On June 8, 2017, the House of Representatives passed, by a 233-186 party-line vote (with all Democrats and one Republican voting against), the Financial CHOICE Act of 2017, a bill principally designed to reverse many features of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank). The House Financial Services Committee majority has provided both an executive summary and a comprehensive summary of the current bill. It is unclear at this time what action the U.S. Senate will take with regard to the bill in its current form.

While the vast majority of the bill relates to the banking provisions of the Dodd-Frank Act and other financial regulatory reforms, the bill also contains a number of substantive and procedural changes that are intended to facilitate greater access to the capital markets by issuers and reduce regulatory burdens generally on public and private companies.

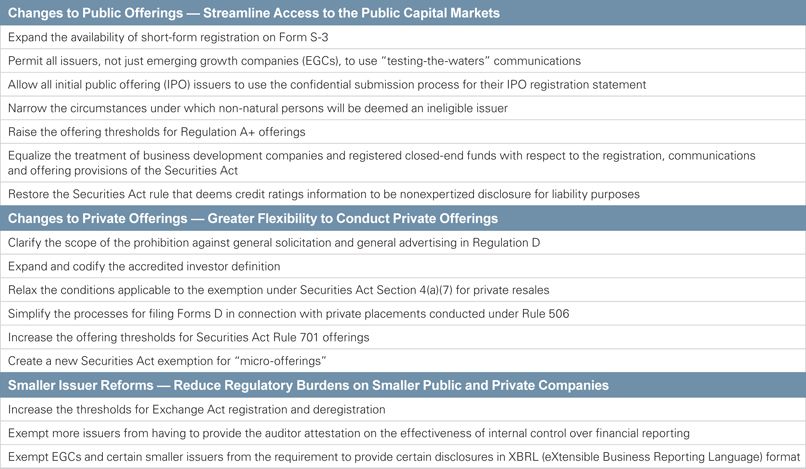

The following is a summary of the key capital markets reforms contained in the bill.

Changes to Public Offerings

Form S-3 Eligibility (Section 426). Subject to the conditional exception discussed immediately below, the transactional requirements of Form S-3 currently only permit an issuer to register a primary offering for cash on a “short-form” Form S-3 where the aggregate market value of the voting and nonvoting common equity held by nonaffiliates (i.e., public float) of the issuer is $75 million or more.1 The bill directs the SEC to loosen the transaction requirements to permit primary offerings by an issuer without regard to its public float so long as it has at least one class of common equity securities listed and registered on a national securities exchange.2

Additionally, issuers that are not, and have not been, a shell company for the last 12 months and that have a public float of less than $75 million have been conditionally permitted to register on Form S-3 smaller primary offerings of securities in an aggregate amount not to exceed more than one-third of their public float so long as the issuer has a class of common equity securities that is listed and registered on a national securities exchange. The bill directs the Securities and Exchange Commission (SEC) to remove the requirement that these issuers have at least one class of common equity securities listed and registered on a national securities exchange.

The bill does not mandate corresponding changes to Form F-3, the analogous short-form registration statement available to foreign private issuers.

Testing the Waters and Confidential Submissions for IPOs (Section 499). The Jumpstart Our Business Startups Act (JOBS Act) significantly eased long-standing Section 5 restrictions on “gun-jumping” by permitting an EGC, or a person authorized to act on the EGC’s behalf, to make oral and written offers to qualified institutional buyers and institutional accredited investors (“testing-the-waters” communications) before or after the filing of a registration statement to gauge investors’ interest in the offering. The bill expands Section 5(d) of the Securities Act to permit all issuers, not just EGCs, to engage in testing-the-waters communications.

The JOBS Act also permits EGCs to confidentially submit draft IPO registration statements to the SEC for review. The bill amends Section 6(e) of the Securities Act to permit all issuers contemplating an IPO to take advantage of the confidential review process, subject to the requirement that the initial confidential submission and all amendments thereto be publicly filed with the SEC no later than 15 days before the date on which the issuer conducts a roadshow.

Elimination of Automatic Disqualification as an Ineligible Issuer (Section 827). Currently, certain judicial or administrative decrees or orders arising out of governmental actions in response to “bad acts” committed by an issuer will result in that issuer becoming an “ineligible issuer” under Rule 405 of the Securities Act.3 An ineligible issuer automatically loses well-known seasoned issuer (WKSI) status for a period of three years and as result will not benefit from automatic shelf registration.4 Additionally, ineligible issuers are unable to use free writing prospectuses, except for those that are limited to descriptions of terms of the offered securities and the offering.

