reached to withdraw the petition.

In a recent case addressing this issue, HKEx censured China U-Ton Future Space Industrial Group Holdings Limited for breaching the Listing Rules by failing to inform HKEx about winding-up petitions presented to it. Between February 2021 and April 2021, China U-Ton was presented with four winding-up petitions but did not publish an announcement or inform HKEx as soon as the company was aware of these petitions. HKEx was not aware of these petitions until the High Court made a winding-up order against China U-Ton in May 2021. HKEx subsequently suspended the company’s trading privileges.

Inadequate Sponsor Due Diligence on Distributors Prompts SFC Action

The use of distributors by a listing candidate can often be a risk area for sponsor due diligence, as highlighted in a recent SFC enforcement case.

Ample Capital Limited (ACL) acted as a sponsor in connection with COCCI International Limited’s application to list on the GEM board of HKEx. A major distributor accounted for a substantial portion of COCCI’s total revenue and contributed significantly to the group’s revenue growth. The SFC found that ACL’s due diligence in relation to this distributor was inadequate in a number of areas:

(i) regarding the payments settled by the distributor, which were made through several third parties. According to the SFC, settlement through such third parties was a red flag, as the third parties could be used to disguise the original source of the funds and facilitate a fraudulent scheme;

(ii) regarding the independence of the distributor, as information suggested a connection between the distributor, a COCCI director and an indirect COCCI shareholder; and

(iii) regarding sales to the distributor, which entity purportedly distributed products to other end customers. In particular, ACL did not verify information provided by the end customers, for example, by way of site visits or interviews, and failed to use publicly available information to verify the accuracy of documents.

The SFC found these inadequacies particularly concerning given the importance of the distributor as a source of revenue and growth for COCCI.

The SFC determined that ACL breached multiple provisions of the Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission by failing to perform its due diligence obligations properly. Furthermore, the SFC found that ACL breached its duty under the Corporate Finance Adviser Code of Conduct to act with due skill, care and diligence and observe proper standards of market conduct in the best interests of its clients and the integrity of the market. The SFC attributed ACL’s breaches to its responsible officer’s failure to, among other practices, act with due skill, care and diligence in handling the listing application and supervising ACL’s work as a sponsor. Accordingly, in October 2021, the SFC suspended the responsible officer’s license for 17 months.

SFAT Affirms SFC Action on Sponsor Failures

The Securities and Futures Appeals Tribunal (SFAT) has upheld the SFC’s decision to reprimand and fine Yi Shun Da Capital Limited (YSD Capital) for failing to discharge its duties as the sponsor in the listing application of Imperial Sierra Group Holdings Limited in 2017.

The SFC found that YSD Capital failed to perform all reasonable due diligence on Imperial Sierra before submitting the listing application and to ensure that all material information obtained was included in the draft listing document submitted to HKEx and that the information was accurate and substantially complete.

Third-party payments: Imperial Sierra received substantial payments from customers through third parties during the three years ended 31 December 2014, 2015 and 2016. However, YSD Capital (i) failed to verify with Imperial Sierra’s customers their relationships with the third-party payers and the reasons for the third-party payments even when it was apparent that some third-party payers did not know the reasons for such payments, (ii) simply relied on Imperial Sierra’s representation as reasons for the third-party payments and (iii) failed to conduct independent enquiries and make appropriate follow-up enquiries to address several warning signals regarding the third-party payments.

Loan and investment arrangements: Imperial Sierra recorded a shareholder’s loan of HK$35 million as of January 2017, which consisted of withdrawals made by the chairman and controlling shareholder to facilitate various loan and investment arrangements between him and his acquaintances. The SFC found that YSD Capital failed to (i) obtain and review the agreements and the bank transaction records related to these loan arrangements before submitting the listing application, (ii) investigate the loans despite learning that some acquaintances were unable to explain the reasons or purposes of the loan arrangements, (iii) disclose the fact that some acquaintances were third-party payers or entities connected with Imperial Sierra’s customers and (iv) take appropriate steps to verify the relationships between some acquaintances and Imperial Sierra’s customers.

Suspicious transactions: The SFC also found suspicious transactions that should have called into question whether Imperial Sierra and/or its chairman had provided financial support for some of its customers’ payments. For instance, YSD Capital failed to perform any meaningful due diligence on the transactions in which Imperial Sierra transferred RMB2 million to a third-party payer as a personal loan advanced by Imperial Sierra’s chairman two days after the same third-party payer made a payment of RMB2.3 million to Imperial Sierra on behalf of a prominent customer.

The SFC further found that YSD Capital had failed to ensure disclosure of all material information — in particular, information on the above matters — in Imperial Sierra’s draft listing documents.

The SFAT, agreeing with the SFC’s findings, stated that undue reliance on management representations cannot be regarded as a proper discharge of reasonable due diligence. In response to YSD Capital’s claim that YSD Capital had been entitled to rely on the view expressed in the accountant’s report that the financial statements gave a true and fair representation of Imperial Sierra’s financial affairs, the tribunal ruled that a sponsor cannot wash its hands of the matter on the basis that the reporting accountant found nothing that required it to qualify its report.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.