The bill narrows the circumstances under which a non-natural person will be deemed an ineligible issuer and provides that certain SEC or government enforcement actions or settlements will no longer result in issuers, including WKSIs, becoming subject to automatic disqualification as an ineligible issuer.5

Regulation A+ Expansion (Section 498). Regulation A is an exemption from registration under Section 3(b) of the Securities Act for certain small issuances, where the exempt transactions typically share certain characteristics with registered public offerings. The JOBS Act amended Section 3(b), directing the SEC to adopt rules exempting from the registration requirements of the Securities Act offerings of up to $50 million per year. The bill would further amend Section 3(b) of the Securities Act to increase the threshold from $50 million to $75 million during a 12-month period, adjusted for inflation every two years.

Parity for Business Development Companies and Registered Closed-End Funds (Sections 438 and 499A). Currently, business development companies and registered closed-end funds are excluded from the WKSI definition and not eligible to use free writing prospectuses. Further, Form N-2, the registration statement form used by business development companies and registered closed-end funds, is not included in the definition of automatic shelf registration statement. The bill would make business development companies and registered closed-end funds eligible for the same securities offering (and proxy) rules as other listed operating companies, including, most prominently, the communication safe harbors and automatic registration provisions in the SEC’s 2005 offering reforms. The bill also would provide a safe harbor regarding certain analysts’ research reports not currently available to business development companies and registered closed-end funds.

Repeal of Dodd-Frank Act Nullification of Rule 436(g) (Section 853). The bill restores Rule 436(g) of the Securities Act, which provides that the security rating assigned to any class of debt securities, convertible debt or preferred stock by an credit rating agency is not considered part of a registration statement prepared or certified by an expert. The restoration of Rule 436(g) will insulate credit rating agencies from Section 11 liability for material misstatements or omissions in the part of the registration statement that includes a credit rating that they provided. Because the credit ratings information will not be deemed expertized disclosure, issuers will be able to include the credit ratings information without obtaining a consent of the credit rating agency (which consent currently is rarely given due to liability concerns). The practical impact of this change may be muted, however, as issuers have been permitted to include a security rating from a credit rating agency in an offering term sheet without having to secure a consent from the agency.

Changes to Private Offerings

General Solicitation (Section 452). The bill directs the SEC to clarify that the prohibition against “general solicitation or general advertising” in Regulation D would not apply to presentations or communications by or on behalf of an issuer made at certain events, including meetings sponsored by angel investor groups, venture forums, venture capital associations and trade associations, so long as (i) any advertising for the event does not reference a specific securities offering, (ii) only limited information about the issuer and its securities offering is communicated at the event, and (iii) the event sponsor does not provide investment advice, charge for attendance, or engage in activities or receive compensation that would require registration as a broker-dealer under the Securities Exchange Act of 1934 or Investment Advisers Act of 1940.

Accredited Investor Definition (Sections 466 and 860). The bill would import the net worth and income tests from the accredited investor definition in Regulation D (and Regulation A) into the statutory definition of accredited investor under the Securities Act. The revised statutory definition would freeze the income test at $200,000 (or $300,000 including spousal income) but permit an inflation-adjustment to the net worth threshold (currently at $1 million) every five years, which would effectively repeal a Dodd-Frank Act mandate requiring each threshold to increase every four years. The bill also would expand the categories of natural persons under the statutory definition who would be considered accredited investors to include, among others, individuals who are (i) licensed or registered brokers or investment advisers, and (ii) deemed by the SEC to have demonstrable education or job experience to qualify such individual as an accredited investor, irrespective of salary or net worth.

Additionally, the bill would direct the SEC to revise Regulation D to provide that a person who is a “knowledgeable employee” of a private fund or the fund’s investment adviser would be an accredited investor for purposes of a Rule 506 offering of a private fund with respect to which the person is a knowledgeable employee.

Expanding the Resale Exemption Under Section 4(a)(7) (Section 431). Section 4(a)(7) contains a conditional exemption for certain private resales of public and private company securities. The exemption codifies much of the so-called “Section 4(1½)” exemption but is best read as more limited in scope due to certain of the conditions attached to the exemption. The bill would liberalize the Section 4(a)(7) exemption by eliminating many of its existing conditions, including the issuer information requirements applicable to transactions in private company securities, and permitting general solicitation and general advertising so long as all such sales are made through a platform available only to accredited investors. Consistent with its purpose of facilitating resales, the amended exemption would remain unavailable for sales by the issuer or its subsidiaries (but could still be used by affiliates of the issuer), underwriters and dealers. As is the case today, securities sold pursuant to the amended Section 4(a)(7) exemption would be “restricted securities,” as defined by Securities Act Rule 144. By stripping away many of the conditions currently found in Section 4(a)(7), the bill would move the statutory exemption closer to the long-standing informal Section 4(1½) exemption.

Private Placement Filing Requirements (Section 466). Currently, an issuer conducting an offering under Rule 506 of Regulation D is required to file an amendment(s) to a previously filed Form D for an offering to reflect certain changes in the information presented in such Form D. The bill directs the SEC to revise the Form D filing requirements so that an issuer relying on Rule 506 is only required to file a single notice of sales containing the information required by Form D not earlier than 15 days after the date of first sale of securities. The bill also would prohibit the SEC from conditioning the availability of any exemption under Rule 506 on the issuer’s filing of a Form D. Finally, the bill would prevent the SEC from requiring issuers to submit written general solicitation materials to the SEC for a Rule 506(c) offering.

Increased Amounts Permitted Under Rule 701 (Section 406). Rule 701 of the Securities Act provides an exemption from registration for offers and sales of securities by nonreporting issuers to employees pursuant to written compensatory benefit plans or written compensatory contracts. Currently, an issuer must provide enhanced disclosures, including risk factors and financial statements prepared in accordance with (or reconciled to) U.S. generally accepted accounting principles (US GAAP) or International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board, if the aggregate price or amount sold during any consecutive 12-month period exceeds $5 million. The bill directs the SEC to increase the threshold to $20 million and index the amount for inflation every five years.

Registration Exemption for “Micro-Offerings” (Section 461). The bill would amend Section 4 of the Securities Act to add a new exemption from registration for “micro-offerings.” The bill also would deem any securities issued in a micro-offering to be “covered securities,” thus pre-empting such transactions from state blue sky registration provisions. Issuers using the new exemption could not sell to more than 35 purchasers and each purchaser would be required to have a substantive pre-existing relationship with an officer, director or holder greater than 10 percent of the issuer. Additionally, the aggregate amount of all securities sold by the issuer during the 12-month period preceding such transaction cannot exceed $500,000.

Smaller Issuer Reforms

Increased Thresholds for Registration and Deregistration (Section 497). The bill would amend the shareholder thresholds for registration and deregistration under the Exchange Act, making it easier for companies to stay private longer and exit the SEC registration and reporting regime, respectively.

- Section 12(g) of the Exchange Act. Currently, companies must register under Section 12(g) if they have over $10 million in assets and either at least 2,000 holders of record or 500 holders of record that are not accredited investors. The bill would remove the 500 holders registration requirement and mandate the SEC to index the $10 million figure for inflation every five years. The bill also would permit deregistration under Section 12(g) if a company files a certification that its holders of record are less than 1,200 persons, as opposed to the current 300-person threshold.

- Section 15(d) of the Exchange Act. Currently, companies with an effective registration statement under the Securities Act are required to file periodic and current reports with the SEC. The duty to file is suspended automatically by operation of law if the securities to which the registration statement relates are held of record by fewer than 300 persons. The bill would raise the threshold to 1,200 persons.

Evaluation of Internal Control Over Financial Reporting (Sections 441 and 847). Under Section 404 of the Sarbanes-Oxley Act and related SEC rules, each annual report of a public company (other than the initial annual report for a newly reporting public company) must contain a report on internal control over financial reporting that, among other things, contains management’s assessment of the effectiveness of the internal control structure and procedures of the issuer for financial reporting. Similarly, subject to an exemption for EGCs and smaller reporting companies (generally those with a public float less than $75 million), the registered public accounting firm that prepares or issues the audit report for the issuer is required to issue an attestation report on the effectiveness of the company’s internal control over financial reporting.

- Section 441. Temporary Exemption for Low-Revenue Issuers. Under current law, an EGC that otherwise has not triggered any of the disqualification conditions in the EGC definition will cease to qualify as an EGC on the last day of its fiscal year following the fifth anniversary of the date of its first registered sale of common equity securities (typically, its IPO). At that time, the issuer would be subject to the auditor attestation requirement. The bill would allow issuers with average annual gross revenues of less than $50 million to continue to take advantage of the EGC exemption from the auditor attestation requirement until the earliest of (i) the last day of the fiscal year of the issuer following the 10th anniversary of the first sale of registered common equity securities, (ii) the last day of the fiscal year of the issuer during which the average annual gross revenues of the issuer exceeds $50 million, or (iii) when the issuer becomes a large accelerated filer.6

- Section 847. Small Issuer Exemption. The bill would provide an exemption from the auditor attestation requirement for any issuer with a total market capitalization of less than $500 million or any issuer that is a depository institution and has less than $1 billion in assets.

Exemption from XBRL Requirements for EGCs and Other Smaller Companies (Sections 411-413). SEC rules currently require operating companies to provide the information from the financial statements accompanying their registration statements and periodic and current reports in XBRL format by submitting it to the SEC in exhibits to the registration statements and reports, and posting it on their websites. These XBRL requirements apply to operating companies that prepare their financial statements in accordance with US GAAP or IFRS.

The bill exempts EGCs from the requirement to use XBRL for financial statements and other periodic reporting, although EGCs may elect to continue to use it. The bill also exempts companies with total annual gross revenues of less than $250 million until five years after the date of enactment of the Financial CHOICE Act or two years after any determination by the SEC (after completion of a detailed cost-benefit analysis) that the benefits of the requirements to issuers outweigh the costs, but in no event earlier than three years after enactment.

__________________

1 Form S-3 is the “short-form” used by eligible domestic issuers to register securities offerings under the Securities Act. The form allows issuers to rely on their reports filed under the Securities Exchange Act of 1934, as amended (Exchange Act), to satisfy the form’s disclosure requirements. Form S-3 also automatically updates information contained in the prospectus by forward incorporation of Exchange Act reports filed with the SEC after the registration statement is declared effective. The ability to forward incorporate by reference enables an issuer’s prospectus under a registration statement to stay current after effectiveness through the automatic inclusion of the issuer’s current and future Exchange Act reports. An issuer that cannot avail itself of forward incorporation by reference must update its prospectus after effectiveness, either by means of prospectus supplements or post-effective amendments, the latter of which are potentially subject to SEC staff review before becoming effective.

2 The following eligibility requirements for use of Form S-3 remain unchanged by the bill: (i) the issuer has been subject to the Exchange Act registration and reporting obligations (i.e., a public company) for the past 12 calendar months, (ii) the issuer has timely filed all Exchange Act reports required to be filed during the past 12 calendar months (including Forms 10-K, 10-Q, 8-K and proxy reports), (iii) the issuer has not failed to pay any dividend or sinking fund installment on preferred stock since the end of the most recent fiscal year, (iv) the issuer has not defaulted on any material debt or long-term lease since the end of the most recent fiscal year, and (v) the issuer has filed with the SEC and posted on its corporate website all interactive data files (XBRL information) required to have been filed during the past 12 calendar months.

3 “Bad acts” include certain felony or misdemeanor convictions specified in four enumerated provisions under Section 15 of the Exchange Act or judicial or administrative orders or decrees (including settlements) finding or enjoining anti-fraud violations.

4 When an issuer qualifies as a WKSI, it can register a securities offering under the Securities Act on a shelf registration that becomes effective automatically upon filing. This streamlined process provides flexibility for a WKSI to time securities sales to meet market conditions, without waiting for the SEC staff to review and comment on a registration statement and declare it effective. A WKSI is an issuer that satisfies the registrant requirements of Form S-3 or F-3 and either has a common equity public float of $700 million or more, or has issued, in the last three years, at least $1 billion aggregate principal amount of nonconvertible securities, other than common equity in primary registered offerings for cash. A WKSI may not be an ineligible issuer.

5 Specifically, Section 827 would exempt from ineligible status non-natural persons who have been (i) convicted of any felony or misdemeanor or made the subject of any judicial or administrative order, judgment or decree arising out of a governmental action, or (ii) suspended or expelled from membership in, or suspended or barred from association with a member of, a registered national securities exchange or a registered national or affiliated securities association for any act or omission to act constituting conduct inconsistent with just and equitable principles of trade. This would be the case unless the SEC, by order, on the record after notice and an opportunity for hearing, makes a determination that such non-natural person should be disqualified or otherwise made ineligible for purposes of such provision.

6 An issuer becomes a large accelerated filer when all of the following conditions are met as of the end of its fiscal year: (i) the issuer’s public float was $700 million or more as of the last business day of its most recently completed second fiscal quarter, (ii) the issuer has been subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act for at least 12 calendar months, (iii) the issuer has previously filed at least one annual report under Section 13(a) or 15(d) of the Exchange Act, and (iv) the issuer was unable to rely on the smaller reporting company requirements for its annual and quarterly reports.

This memorandum is provided by Skadden, Arps, Slate, Meagher & Flom LLP and its affiliates for educational and informational purposes only and is not intended and should not be construed as legal advice. This memorandum is considered advertising under applicable state laws.